In the global economy today, few topics get as much attention as inflation. Central bankers from major economies have in recent days been repeating a message that is beginning to be taken a little more seriously by markets: the fight against inflation is not over. Although price growth is showing signs of moderation, policymakers are wary that premature decisions could unravel years of progress.

What is striking from my position is not merely the continued inflation but the shift in tone. One year ago, it was how fast rates should rise. Now it’s about how long they have to stay high and that’s a very different kind of challenge.”

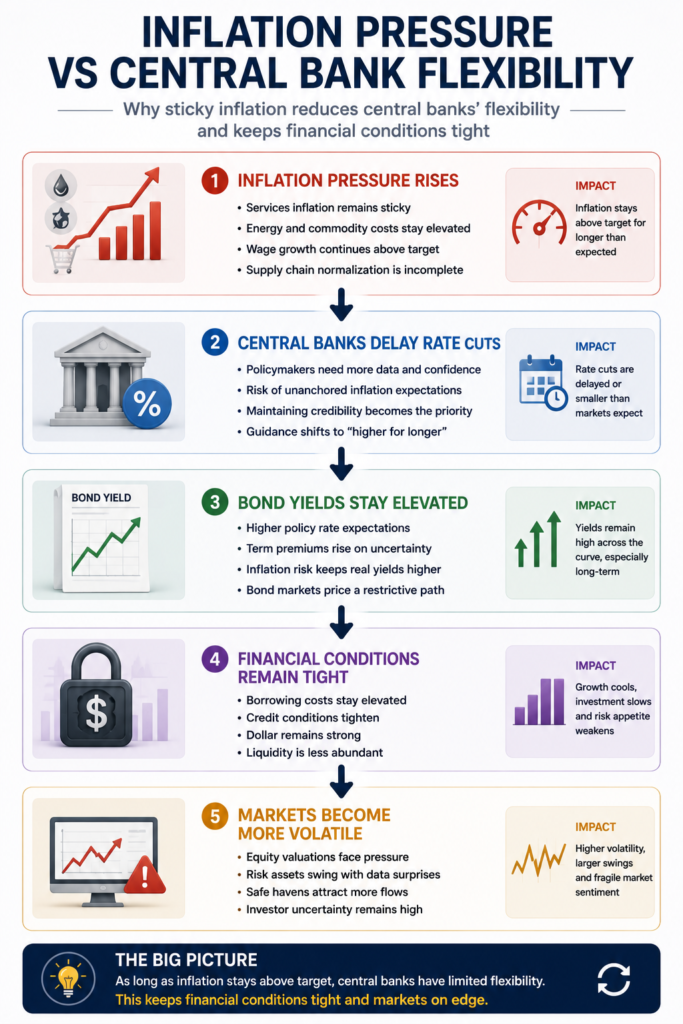

Inflation Pressure vs Central Bank Flexibility

Why Central Banks Are Losing Flexibility

One of the biggest macroeconomic problems in 2026 is that central banks are finding it increasingly difficult to regain flexibility.

For most of the last year, markets expected inflation to continue cooling steadily, allowing central banks to gradually pivot toward lower interest rates. But reality has become more complicated.

Inflation is no longer being driven only by temporary supply-chain disruptions or post-pandemic distortions. Instead, several structural forces continue keeping price pressures more persistent than policymakers expected.

Those forces include:

- Energy volatility.

- Wage pressure.

- Geopolitical fragmentation.

- Supply-chain reshoring.

- Rising commodity costs.

- And elevated government spending.

This creates a very difficult situation for central banks. If they cut interest rates too early, inflation could accelerate again and damage credibility. But if they keep rates restrictive for too long, they risk slowing the economy too aggressively and tightening financial conditions further.

From my perspective, this is why markets have become increasingly sensitive to every inflation report, labor-market release and central bank speech.

Investors understand that policymakers are trapped between:

- Inflation persistence.

- Slowing growth.

