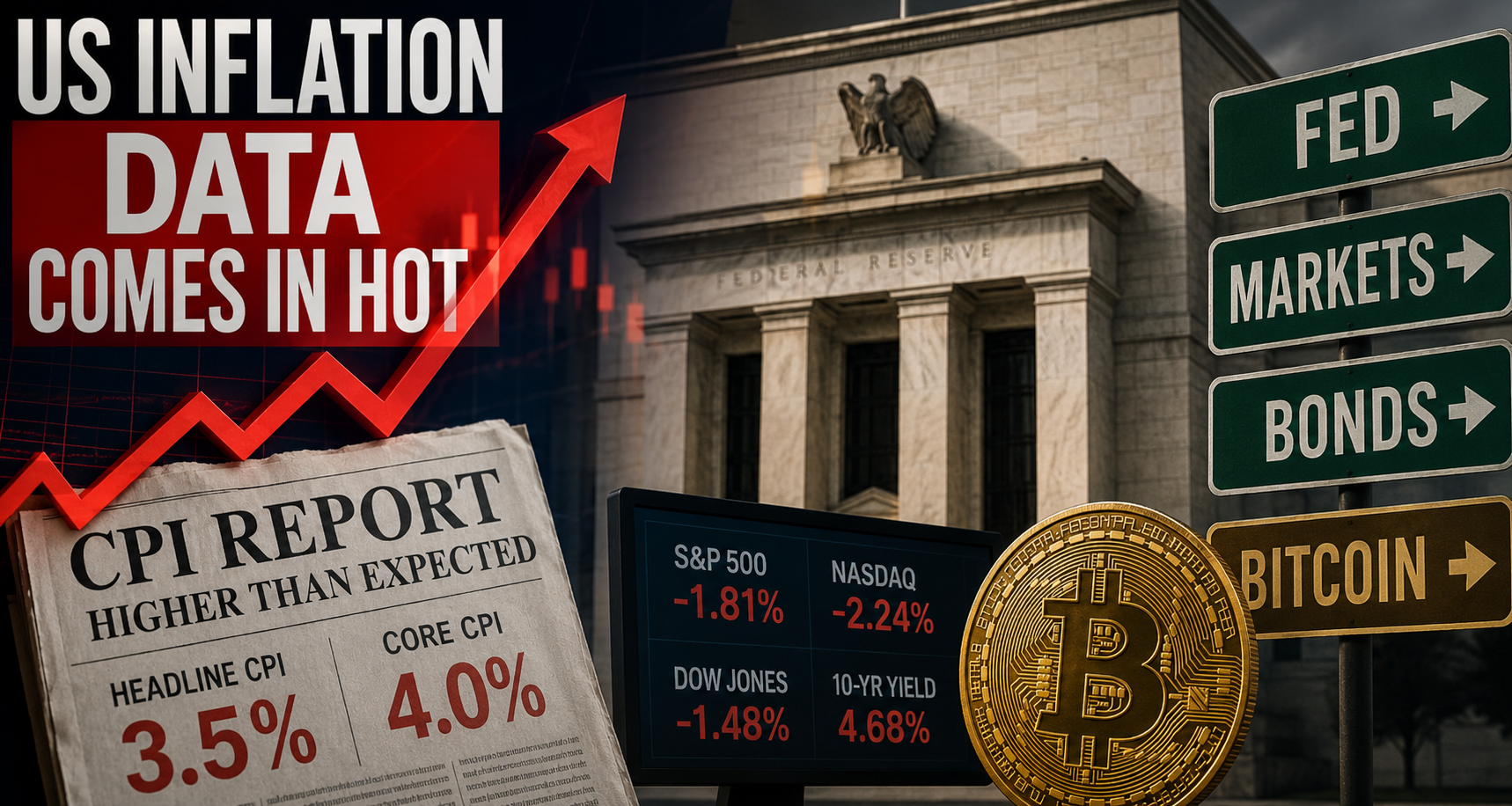

The latest US inflation data is not the kind of CPI report investors wanted to see.

