Why lithium, copper, rare earths, uranium and critical minerals are becoming the new backbone of the global economy

Traditional commodities are no longer the whole story.

For decades, global markets were dominated by oil, gas, gold, wheat, copper and other classic raw materials. They still matter. Oil still moves inflation. Gold still reflects fear, real rates and monetary uncertainty. Wheat still matters for food security. Copper still acts as a barometer of industrial activity.

But a new generation of strategic commodities is now moving toward the center of the global economy.

Lithium, rare earths, graphite, gallium, magnesium, uranium, nickel, cobalt and high-demand copper are no longer just technical inputs for engineers or industrial supply chains. They are becoming macroeconomic assets.

The reason is simple: the world is electrifying, digitizing and rearming at the same time.

This is why strategic commodities are no longer a niche story. They are becoming one of the most important macro themes of the decade.

According to the International Energy Agency, electricity demand from data centers surged 17% in 2025, while AI-focused data centers grew even faster. The IEA also expects global electricity demand growth to accelerate to an average of 3.6% per year between 2026 and 2030, compared with 2.8% over the previous decade.

That matters because AI is not just a software revolution. It is also a commodity, energy and infrastructure story.

What Is Really Happening

The market is slowly realizing that critical minerals are not just raw materials. They are strategic bottlenecks.

In the old commodity cycle, investors mostly focused on supply, demand, inventories, interest rates and global growth. That still matters. But the new commodity cycle is different.

Today, the key question is not only:

Will demand rise this year?

The deeper question is:

Which materials are essential for the next economic system?

That changes everything.

A commodity becomes strategically important when it is difficult to replace, geographically concentrated, politically sensitive or essential for critical infrastructure. That is exactly what is happening with lithium, copper, rare earths, uranium, graphite, gallium and magnesium.

These materials sit at the intersection of several major forces:

AI infrastructure

Data centers

Power grids

Electric vehicles

Battery storage

Renewable energy

Defense spending

Semiconductors

Nuclear power

Geopolitical fragmentation

Supply-chain security

This is why governments are moving fast.

Spain, for example, approved its First Action Plan for the Sustainable Management of Mineral Raw Materials 2026–2030, linked to €414 million in public investment. The plan focuses on autonomy, industrial development, circularity and sustainable management.

Brazil is also moving in the same direction. Its government has been working on new regulation for critical minerals, with a focus on sovereignty, attracting investment and increasing domestic processing without relying mainly on large tax breaks.

This tells us something important: critical minerals are no longer just a mining issue. They are becoming an industrial policy issue.

The New Strategic Commodity Chain

| Macro Trend | Required Infrastructure | Key Commodities |

|---|---|---|

| Artificial Intelligence | Data centers, chips, electricity | Copper, gallium, rare earths, uranium |

| Energy Transition | Batteries, EVs, grids, renewables | Lithium, graphite, nickel, copper |

| Defense Spending | Missiles, radar, electronics, magnets | Rare earths, gallium, titanium |

| Nuclear Revival | Reactors, fuel cycle, stable baseload power | Uranium |

| Supply-Chain Security | Domestic refining, recycling, processing | Lithium, magnesium, rare earths |

AI, electrification and geopolitical risk are turning critical minerals into strategic macro assets.

