Tariffs, strategic competition and debt risks are colliding at a delicate moment for global markets

The trade conflict between the United States and China is no longer simply a dispute over tariffs or trade balances.

It is gradually evolving into a broader economic and geopolitical confrontation capable of reshaping global supply chains, inflation dynamics, industrial policy, technological leadership and long-term capital flows.

What initially began years ago as a disagreement over manufacturing practices and market access is now increasingly connected to:

- Artificial intelligence.

- Semiconductor dominance.

- Strategic commodities.

- Energy security.

- Industrial autonomy.

- Financial resilience.

From my perspective, this is one of the most important structural macroeconomic transitions currently taking place in global markets. And the timing could hardly be more sensitive.

The global economy is already dealing with:

- Historically high public debt.

- Tighter financial conditions.

- Elevated bond yields.

- Slowing growth momentum.

- Geopolitical instability.

- Persistent inflation pressures.

- Growing concerns over fiscal sustainability.

That is why the current trade tensions matter far beyond imports and exports. They are emerging at a moment when the global financial system is already carrying significant structural vulnerabilities.

As explained in our previous analysis, “Global Debt Crisis Escalates and Raises Financial Risk”, rising debt levels combined with higher interest rates are already reducing fiscal flexibility across multiple economies.

A prolonged trade war could amplify those risks considerably.

The reason is simple: fragmentation tends to increase costs, reduce efficiency and weaken global growth at precisely the moment when many governments can least afford additional economic stress.

The Trade War Is No Longer About Trade Alone

The modern US-China confrontation increasingly revolves around:

- Semiconductors.

- AI infrastructure.

- Rare earths.

- Industrial supply chains.

- Advanced manufacturing.

- Technological sovereignty.

- Strategic minerals.

- Energy security.

Tariffs are now only one visible layer of a much broader strategic rivalry.

China continues to dominate large parts of the global supply chain for:

- Rare earth refining.

- Battery materials.

- Industrial processing.

- Solar components.

- Strategic manufacturing.

Meanwhile, the United States is attempting to reduce dependency on Chinese production while expanding domestic industrial capacity through subsidies, export controls and industrial policy.

This creates a powerful feedback loop:

- Tariffs increase costs.

- Supply chains fragment.

- Companies relocate production.

- Governments intervene more aggressively.

- Geopolitical risk rises.

- Markets become more volatile.

And unlike previous decades, this is happening in an environment where globalization itself is slowing down. For years, companies optimized their operations around efficiency and low-cost international production. Today, many are being forced to optimize around resilience and strategic security instead.

That transition is far more expensive. It also introduces uncertainty into corporate investment decisions, long-term earnings expectations and global capital allocation.

The New Economic Fragmentation Cycle

Trade wars increasingly affect inflation, investment flows and financial stability simultaneously.

Why Markets Are Paying Attention Again

Financial markets initially viewed the trade war mainly as a temporary political or negotiation-driven risk. That perception is gradually changing. The reason is that investors increasingly understand this may not be a short-term cycle, but rather a structural shift in the architecture of the global economy.

The world economy spent decades optimizing around:

- Low-cost manufacturing.

- Globalization.

- Efficient supply chains.

- Just-in-time production.

- Cross-border capital flows.

Now governments are prioritizing:

- Resilience.

- National security.

- Strategic autonomy.

- Domestic manufacturing.

- Supply-chain control.

This transition is fundamentally inflationary because it sacrifices part of the efficiency created during the globalization era.

Producing goods closer to home often means:

- Higher labor costs.

- Higher infrastructure spending.

- Duplication of supply chains.

- Lower economies of scale.

- Greater regulatory costs.

That does not necessarily mean runaway inflation. But it does suggest that the ultra-low inflation environment experienced during the 2010s may not fully return.

And that changes the macroeconomic landscape significantly.

Higher structural inflation could force central banks to maintain restrictive monetary policies for longer periods, especially if trade fragmentation continues to pressure supply chains.

Globalization Era vs Fragmentation Era

| Globalization Model | Fragmentation Model |

|---|---|

| Lowest-cost production | Strategic production |

| Global supply chains | Regionalized supply chains |

| Efficiency optimization | Security and resilience |

| Cheap imports | Higher production costs |

| Trade integration | Industrial protectionism |

| Stable disinflation | Structural inflation pressure |

The global economy is gradually moving from efficiency-driven globalization toward resilience-driven regionalization.

Why This Matters for Inflation

One of the biggest macroeconomic consequences of the trade war is inflation persistence.

For decades, globalization acted as a powerful disinflationary force by:

- Reducing manufacturing costs.

- Increasing global competition.

- Expanding labor supply.

- Lowering import prices.

- Improving supply-chain efficiency.

Now part of that mechanism is reversing.

If companies relocate production away from China:

- Costs rise.

- Logistics become less efficient.

- Industrial duplication increases.

- Labor becomes more expensive.

- Inventory management becomes more complex.

This process may create structural upward pressure on prices across several sectors of the economy. And importantly, this inflationary effect could persist even if energy prices temporarily stabilize.

