Public Debt Crisis Enters a Critical Phase in the Global Economy

The global public debt problem is no longer a distant structural concern quietly hidden beneath years of easy monetary policy and massive liquidity injections.

It is becoming one of the defining macroeconomic risks of the current cycle.

For more than a decade, governments around the world operated in an environment dominated by ultra-low interest rates, aggressive central bank support and abundant liquidity. That framework allowed economies to accumulate enormous levels of debt without generating immediate financial stress. Markets largely accepted rising debt because borrowing costs remained historically cheap and central banks consistently intervened whenever instability emerged.

Today that environment looks completely different.

Interest rates remain elevated, inflation pressures have proven far more persistent than expected, and bond markets are increasingly sensitive to fiscal imbalances. Governments now face the difficult reality of refinancing massive debt burdens at much higher yields while growth momentum across several economies begins to slow.

From my perspective, this transition is one of the most important macroeconomic shifts currently unfolding beneath the surface of financial markets.

The era of ultra-cheap money is ending, and the global financial system is slowly adjusting to a far stricter and less forgiving environment.

Why the Debt Problem Is Becoming More Serious

Debt itself does not automatically create a crisis. The real danger appears when debt grows faster than the economy, borrowing costs rise sharply and investor confidence starts to weaken simultaneously.

For years, low interest rates helped hide these vulnerabilities. Governments could issue debt at extremely low costs, central banks provided liquidity whenever markets became unstable, and investors continued searching for yield in a world where returns were scarce.

Now the situation has reversed.

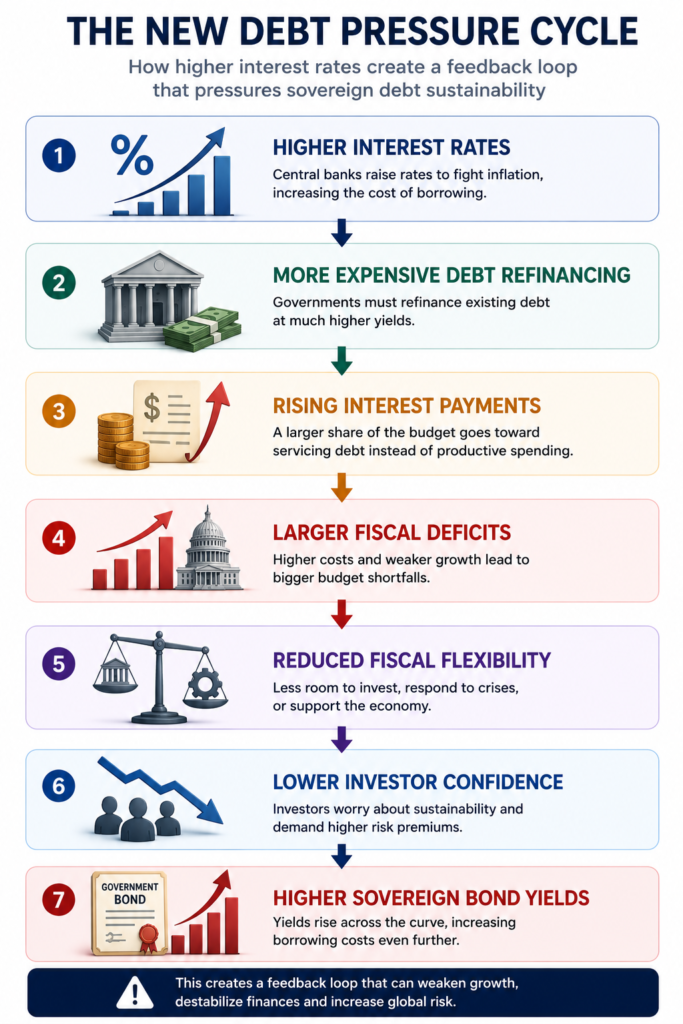

As bonds mature, governments must refinance large portions of existing debt at significantly higher yields. That gradually increases the share of public budgets allocated to interest payments and reduces fiscal flexibility at precisely the moment many economies are already facing slower growth and rising structural costs.

This is particularly important because debt sustainability depends heavily on confidence.

Markets generally tolerate high debt levels for long periods of time until they begin to question whether the underlying equilibrium remains stable. Once that perception changes, sovereign bond markets can react very quickly.