Headline inflation jumped back to 4.2% year over year in May, with the Consumer Price Index rising 0.5% month over month. That is a bad number, not because every single part of the inflation basket is exploding, but because it hits at exactly the wrong moment: markets were hoping for rate-cut relief, and this report makes that story much harder to defend. Core CPI, which excludes food and energy, rose 2.9% year over year, which is less dramatic than the headline number but still clearly above the Federal Reserve’s comfort zone. The Fed’s longer-run inflation goal is 2%, measured by PCE inflation, not CPI, but a 4.2% CPI print still creates an uncomfortable credibility problem.

When I look at this CPI report, I do not see just another macro number. I see a warning sign for every asset that has been pricing in easier financial conditions: stocks, long-duration growth names, bonds, crypto and even parts of the real estate market.

The key issue is simple: inflation is hot again, and the Fed cannot casually ignore that.

The Latest US Inflation Data: Why the CPI Report Was Bad

The headline number is the first problem. A move to 4.2% annual inflation is psychologically important because it takes the market away from the “inflation is slowly drifting back to target” narrative and pushes it toward a more uncomfortable question: what if inflation gets stuck above 3% or 4% again?

That matters because markets do not only react to the data itself. They react to how the data changes the expected path of interest rates.

Before a hot CPI report, investors can tell themselves a comfortable story: inflation is cooling, the Fed will eventually cut, bond yields will fall, liquidity will improve, and risk assets can continue higher. But after a bad inflation print, that story becomes fragile. Suddenly, rate cuts look less certain. The Fed sounds less flexible. Bond yields become more dangerous. Equity multiples become harder to justify. Bitcoin and crypto lose part of the liquidity tailwind they depend on.

Headline CPI jumped back above 4%

The headline CPI number is ugly because it shows inflation accelerating again. In May, CPI rose 0.5% month over month and 4.2% year over year, according to the Bureau of Labor Statistics. Energy was the dominant factor behind the monthly increase, which makes the report different from a broad, demand-driven inflation shock. But it is still a problem because energy affects everything: gasoline, freight, airline costs, business margins, consumer confidence and inflation expectations.

This is why I would not dismiss the report as “just energy.” That phrase sounds reassuring, but it can be dangerous. Energy shocks often start as a narrow problem and then spread into other parts of the economy if they last long enough.

Core inflation was less dramatic, but still too high

Core CPI was not as scary as the headline number. That is the one piece of the report that gives the Fed some room to breathe. Core inflation at 2.9% year over year suggests that the underlying inflation trend is not yet spiraling out of control.

But “less bad” is not the same thing as “good.”

The Fed does not want inflation near 3%. It wants inflation moving convincingly toward 2%. And the problem with a hot headline CPI report is that it can eventually contaminate core inflation through second-round effects. If companies face higher energy and transportation costs, they may raise prices. If workers feel their purchasing power falling, they may demand higher wages. If consumers start expecting higher inflation, that expectation itself can become part of the inflation problem.

That is the real risk.

Why this matters more than a normal monthly CPI print

This CPI report matters because it challenges the market’s assumptions.

A single bad inflation report does not automatically mean the Fed will hike rates. But it does make rate cuts harder to justify. It also forces investors to reprice the probability of a longer period of restrictive monetary policy.

In plain English: money may stay expensive for longer.

And when money stays expensive, everything changes.

Why Has US Inflation Risen So Much?

The main reason inflation jumped is energy. The BLS reported that the energy index rose 23.5% over the past 12 months, while gasoline surged 40.5% year over year. Energy also rose 3.9% in May, contributing heavily to the monthly CPI increase.

That is the first answer.

But it is not the whole answer.

Inflation does not move through the economy in a straight line. It moves through channels. Energy is the initial shock, but the second step is what matters for investors.

Energy prices are the main driver

Energy is one of the most powerful inflation drivers because it touches almost every part of the economy.

When oil and gasoline prices rise, households feel it immediately. Filling up the car becomes more expensive. Heating and cooling costs can rise. Travel becomes more costly. Delivery costs increase. Businesses that rely on transportation see margins squeezed.

This creates two possible outcomes.

In the first outcome, companies absorb the higher costs and profit margins fall. That is bad for equities.

In the second outcome, companies pass the costs on to consumers and prices rise more broadly. That is bad for inflation and therefore bad for the Fed.

Neither scenario is great.

Gasoline, transportation and logistics are the channels to watch

Gasoline matters because it is visible. People may not check the CPI basket every month, but they notice the price at the pump.