Why AI Is Changing the Commodity Market

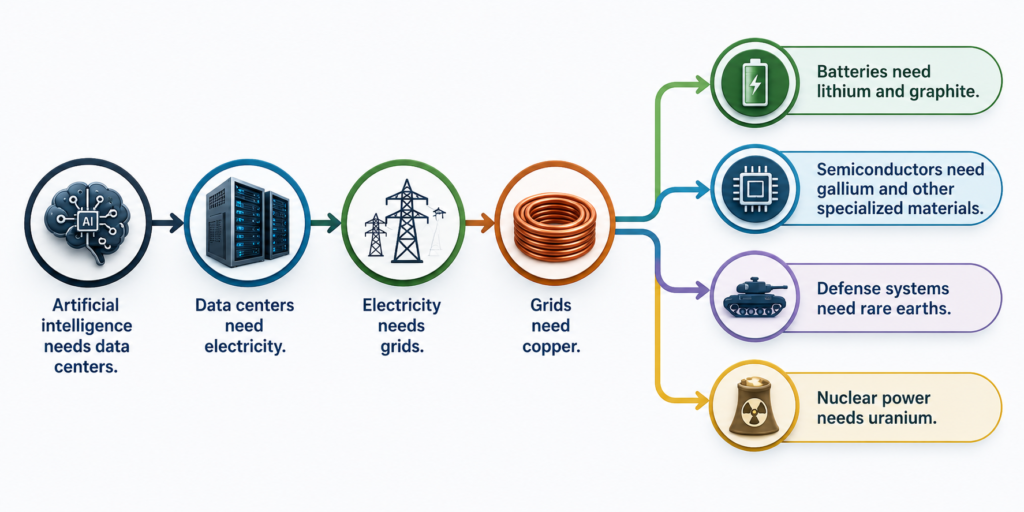

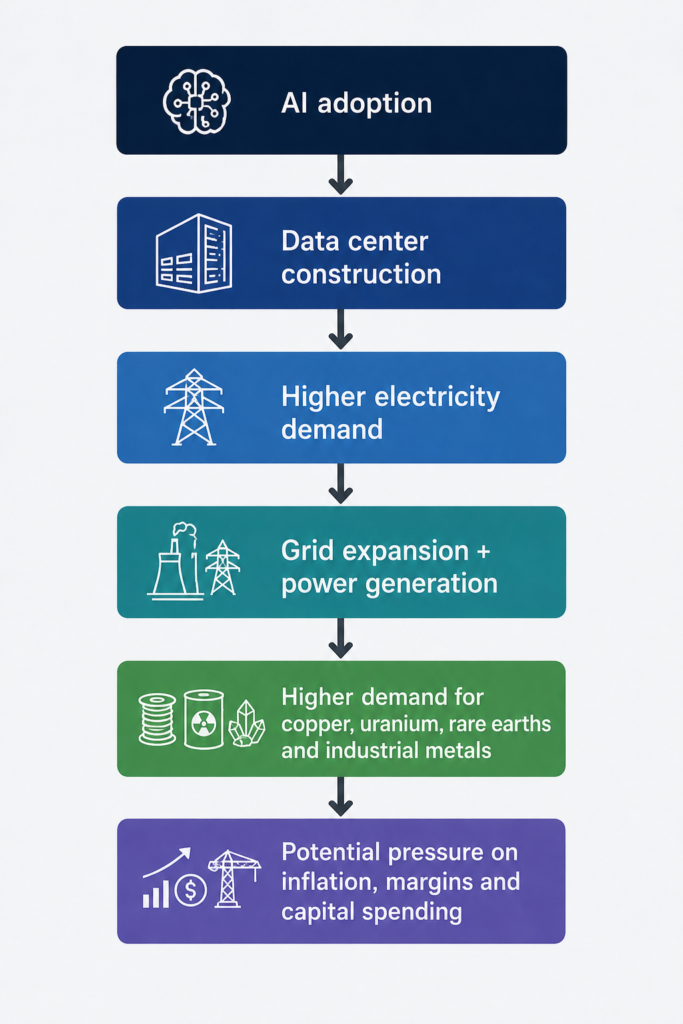

Artificial intelligence looks digital from the outside, but physically it is very resource-intensive.

Every AI model needs chips. Every chip needs advanced manufacturing. Every data center needs land, electricity, cooling systems, transformers, power lines and backup energy. Every grid expansion needs massive amounts of copper and other industrial materials.

This is the part of the AI boom that markets are still trying to price correctly.

AI may be deflationary in the long term if it boosts productivity, automates workflows and reduces labor costs. But in the short and medium term, it can also be inflationary in specific sectors because it increases demand for electricity, construction, chips, cooling systems and critical minerals.

That creates a very interesting macro contradiction:

AI may reduce costs in software, services and labor-intensive industries. But it may increase costs in power, infrastructure, metals and energy systems.