- And financial stability risks.

The Federal Reserve faces this dilemma very clearly.

The U.S. economy remains relatively resilient, but services inflation and wage growth have stayed sticky. That means the Fed cannot confidently declare victory over inflation yet. The European Central Bank faces an even more complex environment because weak economic growth is colliding with persistent inflationary pressure. And in Japan, the Bank of Japan continues dealing with imported inflation risks caused by yen weakness and global energy costs.

This is why financial markets may continue experiencing:

- Higher volatility.

- Unstable bond yields.

- Shifting rate-cut expectations.

- And sudden changes in risk appetite.

The era of ultra-predictable central bank policy may be ending.

And from a macro perspective, that changes everything for:

- Equities.

- Bonds.

- Real estate.

- Commodities.

- And crypto markets.

A Slowing Trend… But Not Enough

Inflation has certainly retreated from its peak levels. Headline inflation, driven heavily by energy and food, has eased as global supply chains stabilize and energy markets become less volatile. This has provided some respite to households and policymakers alike.

But the real concern is what’s referred to in the economist community as core inflation the underlying measure that strips out volatile components like food and energy. This metric has been much more stubborn. It reflects deeper structural pressures in the economy, especially:

- Persistent wage growth

- Rising costs in the services sector

- Strong consumer demand in certain areas

These factors suggest that inflation is no longer just a temporary shock but has become embedded in the system. And that’s exactly what central banks are trying to avoid.

Central Banks Choose Patience Over Speed

Institutions such as the Federal Reserve and the European Central Bank have been clear that the aggressive pace of rate hikes may be over but the restrictive phase is far from over.

Interest rates remain high and policymakers are signalling they are prepared to keep them there for longer than expected. The goal is simple, yet difficult: to return inflation sustainably to target levels that are usually around 2%, without triggering a sharp economic slowdown.

This balancing act is a fine one. Cut rates too quickly and inflation could come roaring back. If they remain too high for too long, economic growth could stall.

The Real-World Impact of High Interest Rates

The impact of high interest rates over a longer period is increasingly being felt in the economy.

Borrowers pay more to consumers. Credit cards, personal loans and especially mortgages now cost considerably more. This has started to temper spending, especially on large purchases and discretionary goods.

For businesses, the environment is also shifting. Companies are reassessing:

- Investment plans

- Hiring strategies

- Expansion projects

The cost of capital has risen, making it harder to justify riskier or long-term investments. As a result, economic activity is beginning to cool not dramatically, but noticeably.

The housing market is one of the clearest examples. Highly sensitive to interest rates, it has shown signs of slowing in multiple regions, with reduced transaction volumes and more cautious buyers.

A Surprisingly Resilient Labor Market

Labour markets in many developed economies remain tight despite the tighter financial conditions. Employment levels are relatively high and there are still shortages of labour in some sectors.

The resilience is positive at first sight it supports household income and helps sustain demand. But it is also a threat for the central bank.

A tight labor market can push up wages, which is good for workers but can also add to inflation, especially in services. Strong employment feeds into the inflationary spiral, forcing central banks to stick to restrictive policies

Lessons From the Past Shape Today’s Decisions

A common theme of recent policy-maker statements is the need to avoid repeating past mistakes. In the past, central banks have sometimes been too quick to ease policy after initial success in bringing inflation down, and seen it return with a vengeance.

Officials seem intent not to repeat that mistake this time. It’s all about credibility, so markets and the public can be assured that inflation will be brought under control and stay there.

For me, this is where the psychology of monetary policy becomes as important as the numbers. Expectations cause behavior, and behavior causes inflation. If people expect prices to continue to rise, they act on that expectation and it can become a self-fulfilling prophesy.

Markets Adjust to a “Higher for Longer” Reality

Financial markets have responded quickly to this change in tone. A few months ago, investors had generally expected interest rate cuts in the near term. That expectation has now been pushed further into the future.

