When geopolitical tensions rise, most people expect the stock market to fall. That reaction makes sense on the surface. If there is war risk, energy disruption, inflation pressure, and political uncertainty, why would investors keep buying stocks?

And yet, that is exactly what can happen.

The S&P 500 can rally during geopolitical crises because the market is not simply reacting to fear. It is constantly repricing probabilities, future earnings, interest rates, liquidity, and relative opportunity. In other words, the market is not asking, “Is the world calm?” It is asking, “Are future corporate profits still intact, and is the worst-case scenario already priced in?”

That distinction is everything.

In my view, this is where a lot of investors misunderstand the stock market. They look at the headlines and assume prices should move in a straight line with the news. Bad news should mean stocks down. Good news should mean stocks up. But markets are rarely that simple. The S&P 500 often bottoms before the headlines improve, and it can climb while the news still feels uncomfortable.

That is what makes the current market so interesting. Geopolitical tension remains elevated, especially around the Middle East and energy markets, but the S&P 500 has still shown resilience. Reuters reported that even when the S&P 500 and Nasdaq pulled back on stronger inflation data and renewed Iran-related tension, both indexes remained near recent record highs.

So the question is not simply: Why is the market ignoring geopolitical risk?

The better question is: What does the market believe about the economic impact of that risk?

The S&P 500 Does Not Trade the Crisis It Trades the Expected Damage

The first thing I always remind myself is that the S&P 500 is not a real-time emotional reflection of the world. It is a forward-looking pricing machine.

That means a geopolitical crisis does not automatically create a sustained bear market. For that to happen, the crisis has to damage the things that truly drive equity prices:

- corporate earnings,

- profit margins,

- interest rates,

- inflation expectations,

- credit conditions,

- investor liquidity,

- and the valuation investors are willing to pay for future growth.

If the crisis is frightening but contained, stocks can recover quickly. If the market believes the worst-case scenario is becoming less likely, the S&P 500 can rally even while the situation remains tense.

This is why the phrase “less bad than feared” is so important.

A market rally during a geopolitical crisis is often not a celebration. It is not investors saying everything is fine. It is investors saying, “The outcome we feared most may not happen.”

That can be enough.

If traders initially price in a major oil shock, a broader regional war, a shipping crisis, and a central bank inflation problem, the market may sell off aggressively. But if the next few days or weeks show that the crisis is still serious but more contained than feared, then the risk premium starts coming out of prices.

That is when a rally can begin.

Investing.com described part of the recent move as a result of geopolitical premium unwinding and liquidity flow, with risk assets responding positively as investors reassessed the severity of the shock.

That is how markets work. They do not need perfect news to rise. They only need the future to look better than what was already priced in.

Why the S&P 500 Can Rise While the World Feels Unstable

The current setup looks contradictory. On one side, geopolitical tension is real. Energy markets are sensitive. Inflation risks have not disappeared. Reuters reported that oil rallied as Iran-related ceasefire hopes weakened, with crude prices rising sharply and geopolitical uncertainty weighing on global markets.

On the other side, the S&P 500 has remained close to record territory.

That feels strange until you break down what investors are actually buying.

They are not buying “peace.”

They are buying resilience.

The S&P 500 today is heavily influenced by large, profitable, globally dominant companies. Many of the biggest names in the index have strong balance sheets, high margins, global revenue streams, pricing power, and business models tied to long-term themes like artificial intelligence, cloud computing, digital advertising, semiconductors, and automation.

That matters because geopolitical tension does not hit every part of the market equally.

A small industrial company with high fuel costs and weak margins may be very vulnerable to energy disruption. But a mega-cap technology company with huge cash reserves and global demand may be far more insulated. Since the S&P 500 is weighted by market capitalization, the largest companies have an outsized influence on the index.

That is one reason the index can look stronger than the broader economy.

Euronews framed this as a sharp contrast between Wall Street and Main Street: equity markets pushing toward records even while the real economy faces pressure from war, energy disruption, and slower growth.

From my perspective, that contrast is not a bug in the market. It is one of its defining features.

The S&P 500 is not the economy.

It is a collection of large public companies, weighted toward the biggest winners.

And in a crisis, global capital often runs toward the strongest, deepest, most liquid market available.

That market is still the United States.