That shift now appears to be starting.

The New Debt Pressure Cycle

Higher rates are creating a feedback loop that increasingly pressures sovereign debt sustainability.

Bond Markets Are Beginning to Reprice Risk

One of the clearest warning signals is coming directly from sovereign bond markets.

Over recent months, yields have risen sharply across multiple advanced and emerging economies as investors reassess fiscal sustainability under a higher-for-longer interest rate environment.

This is not merely a technical market adjustment.

Bond markets are effectively recalculating the risk of lending money to governments in a world where inflation remains sticky, liquidity conditions are tighter and central banks are no longer acting as unconditional backstops for financial markets.

For years, markets largely assumed that central banks would rapidly lower rates whenever economic stress appeared. That assumption is now weakening significantly.

The Federal Reserve and the European Central Bank remain constrained by inflation concerns, which limits their ability to quickly return to the extremely accommodative monetary policies seen after the 2008 crisis or during the pandemic era.

That changes everything for debt markets.

When investors begin to believe rates may remain structurally higher for longer, debt levels that once appeared manageable suddenly look much more fragile.

Low-Rate Era vs High-Rate Era

| Previous Environment | Current Environment |

|---|---|

| Near-zero rates | Higher-for-longer rates |

| Cheap refinancing | Expensive refinancing |

| Strong central bank support | Restrictive monetary policy |

| Abundant liquidity | Tight financial conditions |

| Debt appeared manageable | Debt sustainability questioned |

| Low bond volatility | Rising sovereign volatility |

The transition from ultra-loose monetary policy to restrictive conditions is exposing fiscal vulnerabilities globally.

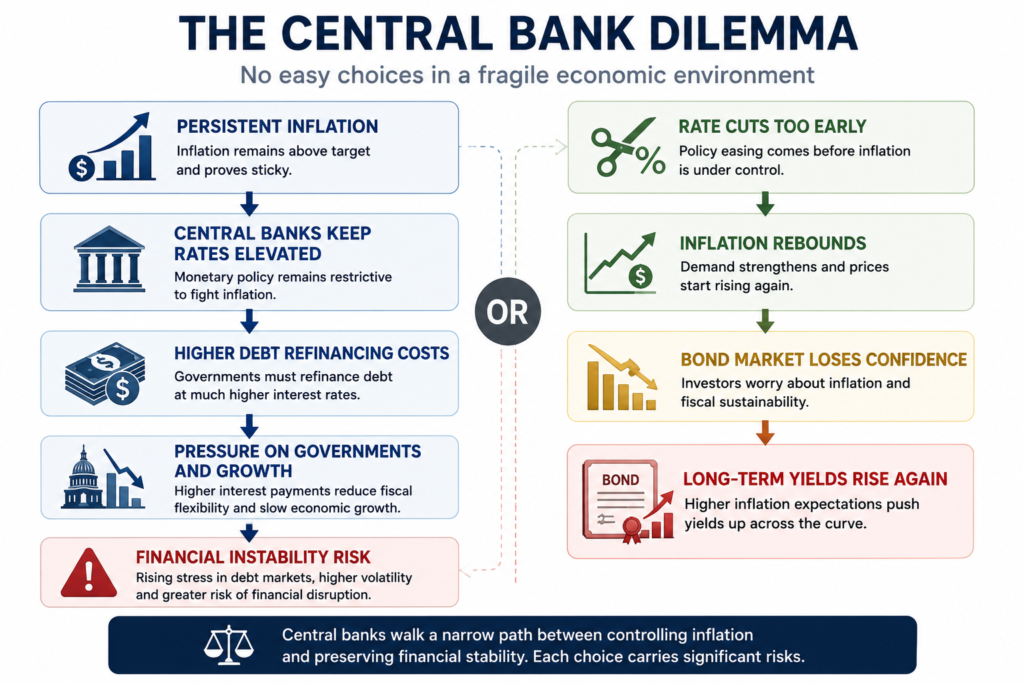

Central Banks Are Caught in an Increasingly Difficult Position

The policy dilemma facing central banks is becoming more complicated with every passing month.

On one side, inflation remains above target in several major economies. On the other, restrictive monetary policy is increasing pressure on governments, corporations, banks and consumers.