This re-evaluation has led to greater volatility, particularly in bond markets where yields are responsive to changing expectations about future rates. We’ve also seen a reaction in the equity markets with some volatility in interest rate sensitive sectors like technology and real estate.

At the same time, investors are recalibrating their strategies, focusing more on:

- Defensive assets.

- Stable cash flows.

- Companies with strong balance sheets.

The era of easy money is clearly behind us, at least for now.

Global Uncertainty Adds Complexity

The global environment adds to the uncertainty surrounding inflation. Geopolitical tensions, energy prices swings and ongoing supply chain adjustments are all likely to have an impact on inflation in unforeseen ways.

These external variables mean that central banks have to stay flexible. Even while taking a restrictive stance, they are ready to move quickly to adjust policy if conditions change.

Europe’s Unique Challenge

In Europe, the situation is particularly complex. Economic growth has been weaker compared to other regions, limiting the room for aggressive monetary tightening.

The European Central Bank faces a difficult trade-off:

- Raise rates too much → risk deepening the slowdown.

- Lower rates too soon → risk reigniting inflation.

This delicate balance explains the cautious, incremental approach that European policymakers have adopted. Every decision is carefully calibrated, with an emphasis on avoiding extreme outcomes.

Households and Businesses Feel the Pressure

The economic climate for households remains difficult. Inflation has come down from its peak, but the cost of living is still high. Food, housing and services continue to be essential items that strain budgets.

Many families are altering their spending habits, concentrating on essentials and cutting discretionary spending. The change is small but pervasive, and it is an important driver of aggregate economic activity.

Businesses, meanwhile, are operating in an increasingly uncertain landscape. Demand is slowing, financing is more expensive and future conditions are harder to predict. The result has been a more restrained attitude to investment and expansio

What Comes Next?

Looking ahead, the trajectory of inflation will remain the single most important factor guiding monetary policy. Central banks will continue to monitor:

- Wage growth.

- Core inflation trends.

- Consumer demand.

- Global economic conditions.

Any significant deviation from expectations could prompt a shift in strategy, whether toward further tightening or, eventually, easing.

Conclusion: A Defining Moment for Monetary Policy

The world economy is at a critical crossroads and the decisions taken by central banks will shape the path of growth and stability for years to come. Inflation is slowing but not under control and policy makers know it.

What makes this moment so hard is the need to balance competing risks: to contain inflation without causing a recession, to keep credibility without over-tightening, to react to data without overreacting.

If anything seems clear, it is that we are in a period of transition. The easy answers are gone and every decision matters. Central banks are being cautious, deliberate and clear-eyed about the fact that the road ahead is not straightforward.

FAQs

Why is inflation becoming persistent again?

Inflation remains persistent because of structural factors like energy volatility, wage growth, geopolitical tensions, supply-chain restructuring and commodity pressure.

Why are central banks delaying rate cuts?

Central banks fear that cutting rates too early could allow inflation to rise again and damage their credibility.

Why do markets react so strongly to inflation data?

Because inflation directly affects interest rates, bond yields, liquidity conditions and the future direction of monetary policy.

How does inflation affect bond yields?

Higher inflation expectations usually push bond yields higher because investors demand more compensation for inflation risk.

Why are higher bond yields important for stocks?

Higher yields increase borrowing costs and reduce the attractiveness of future corporate earnings, which can pressure equity valuations.

Why do crypto markets care about inflation?

Crypto markets are highly sensitive to liquidity conditions. Persistent inflation can delay rate cuts and tighten financial conditions, creating pressure on speculative assets.

What does “higher for longer” mean?

It refers to the possibility that central banks may keep interest rates elevated for a much longer period than markets previously expected.

Why is the Federal Reserve in a difficult position?

Because the Fed must balance inflation control with economic growth and financial stability at the same time.

Could central banks still cut rates later in 2026?

Yes, but markets increasingly believe cuts may arrive later and more gradually than originally expected.