Donald Trump’s latest threat against Iran is not just another geopolitical headline. I see it as a full macro event.

That matters because markets do not wait for formal declarations of war. They move on risk, probabilities, shipping routes, inflation expectations, and central bank reactions. And right now, Trump’s warning that Iran has taken too long to negotiate combined with renewed U.S.-Iran military exchanges near the Strait of Hormuz lands directly on the most sensitive nerve in the global economy: energy.

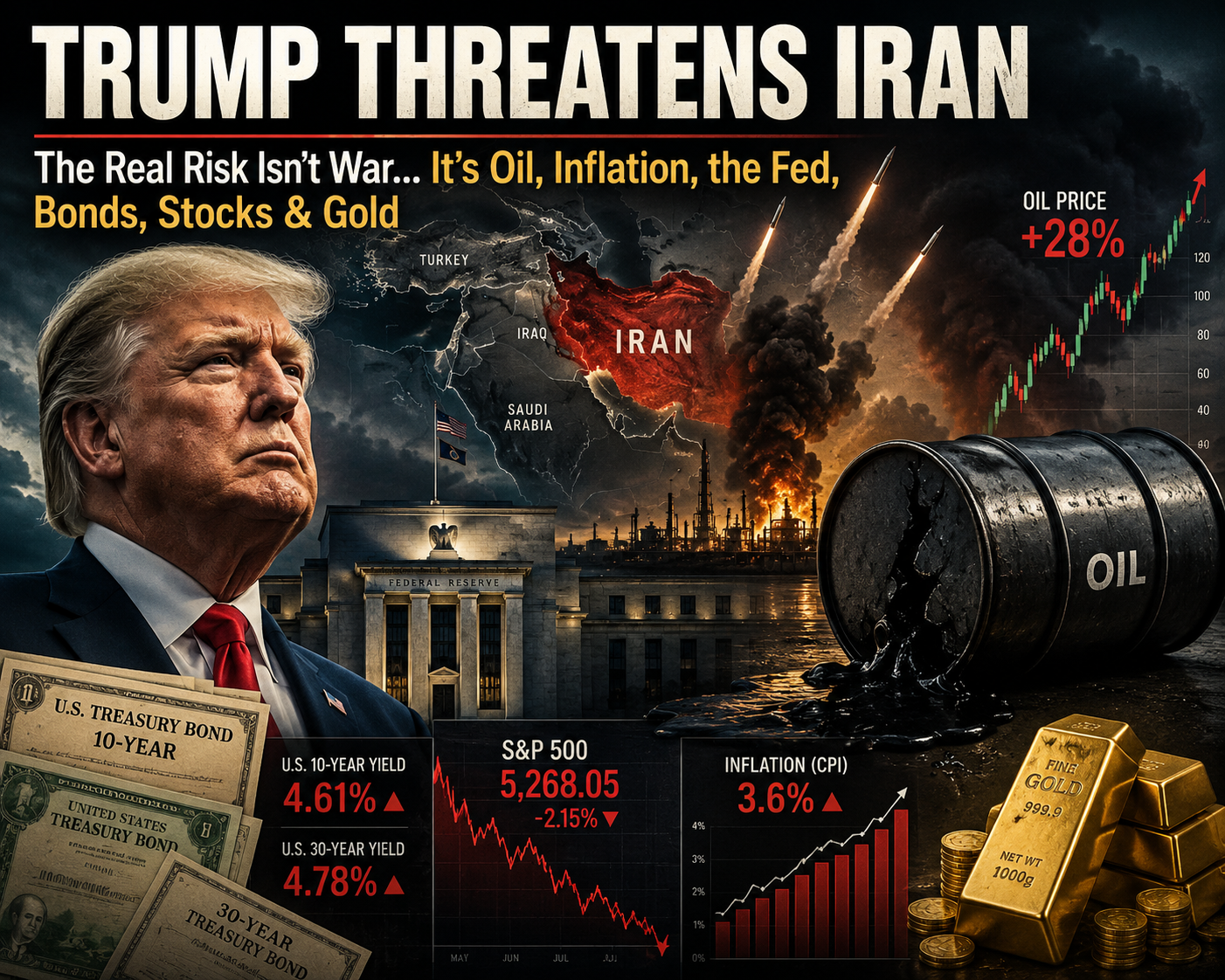

According to Reuters, oil prices jumped after Trump threatened a heavy response against Iran, with Brent settling above $93 a barrel and U.S. crude around $90 as traders priced in renewed geopolitical risk and supply concerns. RTVE reported that Trump said the U.S. could attack Iran “with force” if Tehran does not sign a peace agreement, while also pointing to possible strikes on power plants and bridges.

That is why I do not read this story only as “Trump threatens Iran.” I read it as a chain reaction: oil first, inflation second, the Federal Reserve third, and then everything else bonds, stocks, the dollar, gold, and global risk appetite.

What Trump Said About Iran and Why Markets Care

Trump’s message is simple: Iran waited too long, the agreement is supposedly ready, and Tehran must sign or face consequences. RTVE reported that Trump claimed Iran had already agreed not to have a nuclear weapon but had not signed the document. Iran, meanwhile, responded that threats against the “arteries of life” of its people show desperation and said it would stand firm against pressure.

El País added a broader context: Iran attacked U.S. bases in Jordan, Bahrain, and Kuwait after U.S. strikes near the Strait of Hormuz, while Trump warned that attacks could continue.

Markets care because the Strait of Hormuz is not just a map location. It is one of the most important energy chokepoints in the world. If investors believe shipping lanes are at risk, oil gets a war premium. If oil gets a war premium, inflation expectations rise. If inflation expectations rise, the Fed has less room to cut rates and may even have to stay hawkish.

That is the real danger. The military story becomes a market story very quickly.

Does Iran Really Want the Conflict to End?

The honest answer is complicated.

