Record Highs, Expensive Oil and a Geopolitical Risk Markets Can No Longer Ignore

The S&P 500 is once again approaching one of those moments where markets look incredibly strong on the surface but increasingly fragile underneath.

After recently pushing toward fresh highs, Wall Street now faces a much more complicated macro environment shaped by three major forces colliding at the same time:

- Rising geopolitical tensions between Iran and the United States.

- Higher oil prices and renewed inflation fears.

- Growing uncertainty around the Federal Reserve’s next move.

And from what I’m seeing, investors are beginning to understand that this combination could become much more important than most expected only a few weeks ago.

Because this is no longer just another geopolitical headline cycle.

This is becoming a macroeconomic story.

A monetary-policy story. An energy story. A liquidity story.

And potentially one of the biggest tests for equities during the second half of 2026.

Wall Street still has powerful bullish drivers supporting the market. Artificial intelligence, strong corporate earnings and massive concentration into mega-cap technology stocks continue acting as fuel for the S&P 500.

But at the same time, geopolitical tensions in the Middle East are injecting a completely different type of risk into financial markets:

An inflationary risk.

And historically, inflation shocks are one of the few things capable of seriously destabilizing expensive equity markets.

S&P 500 vs Brent Oil During Iran–US Escalation

Markets continue climbing despite geopolitical tension, but rising oil prices are beginning to pressure inflation expectations and Fed policy assumptions.

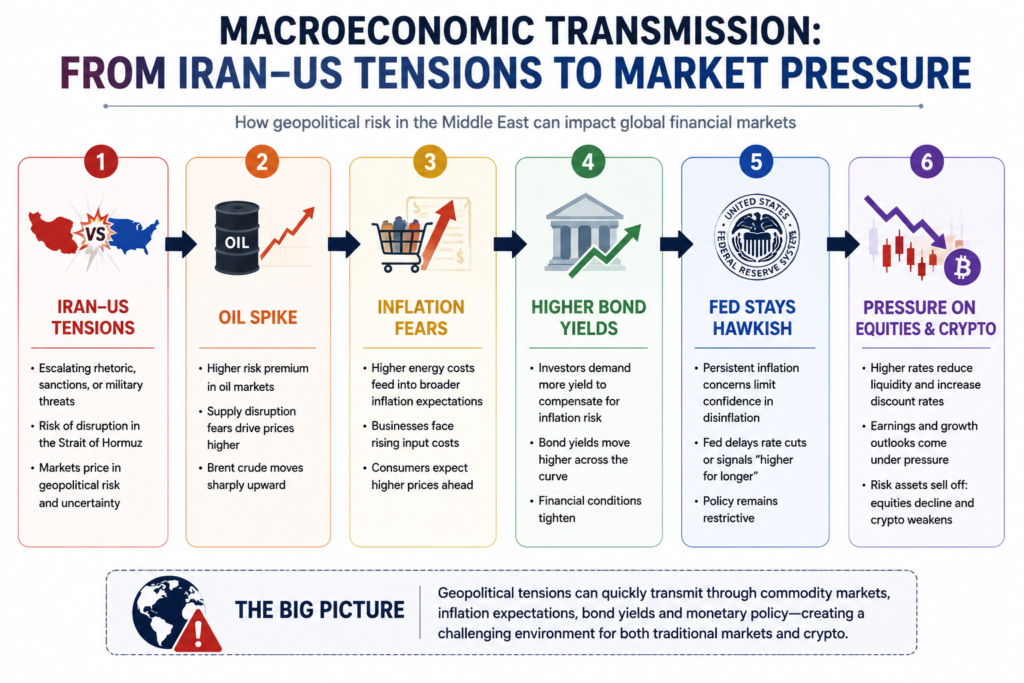

Why Iran and the United States Matter So Much for the S&P 500

At first glance, many investors assume tensions between Iran and the United States only matter for oil traders. That is a massive misunderstanding.

The relationship between geopolitics and the S&P 500 runs much deeper than crude prices alone. Oil is simply the first transmission channel.