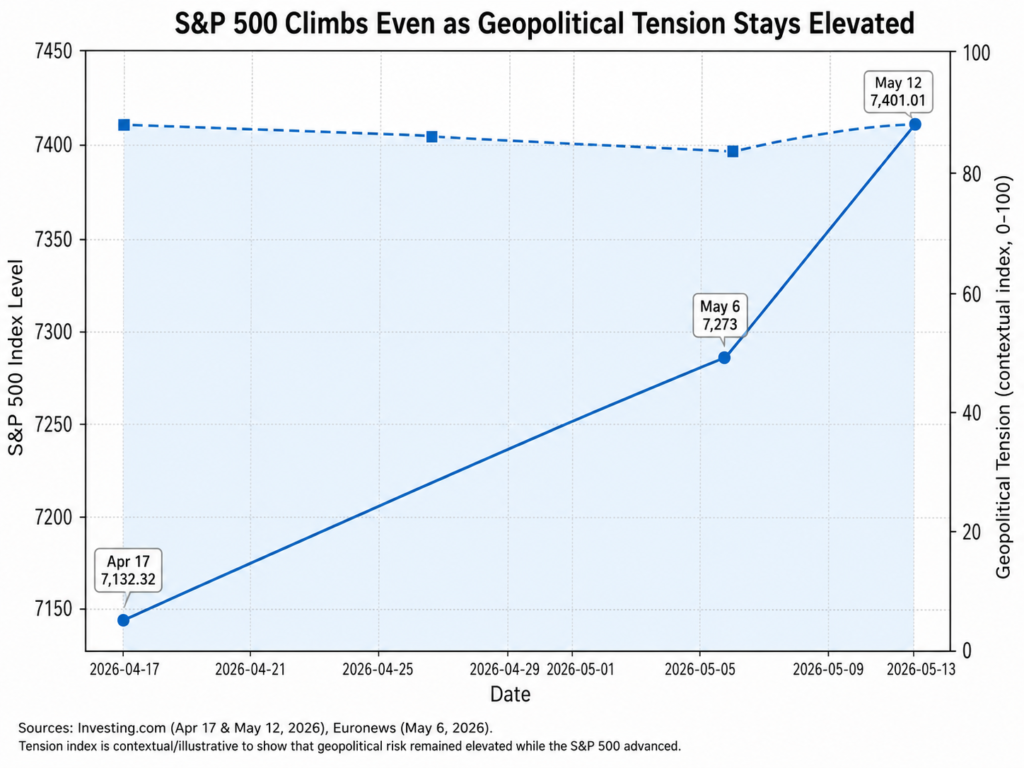

S&P 500 Climbs While Geopolitical Tension Stays Elevated

The S&P 500 continued climbing even as geopolitical tension remained elevated, showing how markets can rise when investors believe the worst-case scenario is being avoided or absorbed.

How to Interpret This Chart

This chart captures the core idea of the article: the S&P 500 can move higher even when geopolitical tension remains elevated.

The solid blue line shows the S&P 500 moving from 7,132.32 on April 17 to 7,273 on May 6, and then to 7,401.01 on May 12. The dashed line represents a contextual geopolitical tension index, showing that the rally did not happen because the world suddenly became calm. It happened while risk was still present.

That is exactly the point.

The market does not require geopolitical tension to disappear before it can rally. It only requires investors to believe that the tension is manageable, contained, or already reflected in prices.

To me, the chart shows three things clearly.

First, the market can absorb bad news if the damage to earnings expectations is limited.

Second, investors may continue buying US equities when they believe there are few better alternatives globally.

Third, geopolitical risk often causes volatility, but volatility is not the same as a lasting bear market.

This is why the S&P 500 can rise in a world that still feels unstable. The rally is not necessarily saying, “There is no risk.” It is saying, “The risk is not yet large enough to break the earnings cycle.”

The “Safe Ship in a Rough Sea” Analogy

The easiest way I think about this is with a simple analogy.

The S&P 500 during a geopolitical crisis is like the strongest ship sailing through a storm.

The storm is real. The waves are real. The danger is real. But investors are not asking whether the sea is calm. They are asking which ship is most likely to keep moving.

In many crises, the US stock market still looks like the strongest ship.