That visibility is important. Inflation expectations are partly psychological. If consumers keep seeing gasoline prices rise, they may start behaving as if inflation will stay high. They may demand higher wages. They may pull forward purchases. They may become more sensitive to price increases.

Transportation is another key channel. Higher fuel costs can raise shipping costs, airline costs and logistics expenses. If those increases persist, they can feed into the prices of goods and services that are not directly classified as energy.

That is why I would watch transportation-heavy sectors closely. Retailers, airlines, delivery companies, industrial firms and consumer goods businesses can all feel the pressure.

The second-round risk: when energy inflation becomes broader inflation

The Fed can live with temporary volatility. It cannot live with inflation psychology becoming unanchored.

This is the distinction that matters most.

A temporary energy shock is painful but manageable. A broader inflation wave is much more dangerous. If energy prices stay high long enough, the risk is that inflation spreads into services, wages, rents, insurance, transportation and business contracts.

That is when the Fed starts to worry.

In my view, the market should not obsess only over the next CPI print. It should watch whether the energy shock starts appearing in core categories. If core CPI keeps moving higher, the Fed’s patience will run out quickly.

How Will the Fed Take This Inflation Report?

The Fed will not like this report.

That does not mean it will panic. But it does mean the Fed has less room to sound dovish.

The Federal Reserve’s official long-run inflation objective is 2%, and a CPI print above 4% makes it much harder for policymakers to argue that inflation is comfortably under control.

The Fed can probably tolerate a temporary energy shock. What it cannot tolerate is a market that starts believing 4% inflation is normal again.

The Fed can ignore noise, but not a credibility problem

Central banks care deeply about credibility. If people believe the Fed will bring inflation back to target, inflation expectations tend to stay anchored. If people stop believing that, inflation becomes much harder to control.

That is why this CPI report is uncomfortable.

It is not just about May. It is about the message it sends. If inflation remains above target for too long, investors, companies and households may start to adjust behavior around higher inflation.

That is exactly what the Fed wants to avoid.

Rate cuts now look harder to justify

This is probably the most immediate market implication: rate cuts become harder.

A hot CPI report gives hawkish Fed officials more ammunition. It allows them to say, “We need more evidence before easing policy.” Even if the Fed does not raise rates, it can keep rates higher for longer.

For markets, that matters a lot.

Lower expected rate cuts usually mean:

| Asset / Market | Typical Impact of Hot CPI |

|---|---|

| US dollar | Potentially stronger |

| Treasury yields | Higher or more volatile |

| Growth stocks | Pressure on valuations |

| S&P 500 | Risk of multiple compression |

| Nasdaq | More exposed due to duration |

| Bitcoin | Pressure if real yields rise |

| Gold | Mixed: inflation hedge vs stronger dollar |

Could the Fed raise rates again?

A rate hike is not my base case from one CPI report alone. The Fed will likely want to see whether this is a temporary energy-driven spike or the start of something broader.

But the probability of a hike increases if three things happen:

- Energy prices stay high.

- Core inflation starts accelerating.

- Inflation expectations move higher.

That combination would be dangerous.

The Fed does not need to hike immediately to hurt markets. Sometimes the damage comes simply from removing the hope of cuts.

What This Inflation Data Means for the Stock Market

Hot inflation is usually bad for stocks because it attacks the market from several directions at once.

First, it can raise bond yields. Second, it can reduce the probability of Fed cuts. Third, it can pressure corporate margins. Fourth, it can reduce consumer purchasing power. Fifth, it can lower the valuation investors are willing to pay for future earnings.

That is a lot for the market to digest.

Higher inflation pressures valuations

Equity valuation is deeply connected to interest rates.

When inflation is low and rates are falling, investors are often willing to pay higher multiples for future earnings. That is especially true for growth stocks, technology stocks and companies whose profits are expected far into the future.

But when inflation rises and rates stay high, those future profits become less valuable in today’s terms.

That is why a hot CPI report can hit the Nasdaq harder than more defensive sectors. Long-duration assets suffer when discount rates rise.

Growth stocks and the Nasdaq are more exposed

The Nasdaq is full of companies with high expectations. Many of them are excellent businesses, but excellent businesses can still be expensive.

When inflation rises, investors start asking tougher questions:

- Are earnings estimates too optimistic?

- Will margins survive higher input costs?