The real effects spread into:

- Inflation expectations.

- Bond yields.

- Interest-rate policy.

- Consumer spending.

- Corporate profit margins.

- Liquidity conditions.

- Investor psychology.

And eventually, equity valuations themselves.

The Middle East remains one of the most strategically important energy regions on Earth, especially because of the Strait of Hormuz one of the world’s most critical oil transit corridors.

Any disruption involving Hormuz immediately creates fear around global energy supply.

That fear alone can move markets aggressively.

And right now, markets are beginning to price the possibility that geopolitical instability may last longer than initially expected.

Oil Prices Are Becoming the Main Macro Variable Again

One of the clearest changes happening in markets right now is that oil is slowly moving back to the center of the macroeconomic conversation.

For months, investors were almost entirely focused on:

- AI growth.

- Technology earnings.

- Rate-cut expectations.

- Liquidity optimism.

- Equity momentum.

But geopolitical crises have a way of rapidly changing market priorities.

And higher oil prices change everything.

Following stalled diplomatic talks between Iran and the United States, crude prices surged again as traders began pricing a higher geopolitical risk premium into energy markets. The issue is not simply today’s oil supply. The issue is uncertainty around future supply.

Markets always move ahead of reality. If investors believe disruptions could worsen later, prices rise immediately. That is exactly what we are seeing now.

And once oil begins rising aggressively, the effects spread across the entire economy.

Why Higher Oil Prices Become Dangerous for Equities

The first impact of higher oil is relatively obvious:

Companies face rising costs. Transportation becomes more expensive. Manufacturing margins tighten. Logistics costs increase. Consumer purchasing power weakens.

But the second-order effects are far more important. Because once energy prices rise enough, inflation expectations start moving higher again. And inflation expectations influence everything.

Higher inflation expectations can lead to:

- Higher Treasury yields.

- More restrictive Federal Reserve policy.

- Delayed interest-rate cuts.

- Tighter financial conditions.

- Lower equity valuations.

This is where markets become vulnerable.

Because today’s equity market is heavily dependent on liquidity and optimistic growth assumptions.

And expensive markets tend to react aggressively when inflation risks return unexpectedly.

The Federal Reserve May Become the Most Important Variable

One of the biggest reasons the S&P 500 rallied so aggressively earlier this year was the belief that inflation was gradually cooling and the Fed would eventually move toward rate cuts.

But geopolitical energy shocks complicate that narrative.

If oil remains elevated for an extended period, inflation may prove much stickier than markets currently expect.

And if inflation remains sticky:

- The Fed may keep rates higher for longer.

- Financial conditions may remain tight.

- Bond yields may continue rising.

- Equity multiples may compress.

This creates a difficult environment for growth stocks, especially technology companies whose valuations are highly sensitive to discount rates.

And that is why markets are suddenly paying so much attention to every geopolitical headline involving Iran.

Because investors understand that oil can directly influence Federal Reserve policy expectations.

Why the S&P 500 Has Stayed Surprisingly Strong

Despite all these risks, the S&P 500 continues showing impressive resilience.

Honestly, that resilience says a lot about how powerful the current bullish narrative still is.

Mega-cap technology companies continue dominating market flows thanks to:

- Strong earnings growth.

- AI optimism.

- Massive cash reserves.

- Structural productivity expectations.

- Investor concentration into perceived “safe growth”.

These companies have effectively carried large portions of the index higher. And as long as earnings remain strong, markets can continue tolerating a certain amount of geopolitical noise.

But there is an important warning here. The stronger markets become, the more vulnerable they also become to disappointment. Because when valuations are elevated, perfection gets priced in very quickly.

And once markets price perfection, even relatively small macro shocks can trigger violent reactions.