This is why the AI boom is not only bullish for technology companies. It may also create long-term demand for commodity producers, grid operators, nuclear energy, copper miners and companies exposed to critical mineral processing.

The U.S. Energy Information Administration recently projected that U.S. power consumption will hit new record highs in 2026 and 2027, partly because of demand from AI data centers and crypto operations.

That is a major signal.

AI is becoming a power-demand story.

AI Demand Transmission Into Commodities

The AI boom moves from software into physical infrastructure.

The Most Important Strategic Commodities to Watch

| Commodity | Why It Matters | Main Macro Link | Key Risk |

|---|---|---|---|

| Copper | Power grids, data centers, electrification | Infrastructure inflation | Supply disruptions |

| Lithium | Batteries, EVs, energy storage | Energy transition | Price volatility |

| Rare Earths | Magnets, defense, wind turbines, electronics | Geopolitical risk | Concentrated supply |

| Uranium | Nuclear energy and firm power demand | Energy security | Political regulation |

| Graphite | Battery anodes and energy storage | EV supply chains | Processing concentration |

| Gallium | Semiconductors and advanced electronics | AI and chip production | Export controls |

| Magnesium | Industrial alloys and manufacturing | Industrial competitiveness | Supply dependence |

This is where the market story becomes much bigger than simple commodity speculation.

Copper is no longer only a “China growth” trade. It is also an AI grid trade, an electrification trade and an infrastructure trade.

Uranium is no longer only a nuclear energy story. It is increasingly tied to the need for stable electricity as data centers demand reliable baseload power.

Rare earths are no longer only an industrial input. They are a geopolitical weapon because they are essential for defense systems, magnets, electronics and renewable technologies.

Lithium is no longer only an EV material. It is part of the broader battery storage system required to stabilize renewable-heavy power grids.

Copper: The Commodity at the Center of the New Economy

If there is one commodity that best represents this new cycle, it is copper.

Copper is used in power grids, electrical wiring, transformers, renewable energy, electric vehicles, data centers and industrial infrastructure. It is not glamorous, but it is everywhere.

That is why copper is often called “Dr. Copper” because it has historically reflected the health of the global economy. But copper may now be evolving into something even more important: the metal of electrification.

Goldman Sachs has maintained its 2026 copper price forecast at $12,650 per metric ton, while also warning about possible supply risks linked to sulfuric acid shortages, logistics disruptions and exposure in countries such as Chile and the Democratic Republic of the Congo.

This is important because copper supply chains are not simple.

Mining is slow.

Permitting is slow.

Refining is concentrated.

Logistics can be disrupted.

Political risk can rise quickly.

If AI and electrification demand rise faster than supply can respond, copper could become one of the most important inflation-sensitive commodities of the next decade.

Strategic Commodity Sensitivity Map

| Commodity | AI Exposure | Energy Transition Exposure | Geopolitical Risk | Inflation Impact |

|---|---|---|---|---|

| Copper | High | Very High | Medium | High |

| Lithium | Medium | Very High | Medium | Medium |

| Rare Earths | High | High | Very High | Medium |

| Uranium | Medium | High | High | Medium |

| Gallium | Very High | Medium | Very High | Medium |

| Graphite | Medium | High | High | Medium |

Not all commodities react to the same macro forces. Some are more exposed to AI, others to energy security or geopolitical fragmentation.

Why This Matters for Inflation

The most important macro question is not whether critical minerals will go up in a straight line. They will not. These markets are volatile. Prices can crash when supply comes online or when demand slows. Lithium is a good example: even a long-term bullish story can experience brutal short-term corrections.

The real macro issue is different. If critical minerals become more expensive or harder to access, they can raise the cost of building the next economy.

That can affect:

data center construction

electricity infrastructure

EV production

battery storage

semiconductor supply chains

renewable energy deployment

defense manufacturing

industrial competitiveness

This matters for inflation because modern inflation is not only about wages, oil or food. It can also come from bottlenecks in strategic supply chains.