Europe may look more exposed to energy pressure. Emerging markets may look vulnerable to currency stress and capital outflows. Smaller economies may be more dependent on imported energy or global trade flows. But the US market offers depth, liquidity, reserve-currency exposure, and access to some of the most profitable companies in the world.

That is why money can flow into the S&P 500 even during global instability.

This does not mean investors are relaxed. It means they are choosing relative safety inside risk assets.

There is a difference.

Buying the S&P 500 during a crisis does not necessarily mean investors are aggressive. Sometimes it means they believe US large-cap equities are simply a better place to hide than weaker currencies, fragile regional markets, or lower-quality assets.

American Bazaar made a similar point, arguing that Wall Street’s resilience may reflect not broad economic strength, but the absence of better alternatives elsewhere, combined with AI-driven profitability and global capital flows into US assets.

I think that is one of the most important ideas behind this entire rally.

AI and Mega-Cap Strength Are Changing the Crisis Playbook

Another reason the S&P 500 can rally during geopolitical crises is that today’s market leadership is different from past cycles.

The index is no longer driven only by traditional cyclicals, banks, industrials, or energy-sensitive businesses. It is heavily shaped by technology, artificial intelligence infrastructure, semiconductors, software, cloud platforms, and mega-cap companies with enormous cash flows.

That makes the S&P 500 more resilient than many people expect.

If investors believe AI spending will continue, margins will remain strong, and the largest companies will keep growing despite geopolitical noise, then the index can keep rising even while the macro environment looks uncomfortable.

Reuters reported that AI enthusiasm helped Wall Street edge higher even as Iran-related uncertainty and oil price concerns remained in focus.

That is the modern market in one sentence.

The world can look unstable, but if AI leadership remains intact, the largest stocks can keep pulling the index higher.

From my perspective, this is one of the biggest reasons people underestimate the current rally. They look at geopolitical risk, but they do not always look at index composition. The S&P 500 is not equally exposed to every risk. It is disproportionately influenced by a relatively small group of large companies that investors believe can survive and even benefit from structural changes in the economy.

That does not make the rally risk-free.

But it does make it understandable.

Historical Context: Markets Often Recover Faster Than Fear Suggests

There is also a historical reason the S&P 500 can rally during geopolitical crises: markets have often recovered quickly from military shocks.

RBC Wealth Management reviewed 20 major post-World War II military interventions and hostilities. According to its analysis, the S&P 500 fell about 6% on average from the initial market impact to the trough, and in 19 of the 20 events, the market returned to its prior level in an average of 28 days.

That is a powerful statistic.

It does not mean geopolitical events are harmless. It does not mean every crisis is a buying opportunity. And it definitely does not mean investors should ignore war, energy shocks, or inflation pressure.

But it does show that markets often separate the emotional seriousness of an event from its long-term financial impact.

A crisis can be tragic and still not permanently impair S&P 500 earnings.

That is uncomfortable to say, but it is how markets behave.

The stock market is not designed to measure human suffering. It is designed to discount future cash flows. If the future cash-flow machine remains intact, markets can recover quickly.

The Role of Oil, Inflation, and the Federal Reserve

That said, geopolitical risk becomes much more dangerous for the S&P 500 when it turns into an inflation problem.

This is where oil matters.

If geopolitical tension causes a short-term spike in oil but prices stabilize, the market may absorb it. But if energy prices stay high long enough to lift inflation expectations, squeeze consumers, hurt corporate margins, and force the Federal Reserve to stay tighter for longer, then the rally becomes more fragile.

That is why investors pay so much attention to crude oil during Middle East tensions.

A contained geopolitical shock is one thing.

A sustained energy shock is another.

The first can create volatility.

The second can damage the macro foundation of the market.

Reuters reported that rising oil prices and stronger inflation data complicated the interest-rate outlook, adding pressure to equities even though major indexes remained close to highs.

This is the key risk.

The S&P 500 can rally through geopolitical tension as long as investors believe inflation, rates, and earnings remain manageable. But if the crisis pushes oil high enough for long enough, the story changes.

At that point, the market stops asking, “Is the crisis contained?”

It starts asking, “Will this force the Fed to tighten into a weakening economy?”

That is a much more dangerous question.

Why the Rally Can Look Irrational but Still Make Sense

I understand why this kind of rally frustrates people.

It can look like the market is detached from reality. Headlines are tense. Oil is volatile. Political risk is rising. Consumers are under pressure. And yet the S&P 500 keeps climbing.