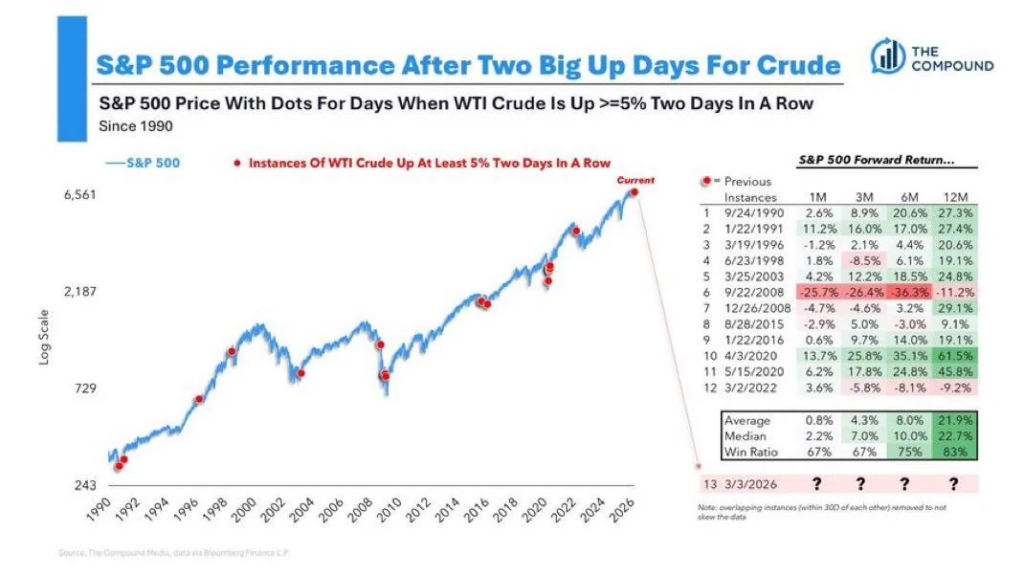

Oil Spikes vs S&P 500 Corrections Since 2000

Historically, prolonged oil shocks eventually pressure equities through inflation, bond yields and tighter financial conditions.

Which Sectors Could Benefit And Which Could Suffer

Potential Winners

Energy Stocks

Oil producers naturally benefit from higher crude prices. If tensions escalate further, energy companies could continue outperforming broader markets.

Defense Companies

Geopolitical instability often increases military spending expectations, supporting defense-related stocks.

Commodity Producers

Certain commodity-linked firms may benefit if global raw-material prices continue rising.

Most Vulnerable Sectors

Airlines and Transportation

Fuel costs are one of the biggest risks for transport-related businesses.

Consumer Discretionary

Higher gasoline and energy prices reduce household purchasing power.

Industrials and Manufacturing

Rising input costs can pressure profit margins significantly.

Small Caps

Smaller companies generally struggle more when financial conditions tighten.

Why Markets Have Become So Headline-Driven

One of the most noticeable changes in recent months is how quickly markets react to geopolitical developments. Negotiation headlines. Military activity. Sanctions. Shipping disruptions. Diplomatic comments.

Everything moves markets almost instantly now.

This type of “headline volatility” usually appears when markets are strong fundamentally but nervous underneath. And honestly, that describes the current environment perfectly. Investors are not fully bearish. But they are becoming increasingly aware that risks are rising.

That creates a fragile equilibrium where sentiment can shift extremely quickly.

Temporary Oil Spike or the Start of Something Bigger?

This may be the single most important question for markets right now. If rising oil prices prove temporary, the S&P 500 can probably continue climbing as long as earnings remain strong and inflation eventually cools again. Markets have historically looked through short-term geopolitical volatility.

But if oil moves toward sustained levels near or above $110 per barrel, the situation changes dramatically.

At that point:

- Inflation expectations could rise sharply.

- Rate-cut hopes could disappear.

- Corporate margins could weaken.

- Consumer spending could slow.

- Bond yields could rise further.

- Equity valuations could compress.

And suddenly, markets would no longer be pricing a temporary disruption.

They would begin pricing a broader macroeconomic slowdown.