If the world wants more AI, more electrification, more defense capacity and more energy security at the same time, the pressure on raw materials could become persistent. That does not mean inflation will explode automatically. But it does mean the disinflationary impact of technology may be partially offset by the physical cost of scaling that technology.

In simple terms:

AI may reduce the cost of intelligence. But it may increase the cost of electricity, metals and infrastructure.

That is the macro tension investors need to understand.

Why Governments Are Treating Commodities Like National Security Assets

The most important shift is control.

In the past, many countries were comfortable relying on global supply chains. If a country needed minerals, components or refined materials, it could import them.

That model is now under pressure.

The pandemic, the war in Ukraine, tensions in the Middle East, U.S.-China rivalry and export restrictions have changed how governments think about supply chains.

Critical minerals are now viewed through the lens of national security.

The question is no longer only:

Can we buy it cheaply?

The new question is:

Can we access it reliably during a crisis?

That is why countries are building strategic partnerships, subsidizing domestic production, supporting recycling, encouraging refining capacity and trying to reduce dependence on concentrated suppliers.

This is also why geopolitical risk is becoming embedded in commodity pricing.

A rare earth is not just a rare earth.

It is a defense input.

A chip input.

An energy transition input.

A geopolitical bargaining chip.

That makes the market more complex and potentially more volatile.

Investment Implications

For investors, this theme is not as simple as buying every commodity linked to AI or the energy transition. That would be a mistake. Strategic commodities can have strong long-term demand but still suffer sharp price declines if supply increases, inventories rise or global growth slows.

The better approach is to think in layers.

1. Direct commodity exposure

This includes copper, uranium, lithium, rare earths and other critical minerals. Potential upside exists if demand exceeds expectations or supply becomes constrained. But volatility is high.

2. Mining and processing companies

Companies with strong reserves, low production costs, political stability and refining capacity may benefit more than pure commodity exposure.

Processing matters because the world does not only need minerals. It needs usable, refined, industrial-grade materials.

3. Infrastructure and grid companies

If AI and electrification increase electricity demand, grid investment becomes essential. This could benefit utilities, power equipment companies, transformer manufacturers and infrastructure firms.

4. Nuclear and uranium supply chains

If data centers require reliable baseload power, nuclear energy could become more attractive. That would support uranium demand and nuclear infrastructure investment.

5. Technology companies with supply-chain control

Large AI and semiconductor companies may increasingly focus on securing energy and material inputs. The winners may not only be the companies with the best models, but also those with the most resilient infrastructure.

The Key Risk: Markets May Overprice the Story

There is one major warning. Whenever a structural trend becomes popular, markets can overprice it.

We saw this with clean energy stocks. We saw it with lithium. We saw it with parts of the EV supply chain. We may see it again with AI-linked commodities.

A strong long-term story does not guarantee a straight-line investment return. Prices can fall even when the long-term thesis remains intact. That is why investors need to separate three things:

- The long-term structural trend.

- The current valuation.

- The short-term supply-demand balance.

A commodity can be strategically important and still be temporarily oversupplied. That is especially true for lithium, nickel and some battery materials, where supply cycles can move faster than demand expectations.

Copper and uranium may have different dynamics because supply growth is harder, slower and more politically sensitive.

Practical Reading for Investors and Policymakers

The old commodity question was:

Is global growth accelerating or slowing?

The new commodity question is:

Which resources are indispensable for AI, energy security and industrial sovereignty?

That is the real shift.

Strategic commodities are no longer priced only by current consumption. They are increasingly priced by future dependency.

That means investors, companies and governments need to ask:

Is this resource essential for critical infrastructure?

Is supply concentrated in a small number of countries?

Can it be substituted?

Can it be recycled efficiently?

Is processing capacity diversified?

Could export restrictions affect supply?

Is demand linked to public policy or private-sector capex?

Could AI and electrification accelerate demand faster than expected?

If the answer points to scarcity, strategic dependence or limited substitution, that commodity may become much more important over time.

Conclusion: Commodities Are Becoming Instruments of Power

The rise of strategic commodities is one of the most important macro stories of the decade.

