UAE exits OPEC and reshapes the energy landscape

The United Arab Emirates’ decision to leave OPEC is not just another headline in the energy space it’s a signal the structure of the global oil market may be entering a new phase. Most of the reporting is focused on the short-term consequences for production but the real story is what it means for coordination, credibility and long-term price stability.

From a market standpoint, it’s not just the number of barrels the UAE will produce next month. But to me it’s the loss of cohesion within OPEC+. The group’s power in the past has come from its ability to act as one. When that unity starts to break down, markets begin to ask themselves whether supply discipline can be maintained at all.

And the timing makes it all the more potent. Already elevated tensions at key geopolitical chokepoints such as the Strait of Hormuz mean that any actual or perceived disruption is quickly priced in. “I have seen situations like this where it is not that the supply has changed, but all of a sudden the reliability of the system that manages that supply is in question.

Saudi Arabia, the de facto leader of OPEC, will probably be the most acutely affected by the shift. Its influence has rested on cohesion within the group and the UAE’s departure threatens that cohesion. Instead, you get a more fragmented environment where the competition for market share may start to outweigh coordinated restraint.

Why the UAE’s exit could move oil prices

The logic seems simple enough. If the UAE leaves OPEC and increases production, oil prices should go down. But markets rarely move in such a straight line.

In my experience, uncertainty is more important than supply levels. When a major producer moves outside of a coordinated framework, it creates uncertainty about future production behaviour, not only for that country, but for others who might follow suit. That uncertainty is often enough to send volatility higher and, in many cases, that pushes prices higher through an increased risk premium.

We may be entering a period where geopolitical narratives are as important as supply and demand fundamentals in determining oil prices. This change tends to attract speculative flows and amplify price movements in either direction. Benchmarks like Brent and WTI will reflect not only the current state of play but also the expectations as to how fragmented the market could become.

I am watching the speed at which expectations change, not just data on the output. That alone could keep prices elevated in the absence of near-term shortfalls if traders get the impression OPEC+ has lost control of supply coordination.

Why Liquidity Still Matters More Than Fundamentals

One of the most important realities in modern financial markets is that liquidity often matters more than fundamentals in the short term.

From a macro perspective, markets do not move only because economic conditions improve or deteriorate. They also move because of:

- Liquidity flows.

- Positioning.

- Central bank expectations.

- Passive investing.

- Corporate buybacks.

- And investor psychology.

This helps explain why the S&P 500 can continue reaching record highs even while many parts of the economy still face pressure from:

- Elevated interest rates.

- Expensive debt.

- Slowing growth.

- And geopolitical uncertainty.

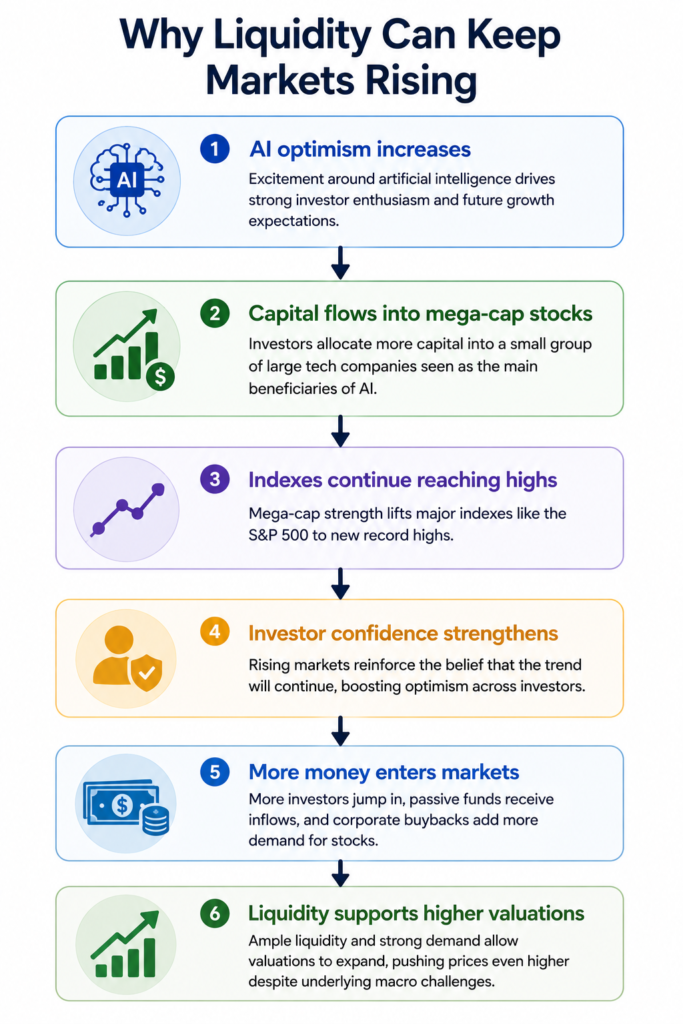

Large technology companies remain one of the strongest drivers behind this trend. Massive enthusiasm surrounding artificial intelligence has concentrated capital flows into a relatively small group of mega-cap stocks that now carry enormous weight inside major indexes.

At the same time, many investors continue positioning for eventual Federal Reserve rate cuts and improved liquidity conditions later in the cycle. That expectation itself can help support markets.

From my perspective, this is one of the reasons the current rally feels both strong and fragile at the same time. Strong because liquidity and momentum remain supportive.

Fragile because valuations increasingly depend on optimistic assumptions about:

- Inflation

- Earnings

- Future growth

- And monetary policy.

If any of those expectations begin to weaken, volatility could return very quickly.