That is why central banks are increasingly concerned not only about short-term inflation spikes, but about longer-term structural inflation dynamics tied to supply chains, industrial policy and geopolitical fragmentation.

This matters enormously for:

- Bond markets.

- Equity valuations.

- Debt sustainability.

- Real wages.

- Corporate profitability.

- Monetary policy expectations.

From a macro perspective, the world economy may be transitioning from an era dominated by efficiency and disinflation toward one characterized by resilience, redundancy and structurally higher costs.

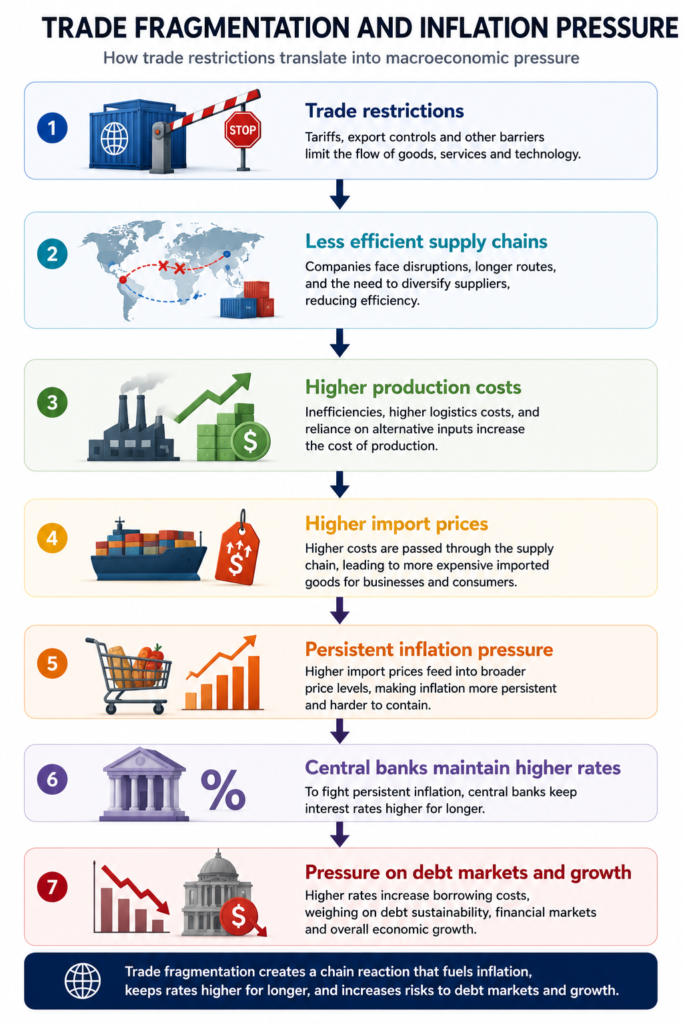

Trade Fragmentation and Inflation Pressure

Trade fragmentation can reinforce inflationary pressures and complicate monetary policy.

The Debt Problem Makes Everything More Fragile.

This is where the situation becomes significantly more dangerous. The global economy is entering this trade confrontation with historically elevated debt levels.

Governments accumulated enormous debt burdens after:

- The 2008 financial crisis.

- The pandemic.

- Fiscal stimulus programs.

- Energy shocks.

- Military spending increases.

- Industrial subsidies.

Now interest rates are substantially higher than they were during most of the previous decade.

That creates a major vulnerability. As discussed in our previous article on the sovereign debt crisis, higher bond yields increase refinancing costs and reduce fiscal flexibility for governments already carrying large debt burdens.

This is critical because fragmented global trade could force central banks to maintain tighter monetary conditions for longer.

That combination:

- Slower growth.

- Persistent inflation.

- Elevated debt.

- Higher refinancing costs.

Creates a much more fragile macroeconomic environment. From my perspective, this is one of the most underestimated risks currently facing markets.

Many investors still analyze:

- Debt.

- Inflation.

- Trade wars.

- Geopolitics.

As separate themes.

But increasingly they are interconnected.

Trade fragmentation can reinforce inflation. Inflation can keep rates elevated. Higher rates can pressure sovereign debt markets. Debt stress can weaken growth and financial stability.

The macro cycle becomes far more unstable when these forces start feeding into each other simultaneously.

Why Trade Wars Increase Financial Fragility

| Trade War Effect | Macroeconomic Consequence |

|---|---|

| Higher tariffs | More inflation pressure |

| Supply-chain disruptions | Lower efficiency |

| Slower trade growth | Weaker GDP growth |

| Higher rates for longer | Debt refinancing stress |

| Reduced global cooperation | More market volatility |

| Industrial subsidies | Rising fiscal deficits |

Trade wars increasingly interact with debt dynamics and monetary policy risks.

China, Rare Earths and Strategic Commodities

One of the most underestimated aspects of this conflict is strategic commodities.

China controls large portions of the global processing capacity for:

- Rare earths.

- Graphite.

- Gallium.

- Battery materials.

- Industrial refining.

This gives Beijing significant strategic leverage.

At the same time, the United States and Europe are trying to:

- Diversify suppliers.

- Expand domestic mining.