Artificial intelligence, data centers, electrification, defense spending, renewable energy, nuclear power and geopolitical fragmentation are all pushing the global economy toward a new resource map.

Oil and gold will still matter.

But they are no longer the only macro commodities that investors need to watch.

Copper, lithium, uranium, rare earths, graphite, gallium and magnesium are becoming part of the invisible backbone of the modern economy.

The deeper story is not just demand.

It is control.

Control over extraction.

Control over processing.

Control over refining.

Control over trade routes.

Control over energy supply.

Control over the industrial base.

Countries and companies that secure stable access to strategic commodities may gain a major advantage in the next phase of global competition. Those that fail to do so may face higher costs, weaker supply chains and lower industrial resilience.

From my perspective, this is why strategic commodities should not be treated as a small mining story. They are becoming a macro story. And possibly one of the most important investment and geopolitical themes of the next decade.

FAQs

What are strategic commodities?

Strategic commodities are raw materials considered essential for the functioning of modern economies, critical infrastructure and national security. These include lithium, copper, uranium, rare earths, graphite, gallium and other minerals used in AI infrastructure, energy systems, semiconductors, batteries and defense technologies.

Why are critical minerals becoming more important in 2026?

Critical minerals are gaining importance because several global trends are accelerating simultaneously:

- Artificial intelligence and data centers

- Electrification and electric vehicles

- Renewable energy deployment

- Nuclear energy expansion

- Defense spending

- Geopolitical fragmentation

All of these sectors require large amounts of specialized materials and stable supply chains.

How does artificial intelligence affect commodity demand?

AI increases demand for physical infrastructure.

Large AI models require:

- advanced semiconductors

- data centers

- electricity grids

- cooling systems

- backup energy capacity

This creates higher demand for copper, uranium, rare earths, gallium and other industrial materials linked to energy and technology infrastructure.

Why is copper considered one of the most important strategic commodities?

Copper is essential for:

- power grids

- electrical wiring

- renewable energy systems

- electric vehicles

- transformers

- AI-related data center infrastructure

Because electrification requires massive grid expansion, copper demand is expected to remain structurally strong over the next decade.

Why are rare earths strategically important?

Rare earth elements are critical for:

- magnets

- semiconductors

- military systems

- wind turbines

- advanced electronics

Their importance is amplified by the fact that global supply and refining are highly concentrated geographically, increasing geopolitical risk.

Could strategic commodities contribute to inflation?

Yes.

If critical minerals become more expensive or supply becomes constrained, they can increase costs across:

- manufacturing

- infrastructure

- energy systems

- semiconductor production

- transportation

- defense industries

This could create long-term structural inflationary pressure in certain sectors of the economy.

Why is uranium attracting more attention again?

Uranium is benefiting from renewed interest in nuclear energy.

As AI data centers increase electricity demand, governments and companies are searching for reliable baseload power sources. Nuclear energy offers stable electricity generation without direct carbon emissions, making uranium strategically relevant again.

How are governments responding to the critical mineral race?

Many governments are:

- increasing domestic mining investment

- supporting refining and recycling

- reducing dependency on foreign suppliers

- creating strategic partnerships

- implementing industrial policies around critical minerals

This reflects growing concerns over supply-chain security and economic sovereignty.

Are strategic commodities a long-term investment theme?

Potentially yes, but volatility remains high.

The long-term structural demand story appears strong due to AI, electrification and infrastructure expansion. However, commodity markets can still experience sharp corrections caused by:

- oversupply

- weaker global growth

- changing regulations

- speculative excesses

Investors need to distinguish between long-term trends and short-term price cycles.

What is the biggest macroeconomic implication of this trend?

The biggest implication may be that commodities are evolving from simple economic inputs into strategic geopolitical assets.

Control over extraction, refining and supply chains could increasingly influence:

- inflation dynamics

- industrial competitiveness

- energy security

- technological leadership

- geopolitical power

In other words, the next phase of global economic competition may depend as much on access to critical minerals as on traditional financial strength.