- Will consumers keep spending?

- Will the Fed keep liquidity tight?

- Are valuations too high if bond yields rise?

That does not mean growth stocks must crash. But it does mean the margin for error becomes smaller.

Why “bad news is bad news” again

During some market cycles, bad economic news can be good for stocks because it increases the odds of Fed cuts.

But hot inflation is different.

Hot inflation is bad news because it limits the Fed’s ability to help. If growth slows while inflation rises, the Fed faces a much harder trade-off. It cannot easily cut rates to support the economy if inflation is still too high.

That is the uncomfortable part of this CPI report.

Markets can handle weak growth if the Fed can respond. They can handle inflation if growth is strong enough. What they hate is sticky inflation with less policy flexibility.

What Happens to Bonds When Inflation Comes In Hot?

Bonds are at the center of this story.

When inflation comes in hotter than expected, bond investors usually demand higher yields. They want compensation for inflation risk, and they also price in the possibility that the Fed will keep rates higher for longer.

That is why hot CPI reports often create pressure in the Treasury market.

Treasury yields may stay higher for longer

If inflation is running at 4.2%, it becomes harder for yields to fall sustainably unless investors believe the spike is temporary.

The market will ask one basic question: is this inflation shock going to fade, or is it going to stick?

If the answer is “fade,” bonds can stabilize.

If the answer is “stick,” yields can remain elevated.

The 2-year yield reflects Fed expectations

The 2-year Treasury yield is especially sensitive to Fed policy expectations.

If traders believe the Fed will delay cuts or consider further hikes, the 2-year yield tends to rise. That can tighten financial conditions quickly because it affects short-term borrowing expectations across the economy.

For me, the 2-year yield is one of the cleanest ways to see whether the market believes the Fed is losing flexibility.

The 10-year yield reflects inflation, growth and risk premium

The 10-year Treasury yield is more complex. It reflects expected inflation, expected growth, Fed policy, global demand for Treasuries and term premium.

A hot CPI report can push the 10-year yield higher if investors believe inflation will remain elevated. But if the report also increases recession fears, the 10-year reaction can become more mixed.

That is why bonds can be tricky around inflation shocks. Short-term yields may rise because of the Fed, while long-term yields depend on whether investors fear persistent inflation or future economic weakness.

What This Means for Bitcoin and Crypto

Bitcoin is one of the most interesting assets in this inflation story because the long-term narrative and the short-term trading behavior can point in different directions.

Long term, Bitcoin is often viewed as a hedge against fiat debasement and excessive monetary expansion. But short term, BTC frequently behaves like a high-beta liquidity asset.

That distinction matters.

Bitcoin’s long-term inflation hedge story vs short-term liquidity reality

In theory, high inflation should help Bitcoin’s narrative. If fiat currencies lose purchasing power, a scarce digital asset with a fixed supply becomes more attractive.

But markets do not always trade on theory.

In the short run, Bitcoin often reacts to liquidity, real yields and risk appetite. If hot inflation pushes Treasury yields higher and makes the Fed more hawkish, BTC can come under pressure even while the long-term inflation-hedge story remains intact.

That is why I would not say, “Inflation is high, so Bitcoin must go up.” That is too simplistic.

A better way to frame it is:

Bitcoin likes the idea of monetary debasement, but it does not like a Fed that is forced to keep liquidity tight.

Why rising real yields can hurt BTC

Real yields are crucial for Bitcoin.

When real yields rise, investors can earn more attractive returns in safer assets. That makes speculative assets less appealing. Bitcoin, tech stocks and other high-duration assets can all suffer in that environment.

This is especially true if the dollar strengthens at the same time. A stronger dollar often tightens global liquidity conditions, and Bitcoin tends to dislike that setup.

When Bitcoin could recover despite hot inflation

Bitcoin could recover if the market starts to believe the inflation spike is temporary.

For example, BTC could stabilize or rally if:

- Energy prices cool.

- Core CPI remains contained.

- The Fed signals patience.

- Treasury yields stop rising.

- Liquidity conditions improve.

- Investors return to risk assets.

So the key for Bitcoin is not just inflation. It is the combination of inflation, Fed reaction, yields and liquidity.

That is the part many people miss.

My Take: This CPI Report Is Not Just About One Bad Number

I think the biggest mistake investors can make here is treating this CPI report as a single isolated number.