But I do not think the market is necessarily irrational here.

I think it is focused on a different layer of reality.

The average person experiences geopolitical crises through news, uncertainty, prices at the pump, and anxiety about what could happen next. The market experiences the same crisis through earnings models, discount rates, volatility pricing, positioning, and liquidity.

Those are not the same thing.

That is why the market can look cold or disconnected. It is not measuring whether the world feels safe. It is measuring whether the expected financial damage is large enough to justify lower equity prices.

Right now, the market’s answer appears to be: not yet.

That is the entire story.

Not “risk does not matter.”

Not “everything is fine.”

Not “stocks can never fall.”

Just this: the market believes the crisis is still financially absorbable.

That phrase matters.

Financially absorbable means the crisis may be serious, but not yet serious enough to destroy earnings, break credit markets, force a major policy shock, or trigger a broad liquidation event.

As long as investors believe that, the S&P 500 can keep rising.

What Could Break the Rally?

The bullish case is understandable, but it is not invincible.

There are several things that could break this kind of rally.

1. A sustained oil shock

If oil keeps rising and stays elevated, inflation pressure becomes harder to ignore. That can hurt consumers, pressure corporate margins, and reduce the odds of easier monetary policy.

2. Higher Treasury yields

If investors start demanding higher yields because inflation risk is rising, equity valuations become more vulnerable. This is especially true for expensive growth stocks.

3. Weak earnings revisions

The S&P 500 can look strong as long as earnings expectations hold up. But if companies begin cutting guidance broadly, the rally loses one of its main supports.

4. Credit stress

Equity markets can tolerate geopolitical headlines. They struggle much more when credit markets begin to show stress. If spreads widen sharply, that would be a warning sign.

5. A broader regional escalation

If a contained crisis becomes a larger military or economic shock, the market will have to reprice risk again.

This is why I would not describe the current rally as risk-free. I would describe it as rational but vulnerable.

There is a big difference.

My Take: The S&P 500 Is Not Ignoring the Crisis

My view is simple: the S&P 500 is not ignoring geopolitical risk. It is ranking that risk against other forces.

Right now, those other forces include AI optimism, mega-cap earnings strength, global capital flows into US assets, liquidity, and the belief that the economic damage from the crisis remains manageable.

That is why the market can climb while the world still feels tense.

The S&P 500 is not saying there is no storm. It is saying the ship is still moving.

And until the crisis starts to seriously damage earnings, inflation, credit, or liquidity, investors may continue to treat pullbacks as opportunities rather than reasons to abandon the market.

That is the uncomfortable truth about markets during geopolitical crises.

They do not need the world to be calm.

They only need the future to be less bad than feared.

Conclusion

The S&P 500 can rally during geopolitical crises because markets price expected financial damage, not emotional intensity.

If investors believe a crisis is contained, if oil does not create a lasting inflation shock, if Treasury yields remain manageable, if mega-cap earnings stay strong, and if global capital continues flowing into US assets, the index can rise even while geopolitical tension remains elevated.

That is exactly what makes the current market so fascinating.

The headlines still look tense.

The geopolitical risk is still real.

But the S&P 500 is telling us that investors still believe the earnings engine is intact.

That does not mean the rally cannot fail.

It means the rally has a logic.

And once you understand that logic, the market no longer looks as irrational as it first appears.

FAQs

Why does the S&P 500 rise during geopolitical crises?

Because markets price future expectations. If investors believe the crisis will remain contained or that the worst-case scenario has already been priced in, the S&P 500 can rally even while headlines remain negative.

Is the stock market ignoring geopolitical risk?

Not necessarily. The market may be acknowledging the risk but deciding that the expected financial damage is manageable.

Why does the US market attract money during global crises?

The US offers deep liquidity, strong institutions, reserve-currency exposure, and large companies with global revenue and strong balance sheets.

What is the biggest risk to this kind of rally?

A sustained oil shock that reignites inflation, pushes Treasury yields higher, and forces the Federal Reserve to remain tighter for longer.

Can the S&P 500 keep rising if tensions worsen?

Yes, but only if investors continue to believe the crisis is economically contained. If earnings, inflation, credit, or liquidity deteriorate meaningfully, the rally becomes much more vulnerable.