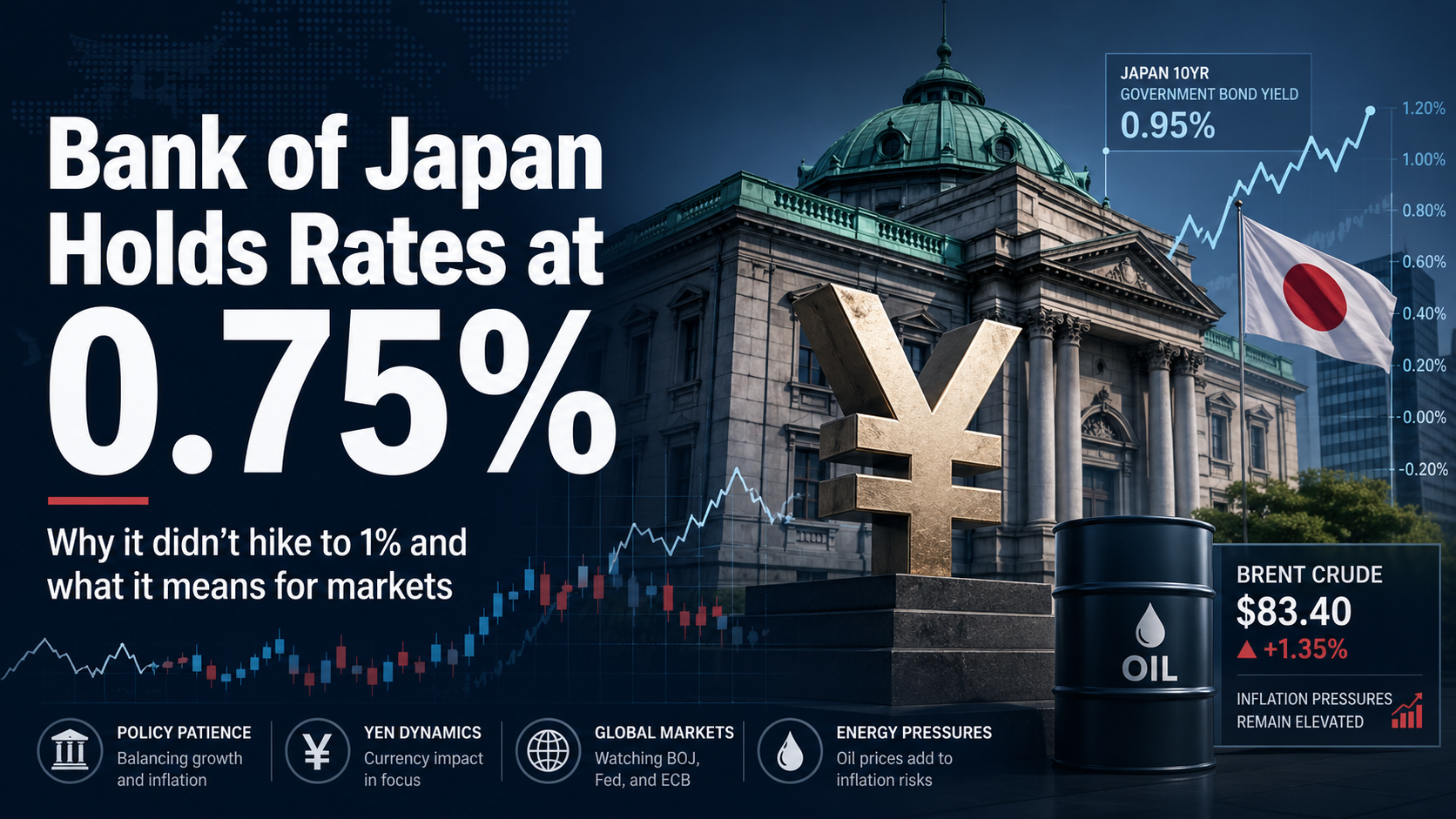

The Bank of Japan has held interest rates at 0.75%, but the decision is far from a calm message for markets. The BoJ chose not to move at its April meeting, although the internal vote shows growing pressure to further tighten monetary policy: the decision passed by 6 votes to 3, with the three dissenters favoring a rate hike to 1%.

The key issue is not only that Japan’s central bank kept rates unchanged, but why it did so. Japan is now facing an uncomfortable mix: higher inflation due to rising oil prices and tensions in the Middle East, but also weaker economic growth. In fact, the BoJ lowered its GDP forecast for fiscal 2026 to around 0.5%, down from the 1% it had projected in January.

I don’t think this is a good break. It is a pause for defense. The Bank of Japan is buying time because raising rates too quickly could make the economy even weaker. However, it can’t ignore the new inflationary pressure coming from energy and imported goods.

Why the Bank of Japan Matters to Global Markets

The Bank of Japan Leaves Rates at 0.75%, but the Message Is Not Neutral

The market had a good idea of what the BoJ would do, but the details of the vote change the meaning a lot. When three board members are already asking for rates to go up to 1%, the message stops being just cautious and starts to sound more limiting.