I do think Iran has incentives to end the conflict. A prolonged confrontation hurts its economy, limits energy exports, increases domestic pressure, and raises the risk of further infrastructure damage. But wanting the conflict to end is not the same as accepting Trump’s terms.

That distinction matters.

Iran may want a deal, but not a deal that looks like surrender. Trump’s public pressure campaign may be designed to force Tehran into signing quickly, but it can also make it politically harder for Iranian leaders to accept the agreement. In that sense, the more public the threat becomes, the harder diplomacy can become.

RTVE reported that Iran’s foreign minister criticized Washington for sending contradictory messages and for repeated ceasefire violations, while warning that Iran would not leave threats unanswered. That tells me Tehran is trying to keep two messages alive at the same time: it is open enough to negotiate, but unwilling to look weak.

So when I ask, “Does Iran really want the final end of the conflict?” my answer is: probably yes, but only if the final deal preserves regime dignity, security guarantees, and some form of economic relief. If the deal is framed as humiliation, escalation becomes more likely.

The First Market Shock: Oil and the Strait of Hormuz

The first asset class to react is oil.

That is exactly what happened. Reuters reported that Brent crude settled at $93.10 and U.S. crude at $90.03 after Trump’s threat and renewed U.S.-Iran clashes. Reuters also reported that U.S. crude rose 1.63% to $89.64 and Brent to $92.65 during the broader global market reaction to the conflict and inflation data.

This is not only about barrels lost today. It is about the probability of barrels being lost tomorrow.

Oil markets price expected disruption. If traders think tankers may avoid the region, insurance costs may rise, exports may slow, or Iran may retaliate against Gulf infrastructure, prices can move before the physical shortage fully appears.

In my view, this is where the macro risk starts. A $5 or $10 oil move can be absorbed. A sustained move toward $100 or higher starts to change inflation expectations, corporate margins, airline costs, trucking costs, consumer gasoline prices, and political pressure in Washington.

The market is not just asking, “Will there be war?” It is asking, “How expensive will energy become if this does not stop?”