The real issue is the chain reaction.

Hot CPI changes Fed expectations. Fed expectations move bond yields. Bond yields affect equity valuations. Equity valuations affect risk appetite. Risk appetite affects Bitcoin and crypto. Energy prices affect margins. Margins affect earnings. Earnings affect stock prices.

That is why one inflation report can matter so much.

The real question is whether inflation spreads beyond energy

If this is mainly an energy shock, the Fed can stay cautious without panicking. It may delay cuts, maintain a hawkish tone and wait for more data.

But if energy inflation spreads into core inflation, the story changes.

That would mean the inflation problem is becoming broader. And broader inflation is harder to fix without tighter policy.

This is the line I would watch very closely:

Headline inflation can be noisy. Core inflation tells us whether the noise is becoming a trend.

Markets can handle bad data; they hate bad data with no clear Fed exit

Markets do not need perfect data. They need a path.

If investors believe inflation will cool and the Fed can cut later, they may look through a bad CPI report. But if the market starts to believe inflation is sticky and the Fed has no clean exit, risk assets become vulnerable.

That is why this report is so important.

It does not guarantee a market crash. It does not guarantee a Fed hike. It does not guarantee Bitcoin weakness forever.

But it does remove some of the easy optimism.

Scenario Table: What Comes Next After This Hot CPI Report?

| Scenario | Inflation Path | Fed Reaction | Bonds | Stocks | Bitcoin |

|---|---|---|---|---|---|

| Best case | Energy cools, core stays near 3% or lower | Fed stays on hold, cuts remain possible later | Yields stabilize | Relief rally possible | BTC benefits from improved liquidity |

| Base case | Headline stays high, core contained | Fed delays cuts, hawkish hold | Yields remain elevated | Choppy market | BTC volatile, range-bound |

| Bad case | Energy spreads into core inflation | Fed considers hikes | Yields rise further | Valuation pressure | BTC weakens as real yields rise |

| Worst case | Inflation rises while growth slows | Fed trapped | Curve volatility increases | Stagflation fears | High volatility, liquidity stress |

My base case is not panic. My base case is higher-for-longer pressure.

The Fed probably does not need to hike immediately unless future data confirms that inflation is broadening. But the market does need to stop assuming that rate cuts are easy.

Conclusion: A Bad Inflation Report, But Not Yet a Full Inflation Panic

The latest US inflation data is bad because headline CPI is back above 4%, energy prices are surging and the report makes the Fed’s job harder.

But it is not a full inflation panic yet.

The key reason is core CPI. At 2.9% year over year, core inflation is still too high, but it is not exploding at the same pace as the headline number. That gives the Fed some room to wait.

Still, the market reaction should be cautious. This report weakens the case for near-term rate cuts, supports the “higher for longer” narrative and puts pressure on bonds, growth stocks and Bitcoin.

For me, the most important takeaway is this:

The danger is not just that inflation rose. The danger is that inflation rose at a moment when markets were positioned for relief.

That makes this CPI report more than a macro headline. It makes it a serious test for the Fed, Treasury yields, equity valuations and crypto liquidity.

FAQs About the Latest US Inflation Data

Why was the latest US inflation data bad?

It was bad because headline CPI rose to 4.2% year over year, driven mainly by energy prices. That is well above the Fed’s 2% inflation objective and makes rate cuts harder to justify.

Will the Fed raise interest rates because of this CPI report?

One hot CPI report alone may not be enough to force a rate hike. But it does make the Fed more cautious. If future reports show that inflation is spreading from energy into core categories, the probability of another hike would rise.

Is high inflation bad for Bitcoin?

In the long run, high inflation can support Bitcoin’s scarcity narrative. In the short run, however, hot inflation can hurt BTC if it pushes real yields higher, strengthens the dollar and forces the Fed to keep liquidity tight.

Why do bond yields rise when inflation is high?

Bond yields often rise because investors demand more compensation for inflation risk. Hot inflation also increases the chance that the Fed keeps interest rates high, which can push short-term Treasury yields higher.

Could inflation fall again if energy prices cool?

Yes. If energy prices fall and the shock does not spread into core inflation, headline CPI could cool again. That would give the Fed more flexibility and could support bonds, stocks and Bitcoin.