The Bond Market May Decide Everything

While most investors focus on equities and oil, bond markets may ultimately determine the next major move. If Treasury yields continue climbing because of inflation fears, financial conditions tighten automatically. That matters enormously because modern equity markets depend heavily on liquidity. Higher yields increase the discount rate applied to future earnings. And that particularly affects high-growth sectors. This is why the relationship between oil, inflation and bond yields is becoming so important.

The S&P 500 is not just reacting to geopolitics directly. It is reacting to how geopolitics may reshape monetary policy and liquidity conditions.

Historical Perspective: Markets Have Seen This Before

History shows that geopolitical crises involving energy supply often follow similar market patterns.

1970s Oil Shocks

One of the clearest examples of energy-driven inflation destabilizing markets and central banks.

Gulf War Period

Oil initially surged aggressively before stabilizing once markets believed supply disruptions would remain manageable.

Russia-Ukraine Conflict

Energy became the transmission mechanism through which geopolitics impacted inflation, central-bank policy and global growth expectations. And honestly, that last comparison may be the most relevant.

Because today’s market is once again realizing that energy prices can rapidly reshape the entire macroeconomic environment.

Three Forces Will Decide the Next Move in the S&P 500

At this stage, the outlook for equities depends primarily on three interconnected variables:

1. Oil Prices

If crude stabilizes, markets may regain confidence quickly. If oil spikes further, inflation fears will intensify.

2. Federal Reserve Policy

The more restrictive the Fed remains, the more pressure expensive equity valuations may face.

3. Corporate Earnings

As long as mega-cap earnings remain strong, markets retain an important structural support mechanism. But if earnings weaken while inflation rises, the market environment could deteriorate rapidly.

Final Thoughts

The S&P 500 still looks fundamentally strong. Artificial intelligence, corporate earnings and structural technology growth continue providing enormous support for equities.

But Wall Street is no longer operating inside a purely bullish macro environment. Geopolitical risk is returning. Oil prices are rising again. Inflation fears are re-emerging. And the Federal Reserve may be forced to stay restrictive longer than markets hope.

From my perspective, this creates one of the most important balancing acts markets have faced in months.

Because as long as tensions between Iran and the United States remain contained, the S&P 500 can likely continue relying on its powerful structural growth narrative. But if energy markets become destabilized for a prolonged period, the situation changes quickly.

At that point, geopolitics stops being background noise. And starts becoming the main macro driver behind global markets again.

FAQs

Why do tensions between Iran and the United States affect the S&P 500?

Because geopolitical tensions can disrupt global energy markets, raise oil prices and increase inflation fears. That eventually affects Federal Reserve policy, bond yields and corporate earnings expectations.

Why is oil so important for stock markets?

Oil impacts transportation, manufacturing and consumer spending. Rising energy prices can reduce profit margins and pressure economic growth.

Could higher oil prices delay Fed rate cuts?

Yes. If inflation rises again because of energy costs, the Federal Reserve may keep interest rates higher for longer.

Which sectors benefit the most from geopolitical tensions?

Energy producers, defense companies and some commodity-related businesses usually benefit when geopolitical risk pushes commodity prices higher.

Which sectors are most vulnerable?

Airlines, industrials, transportation companies and consumer discretionary stocks are often the most exposed to rising fuel and input costs.

Is the S&P 500 still bullish despite geopolitical risks?

Yes, structurally the market remains strong because of AI optimism and strong mega-cap earnings. However, elevated valuations also make the market more sensitive to macroeconomic shocks.

Why are markets reacting so quickly to headlines now?

Because investors understand that geopolitical tensions can rapidly influence inflation, oil prices and central-bank policy expectations.

What happens if oil moves above $110 per barrel?

Markets could begin pricing a much more serious inflation shock, potentially leading to higher bond yields, tighter financial conditions and broader equity-market weakness.

Is this similar to previous oil crises?

There are similarities with historical periods such as the 1970s oil shocks and the Russia–Ukraine energy crisis, where energy prices heavily influenced inflation and market sentiment.

What is the most important thing investors should watch now?

Oil prices, Treasury yields and Federal Reserve expectations remain the three most important macro variables driving equities.