The Fed’s Problem: This Is the Wrong Kind of Inflation

The Federal Reserve can deal with weak demand. It can deal with slowing growth. It can even cut rates if unemployment rises and inflation cools.

But an oil shock is different.

An oil shock raises headline inflation while also hurting growth. That is the worst mix for a central bank because it creates a stagflationary impulse: prices rise, consumers feel poorer, companies face higher costs, and monetary policy becomes trapped.

The Fed’s March 2026 minutes already showed that officials expected higher oil prices to lift inflation in the near term and delay the move back toward the 2% target. Investopedia reported that the Fed had kept its key rate in a 3.5% to 3.75% range as policymakers waited to see how the Iran war would affect inflation.

That is why Trump’s threat matters for rates. If oil stays high, the Fed cannot easily say, “This is temporary.” And if energy inflation leaks into transportation, food, wages, and inflation expectations, the Fed may have to stay restrictive for longer.

MarketWatch reported that traders still saw a Fed rate hike as likely this year, though the probability had eased slightly after CPI data, with odds of a December hike still above 66%.

My takeaway: if the conflict gets worse, rate cuts are basically dead. The debate becomes whether the Fed stays on hold or hikes.

Bonds: Why Treasury Yields Can Rise Even During a War Scare

Normally, geopolitical fear can push investors into U.S. Treasuries. That buying drives bond prices up and yields down.

But this situation is not normal.

When the geopolitical shock is also an inflation shock, bonds get pulled in two directions. Safe-haven demand helps Treasuries. Inflation fear hurts them. If investors believe oil will stay high and the Fed will remain hawkish, yields can rise even while the news is frightening.

That is why I would not blindly assume “war equals lower yields.” In an Iran escalation, the 10-year Treasury is not only pricing fear. It is pricing inflation persistence, Fed credibility, fiscal risk, and the possibility that global capital demands higher compensation to own long-duration bonds.

The iShares 20+ Year Treasury Bond ETF, TLT, was down slightly on June 10, reflecting pressure on long-duration Treasuries. MarketWatch also reported that oil prices and Treasury yields rose after Trump’s tough comments on Iran, as traders worried about energy costs and inflation.

That combination is important: oil up, yields up. For stocks, that is usually uncomfortable.

Stocks: The Market Is Not Pricing War, It Is Pricing Margin Pressure

Equities hate uncertainty, but what they really hate is margin pressure.

If oil rises, many companies face higher input costs. Airlines pay more for fuel. Shipping companies pay more. Retailers face higher logistics costs. Consumers spend more at the pump and less elsewhere. If yields rise at the same time, valuations come under pressure, especially in growth stocks.

Reuters reported that global stocks were mixed after U.S. inflation data and renewed U.S.-Iran tensions, with Asian shares hit harder, European stocks rebounding, and U.S. markets uneven. The SPDR S&P 500 ETF, SPY, traded lower on June 10, while QQQ, the Nasdaq-100 ETF, was also down, showing pressure on broad U.S. equity risk.

This is where I think investors need to separate sectors.

Energy companies may benefit from higher oil prices. Defense stocks may attract flows if military spending expectations rise. But airlines, cruise lines, transport, chemicals, consumer discretionary, and high-duration tech can suffer if oil and yields rise together.

The stock market is not simply asking whether the U.S. will attack Iran. It is asking whether this conflict reduces earnings, raises discount rates, and weakens the consumer.

Gold: The Safe Haven That Can Still Get Hurt

Gold should be the easy trade in a geopolitical crisis. But this environment makes it harder.

Gold likes fear. It likes distrust. It likes geopolitical instability. But gold does not like rising real yields. If Treasury yields rise because the Fed is expected to stay tight, gold can struggle even when the news looks bullish.

That is exactly the tension here. The SPDR Gold Shares ETF, GLD, was down sharply on June 10 despite the Iran escalation. Reuters also reported that precious metals declined as markets processed inflation data, oil moves, and geopolitical tensions.