Why Liquidity Can Keep Markets Rising

Why Record Highs Can Still Be Dangerous

Record highs often create the impression that risk is disappearing. But from a macro perspective, the opposite can sometimes be true.

When markets continue rising for extended periods, investor confidence tends to increase rapidly. Optimism grows, positioning becomes more crowded and many participants begin assuming the rally will continue indefinitely. That environment can become fragile.

Not necessarily because the economy suddenly collapses, but because markets begin pricing extremely optimistic assumptions about:

- Growth.

- Inflation.

- Earnings.

- Liquidity.

- And central bank policy.

In other words, markets begin pricing perfection. The problem with perfection is that it leaves very little room for disappointment. If inflation remains sticky, economic growth weakens, bond yields rise further or the Federal Reserve delays future rate cuts, markets may suddenly need to reprice expectations much more aggressively.

This is especially important today because major indexes are increasingly concentrated in a relatively small group of mega-cap technology companies heavily linked to artificial intelligence optimism. That concentration can amplify both upside momentum and downside volatility.

From my perspective, this does not necessarily mean the bull market is over. But it does mean investors should recognize that record highs do not eliminate risk. Sometimes they simply hide it more effectively.

The real issue: inflation, interest rates, and central banks

This is where the story goes beyond energy, and into the wider macroeconomic environment. Oil is not simply another asset class. It is a vital input into the global economy. When energy prices go up, the effect is felt everywhere in transportation, manufacturing and ultimately consumer prices.

I have seen the speed at which an energy shock can flow through into inflation metrics in past cycles. It seldom stays contained. Instead it reverberates through supply chains, jacking up costs across multiple sectors. Therefore, this development is of particular interest for central banks.

If oil prices remain elevated or become more volatile, policymakers face a difficult trade-off. Lowering interest rates to support growth risks reigniting inflation, while keeping rates high to control prices can further slow economic activity. In this context, the likelihood of a “higher for longer” rate environment increases significantly.

There’s also a growing risk of stagflation a scenario where inflation remains elevated while growth weakens. Markets tend to struggle in this environment because it undermines both equities and fixed income simultaneously. From a macro standpoint, this is one of the more complex outcomes to navigate.

Commodities impact: it’s not just oil

Focusing solely on oil would miss the broader ripple effects across the commodity space. Energy sits at the core of nearly every production process, so changes in oil pricing inevitably affect other markets.

As oil rises, so do transportation and logistics costs, which are passed on to the price of goods from industrial metals to agricultural products. Natural gas markets may also respond, especially where energy substitution is important. Fertilizer costs are tied to energy inputs and any price changes will eventually translate into food inflation.

From a market perspective these second order effects are often more important than the initial move in oil itself. They impact inflation expectations, corporate margins, and even consumer behavior.

There’s also a clear divergence in how different sectors respond. Energy producers and commodity exporters tend to benefit from higher prices, while industries heavily reliant on fuel such as airlines, transportation, and consumer goods face increasing pressure. This creates a more uneven market environment, where sector rotation becomes a key theme.

Macroeconomic consequences of the UAE leaving OPEC

The global impact of this decision will not be evenly distributed. Emerging markets, particularly those that depend heavily on energy imports, are likely to be the most vulnerable. Higher oil prices can widen trade deficits, weaken local currencies, and intensify inflation pressures all of which can destabilize economic growth.

During times such as these capital tends to flow into what are considered safe havens. The US dollar usually appreciates and bond markets become more sensitive to inflation expectations. Such changes can also exacerbate global financing conditions, especially for countries with larger external debts.

For large economies the implications are different. The United States is likely to be relatively insulated given its energy production profile, but it is still very sensitive to inflation dynamics. Europe’s structural vulnerability will persist because of its dependence on imported energy; China’s path will be heavily shaped by the recovery of its domestic demand and policy response.

From my perspective, this is where the real story unfolds not in the immediate reaction, but in how these macro forces evolve over the coming months.

Is OPEC breaking or evolving?

The key question is whether this marks the beginning of a broader breakdown within OPEC or simply a transition into a different kind of structure.

If more countries prioritize national production strategies over collective discipline, the organization could shift away from being a tightly coordinated cartel toward a looser alliance. That would fundamentally change how oil markets behave, increasing volatility and reducing predictability.

Saudi Arabia and Russia are likely to attempt to maintain influence, but their ability to do so depends on continued alignment from other members. Without that, the balance of power within the energy market could shift toward a more competitive, less controlled system.

What I’m monitoring closely in the near term is how other OPEC+ members respond, whether the UAE significantly alters its production strategy, and how oil prices react over the next few weeks. These signals will provide early clues about whether this is an isolated event or the start of a broader trend.

Conclusion: This is bigger than oil

The UAE leaving OPEC is not just an energy story it’s a macroeconomic inflection point. It touches inflation, interest rates, global growth, and financial markets all at once.

From where I stand, this development suggests a move toward a more fragmented and less predictable energy landscape. Markets will need to adjust quickly, and that adjustment is unlikely to be smooth.

From my perspective, the key issue is not whether markets can continue rising, but whether current valuations and expectations leave enough room for the economy and central banks to disappoint.

FAQs

Why did the UAE leave OPEC?

The decision likely reflects a desire for greater production flexibility and strategic independence.

Will oil prices rise?

Not necessarily in a straight line, but volatility and risk premiums are likely to increase.

How does this affect inflation?

Higher energy costs can feed directly into broader inflation across the economy.

Could this impact interest rates?

Yes. Central banks may delay rate cuts or maintain higher rates for longer.

Who benefits from this move?

Energy producers and commodity-exporting countries.

Who is most at risk?

Energy-importing economies and sectors sensitive to fuel costs.