- Subsidize critical industries.

- Reduce dependency on Chinese processing.

This is not just a trade issue anymore. It is a supply-chain sovereignty issue. And artificial intelligence is making this even more important.

AI infrastructure requires:

- Semiconductors.

- Data centers.

- Electricity grids.

- Copper.

- Rare earths.

- Advanced cooling systems.

This means the AI race and the trade war are increasingly connected. The countries capable of controlling critical inputs for AI infrastructure may gain major economic and geopolitical advantages over time.

That is why the conflict increasingly extends beyond traditional manufacturing and into the strategic control of technological infrastructure itself.

The New Strategic Competition

Recommended infographic

The trade war is increasingly connected to AI infrastructure and strategic commodity control.

How Financial Markets Could React

Markets generally dislike uncertainty. And trade fragmentation creates uncertainty in:

- Corporate margins.

- Supply chains.

- Inflation expectations.

- Investment decisions.

- Global growth projections.

But other sectors could face pressure:

- Exporters.

- Global logistics firms.

- Highly leveraged companies.

- Multinational manufacturers.

- Emerging markets dependent on trade flows.

Bond markets may become especially sensitive. If trade fragmentation keeps inflation elevated while growth slows, markets could face a more difficult environment: slower growth combined with persistent inflation.

That is close to a stagflationary setup.

Historically, stagflationary environments tend to be challenging for both equities and fixed income simultaneously because investors face weakening growth without meaningful monetary easing. That is why markets are paying closer attention to long-term inflation expectations and sovereign debt dynamics.

Why This Could Reshape Global Capital Flows

One of the biggest long-term implications is the reorganization of capital allocation.

For years, capital flowed toward:

- Efficiency.

- Globalization.

- Outsourcing.

- Low-cost production hubs.

The next decade may prioritize:

- Resilience.

- Domestic infrastructure.

- Energy security.

- Strategic autonomy.

- Industrial capacity.

- AI infrastructure.

That changes investment incentives globally.

Countries capable of:

- Securing energy.

- Controlling strategic minerals.

- Attracting industrial investment.

- Leading AI infrastructure.

- Maintaining fiscal stability.

May outperform economically over time.

This could also accelerate the divergence between economies with strong industrial capacity and those heavily dependent on external supply chains.

Practical Reading for Investors

The key mistake investors can make is treating the trade war as a temporary political event. This is increasingly a structural macro transition.

The world economy is moving toward:

- More geopolitical competition.

- Less globalization.

- more industrial policy.

- Greater strategic rivalry.

- Higher infrastructure spending.

- More supply-chain redundancy.

Investors increasingly need to analyze:

- Debt sustainability.

- Industrial policy.

- Geopolitical alignment.

- Strategic resources.

- Energy infrastructure.

- AI supply chains.

Rather than relying only on traditional economic indicators.

Conclusion: The Trade War Is Becoming a Macro Risk Multiplier

The US-China trade conflict is evolving into one of the defining macroeconomic themes of this decade. It is no longer simply about tariffs.

It is about:

- Technological leadership.

- Industrial sovereignty.

- AI infrastructure.

- Strategic commodities.

- Debt sustainability.

- Geopolitical influence.

And perhaps most importantly, it is happening at a moment when the global financial system is already fragile. High debt levels, rising yields and slower growth have reduced the margin for policy mistakes.

That is why the combination of: trade fragmentation + structural inflation + sovereign debt pressure.

From my perspective, the most important shift is psychological. For decades, markets assumed globalization would continue expanding almost indefinitely. Now investors are beginning to understand that the world economy may be entering a more fragmented, strategic and politically driven phase.

That transition will likely reshape:

- Inflation dynamics.

- Capital allocation.

- Industrial policy.

- Monetary policy.

- Financial markets.

- Geopolitical alliances.

And the consequences may extend far beyond trade itself.

FAQs

Why is the US-China trade war important for markets?

Because it affects inflation, supply chains, industrial production, corporate margins, debt markets and long-term global growth expectations.

Could trade wars increase inflation?

Yes. Tariffs and fragmented supply chains often increase production and import costs, which can create persistent inflationary pressure. How does the trade war affect central banks?

Trade fragmentation can complicate monetary policy by slowing growth while simultaneously keeping inflation elevated.

Why are strategic commodities becoming more important?

Because AI infrastructure, semiconductors, defense systems and energy transition technologies all depend on critical minerals and industrial supply chains. How does this relate to the global debt problem?

Higher inflation and higher interest rates increase borrowing costs for governments with already elevated debt levels, increasing financial fragility.

Could the trade war accelerate deglobalization?

Yes. Many governments are increasingly prioritizing industrial resilience, supply-chain security and domestic manufacturing over maximum efficiency.

Which sectors could benefit from this environment?

Defense, industrial infrastructure, AI infrastructure, strategic commodities, domestic manufacturing and power-grid investment may benefit structurally.

What is the biggest long-term risk?

A prolonged combination of:

- Trade fragmentation.

- Structural inflation.

- Slower growth.

- Rising debt costs.

Could create a more volatile and financially unstable macroeconomic environment.