This creates a very fragile balancing act.

If central banks maintain high interest rates for too long, refinancing stress intensifies, economic growth slows and financial instability risks increase. But if they cut rates too early, inflation could reaccelerate and markets may lose confidence in their ability to restore price stability.

That is why markets have become extremely sensitive to every inflation report, labor market release and central bank statement.

Investors increasingly understand that monetary policy is no longer operating inside a normal economic cycle. It is operating inside a highly leveraged global financial system where even small changes in rates can have disproportionately large consequences.

From my perspective, this is one of the reasons volatility across bond markets is likely to remain elevated over the coming years.

The Central Bank Dilemma

Central banks are increasingly caught between inflation control and financial stability.

Financial Stress Is Gradually Reaching the Real Economy

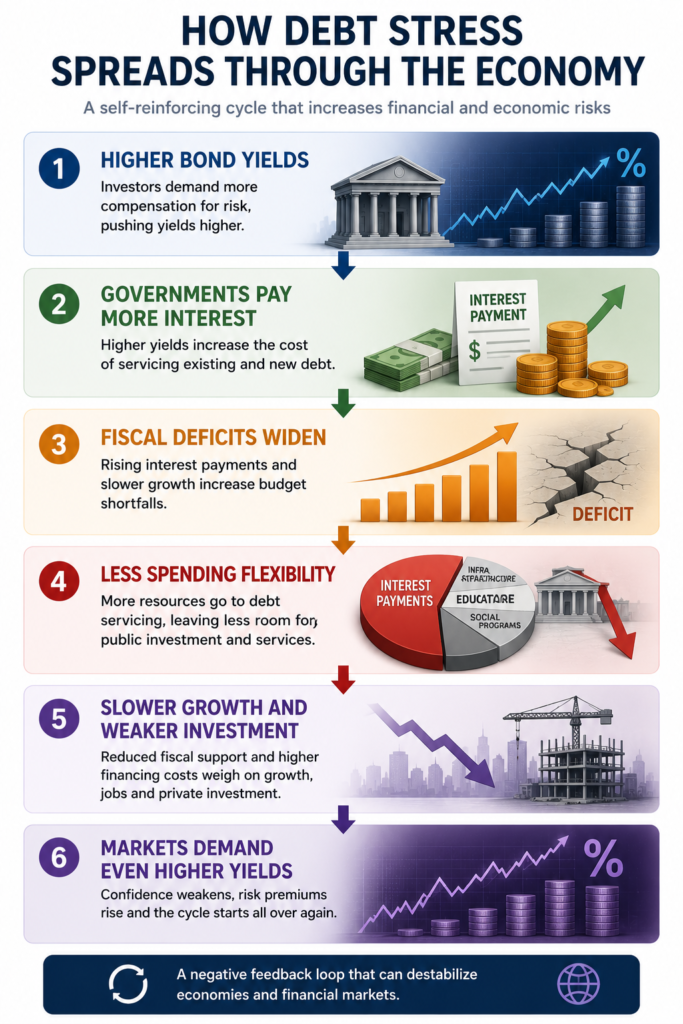

What initially begins in financial markets eventually spreads into the real economy.

That transmission mechanism is becoming increasingly visible.

Higher borrowing costs are already affecting corporate investment decisions, infrastructure projects, housing markets and consumer financing conditions. Governments facing larger interest expenses may eventually be forced to reduce spending, raise taxes or delay fiscal programs.

This is where debt crises become particularly dangerous.

They rarely emerge suddenly. More often, they develop gradually through weakening growth, tighter financial conditions, declining confidence and slower investment until markets eventually realize the equilibrium is no longer stable.

From my perspective, the global economy may be entering the early stages of that process now.

The problem is that the world economy is not dealing with debt pressures alone.

It is simultaneously facing:

- Geopolitical fragmentation.

- Trade tensions.

- Energy transition costs.

- Demographic slowdown.

- AI infrastructure investment requirements.

- Persistent fiscal deficits.

All of these forces increase pressure on public finances at the same time refinancing costs are rising.

Why Growth May Become the Only Sustainable Solution

The key variable in a high-debt world is growth.

If economies can generate strong enough productivity and innovation, debt ratios become easier to stabilize because revenues rise and financial conditions improve organically.