So my view is this: gold becomes more attractive if the conflict escalates into a broader confidence shock, if the dollar weakens, or if investors start doubting the Fed’s ability to control inflation. But if the immediate reaction is higher oil, higher yields, and a stronger dollar, gold can get hit first.

That is why gold is not just a war trade. It is a real-yield trade, a dollar trade, and a trust trade.

Three Scenarios From Here

Scenario 1: A Deal Is Signed

This is the cleanest outcome for markets.

If Iran signs a deal and the Strait of Hormuz risk premium fades, oil could fall quickly. Inflation expectations would cool. The Fed would have more room to stay patient or eventually discuss cuts again. Stocks would likely rally, especially transportation, airlines, consumer discretionary, and growth names.

Gold could weaken in this scenario if fear fades and yields remain firm.

Scenario 2: Controlled Escalation

This is probably the most realistic near-term scenario.

The U.S. and Iran exchange limited attacks, both sides keep talking, and neither wants a full regional war. Oil stays elevated but does not explode. The Fed stays cautious. Treasury yields remain volatile. Stocks chop sideways with sector rotation: energy and defense outperform, consumer and long-duration growth struggle.

This is the “bad but manageable” scenario.

Scenario 3: Full Regional Escalation

This is the dangerous one.

If Iran expands attacks, Gulf bases are hit again, shipping is seriously disrupted, or Israel’s parallel conflicts widen, the market reaction changes completely. Oil could spike hard. Inflation expectations could jump. The Fed could be forced into a more hawkish stance even as growth weakens.

That would be toxic for risk assets.

In that scenario, I would expect equities to sell off, credit spreads to widen, volatility to surge, oil to outperform, and gold to eventually catch a bid once the market shifts from “inflation shock” to “systemic fear.”

My Bottom Line

I do not see Trump’s threat to Iran as a one-day headline. I see it as a macro stress test.

The first question is military: will the U.S. attack again?

The second question is diplomatic: does Iran actually sign?

But the third question is the one markets care about most: does this become a lasting oil shock?

If the answer is yes, then everything changes. The Fed becomes more hawkish. Bonds lose their clean safe-haven role. Stocks face margin pressure. Gold becomes complicated. And the U.S. consumer gets squeezed through gasoline, transport, food, and confidence.

Iran may want the end of the conflict, but not at any price. Trump may want a deal, but his public threats raise the cost of compromise. That is why this moment is so fragile.

For me, the key is simple: watch oil first, then Treasury yields, then the Fed. If those three move in the wrong direction together, this stops being a geopolitical story and becomes a market regime shift.

FAQs

Why did Trump threaten Iran?

Trump threatened Iran because he claims Tehran has taken too long to sign a peace agreement that, according to him, is already negotiated. He has also linked the threat to renewed U.S.-Iran military exchanges near the Strait of Hormuz.

Does Iran want the conflict to end?

Iran likely has economic and strategic reasons to end the conflict, but it does not want to appear to surrender under U.S. pressure. That makes diplomacy possible but politically difficult.

What happens if the Iran conflict gets worse?

The first impact would likely be higher oil prices. The second would be higher inflation expectations. The third would be a more hawkish Fed, which could pressure bonds, stocks, and consumer-sensitive sectors.

Could the Fed raise rates because of the Iran conflict?

Yes, if the oil shock becomes persistent and spreads into broader inflation. MarketWatch reported that traders still saw a 2026 Fed hike as likely, with December hike odds above 66% after the latest CPI data.

Why can Treasury yields rise during a war scare?

Because this is not only a fear shock; it is also an inflation shock. If oil rises enough to keep the Fed hawkish, yields can rise even while investors are nervous.

Is gold a good hedge here?

Gold can help in a deeper geopolitical or confidence crisis, but it can fall if Treasury yields and the dollar rise. That is why gold’s reaction during this Iran crisis is more complicated than a simple safe-haven narrative.