Without sufficient growth, however, debt sustainability becomes much more difficult regardless of fiscal adjustments.

This is one reason why markets are increasingly focused on:

- Artificial intelligence.

- Automation.

- Digitalization.

- Productivity growth.

- Technological infrastructure.

Technology may become one of the few structural forces capable of partially offsetting the burden created by elevated debt levels.

Artificial intelligence, in particular, is increasingly viewed not only as a technological revolution but as a potential macroeconomic stabilizer capable of improving productivity and long-term economic output.

That does not eliminate the debt problem.

But it could help slow the deterioration if productivity gains materialize fast enough.

Countries capable of integrating these technologies more effectively may be better positioned to maintain financial stability over the next decade.

What Could Stabilize Debt Dynamics?

| Potential Stabilizer | Why It Matters |

|---|---|

| Productivity growth | Improves economic output |

| AI and automation | Enhances efficiency |

| Strong labor markets | Supports tax revenues |

| Controlled inflation | Reduces market stress |

| Fiscal discipline | Slows debt accumulation |

| Lower refinancing costs | Improves sustainability |

Growth and productivity may become essential tools for stabilizing debt-heavy economies.

Markets Are Starting to Anticipate the Next Phase

Financial markets are forward-looking by nature. They usually react before economic deterioration becomes visible in official data.

That is why sovereign bond volatility has increased, investors are demanding higher yields and markets are becoming more selective about fiscal risk.

The environment is changing from one where liquidity and central bank support dominated market behavior to one where sustainability, productivity and fiscal credibility matter far more.

That transition could reshape how sovereign risk is priced globally.

Historically, prolonged periods of elevated debt combined with higher interest rates have often produced unstable market environments because confidence becomes increasingly sensitive to economic shocks.

This does not necessarily mean a systemic crisis is imminent. But it does suggest the margin for policy mistakes is shrinking rapidly.

How Debt Stress Spreads Through the Economy

Debt stress can gradually create a self-reinforcing negative cycle.

Conclusion: The Debt Crisis Is Entering a More Fragile Stage

The public debt problem is no longer theoretical or distant. It is gradually becoming one of the central macroeconomic challenges shaping the next phase of the global economy.

For years, low interest rates allowed governments to expand debt with relatively limited consequences. Now the environment has changed fundamentally.

Higher interest rates are exposing vulnerabilities that remained hidden during the era of ultra-cheap money, and financial markets are beginning to adjust accordingly.

From my perspective, the most important shift is psychological.

Markets are beginning to question whether debt trajectories remain sustainable in a world characterized by structurally higher rates, slower growth and tighter liquidity conditions. That matters enormously because sovereign debt markets rely heavily on confidence.

If confidence weakens meaningfully, refinancing costs can rise quickly and create a much more unstable macroeconomic environment. The key question now is whether economies can generate enough productivity, innovation and long-term growth to stabilize debt dynamics before financial stress intensifies further.

The answer may shape the trajectory of:

- Bond markets.

- Equity markets.

- Monetary policy.

- Fiscal policy.

- Global growth.

- Financial stability.

FAQs

Why is public debt becoming a bigger problem now?

Because interest rates are much higher than during the previous decade, making debt refinancing significantly more expensive for governments.

Why are bond yields rising?

Investors are demanding higher compensation for lending to governments due to inflation risks, fiscal deficits and uncertainty around debt sustainability.

How do higher rates affect governments?

Higher rates increase debt servicing costs, reduce fiscal flexibility and make it harder to stabilize debt trajectories.

Why are central banks under pressure?

Because they must balance controlling inflation while also preserving financial stability in a highly leveraged economic system.

Could high debt lead to slower economic growth?

Yes. Rising interest expenses can weaken investment, reduce fiscal flexibility and slow overall economic activity.

Why does productivity growth matter for debt sustainability?

Higher productivity can improve economic growth, increase tax revenues and help stabilize debt ratios over time.

How could AI affect the debt problem?

AI and automation may improve productivity and long-term growth, helping economies manage debt burdens more effectively.

Why are markets becoming more volatile?

Because investors are increasingly reassessing sovereign risk, fiscal sustainability and the long-term consequences of higher interest rates.