The Bank of Japan has now held rates steady for a third consecutive meeting, after raising its benchmark rate to 0.75% in December 2025, its highest level in three decades. Since then, the central bank has preferred to observe how that tightening affects companies, households, and financial markets.

A pause in rates doesn’t always mean easing in the markets. That little detail is important: the BoJ didn’t raise rates today, but it didn’t say it wouldn’t do so in the future. The central bank actually raised its inflation forecasts a lot. For the current fiscal year, the core CPI, which does not include fresh food, is now expected to be 2.8%, up from the 1.9% forecast in January.

Because of the change in forecasts, this decision is like “hold rates, but with a warning.” The real message for investors is that the Bank of Japan still relies on data and that a future rate hike is possible if inflation stays above target.

Why the Yen Carry Trade Matters So Much

One of the most important reasons the Bank of Japan matters far beyond Japan itself is the yen carry trade.

For years, extremely low Japanese interest rates allowed investors to borrow money cheaply in yen and invest those funds into higher-yielding assets around the world. This became one of the hidden engines of global liquidity.

When Japanese rates remain extremely low, borrowing costs in yen stay attractive. That liquidity can then flow into:

- U.S. equities.

- Emerging markets.

- Global bonds.

- Technology stocks.

- And even crypto assets.

From a macro perspective, this means the Bank of Japan indirectly influences financial conditions worldwide. That is why markets pay such close attention to any potential shift in BOJ policy.

If Japanese rates rise aggressively, the economics of the carry trade begin to weaken. Investors may reduce leverage, unwind positions and repatriate capital back into Japan. That process can create volatility across global markets very quickly. This is one of the reasons many investors were relieved that the BOJ did not move rates to 1%.

A sudden tightening cycle in Japan could have acted as a liquidity shock for global financial markets already dealing with:

- Elevated U.S. rates.

- Geopolitical uncertainty.

- And fragile risk sentiment.

From my perspective, the Bank of Japan is no longer just a domestic central bank story. It is increasingly a global liquidity story.

Why the Bank of Japan Is Holding Rates Despite Inflation

The most important question is obvious: if inflation is rising, why is the Bank of Japan not raising rates too?

The answer is in where that inflation came from. The Bank of Japan is under a lot of pressure because of high oil and commodity prices, especially because of problems in the Middle East. Japan relies heavily on imported energy, so higher crude oil prices directly affect the costs of doing business and the real income of households.

The issue is that this inflation isn’t just caused by strong demand in the country. If prices are going up because energy is getting more expensive, raising rates may not fix the real problem and could still hurt consumption, investment, and business profits.

That’s why I think the Bank of Japan is stuck between two risks. If it raises rates too soon, it could make the economy slow down even more. But if it waits too long, it might lose credibility because inflation is already clearly above the 2% target.

That is the hard balance: keeping rates the same gives the BoJ more time, but it doesn’t ease the pressure. On the other hand, the split vote shows that some members of the central bank already think that monetary normalization should happen faster.

Why Japan Still Influences Wall Street

Many investors still view the Bank of Japan as a mostly domestic central bank story. But from a macro perspective, that view is increasingly outdated.

Japan remains deeply connected to the global financial system through:

- Liquidity flows.

- Sovereign bond markets.

- Currency markets.

- And the yen carry trade.

When Japanese monetary policy stays extremely accommodative, global financial conditions often become more supportive for risk assets worldwide. That liquidity does not stay inside Japan.

It spreads across:

- U.S. equities.

- Global bonds.

- Emerging markets.

- Technology stocks.

- And crypto markets.

This is one of the reasons Wall Street watches the BOJ so closely despite Japan’s relatively slow domestic growth.

Markets understand that a meaningful tightening cycle in Japan could trigger:

- Leverage reductions.

- Carry trade unwinds.

- Stronger yen volatility.

- And tighter global financial conditions.

From my perspective, this is why the Bank of Japan has become increasingly important for investors far beyond Tokyo. It is no longer just a Japan story. It is a global liquidity story.

What the BoJ’s Rate Hold Means for Markets

The choice has a number of effects on markets. The first is that the Bank of Japan doesn’t want to cause a sudden tightening of financial conditions. That could be good for Japanese stocks in the short term because it keeps valuations from dropping right away.

But the second interpretation is less comfortable: if the BoJ keeps rates where they are now but raises its inflation forecasts, the market might think that the next hike has only been pushed back. And when markets start to factor in future rate hikes, currencies, bonds, and sectors that are sensitive to interest rates are hit the hardest.

Impact on the Japanese Yen

The yen is probably the asset most sensitive to this decision. In theory, holding rates could weaken the currency because it does not increase the appeal of Japanese assets. In practice, however, a 6-3 vote and higher inflation forecasts may strengthen expectations that the BoJ will hike later.

That is why, in my opinion, the yen may react more to the tone of the statement than to the 0.75% rate itself. If investors understand that the central bank is closer to another hike, the yen could find support, especially against currencies whose central banks are closer to cutting rates.

Impact on the Nikkei 225

The effect on Japanese stocks is mixed. Not raising rates today, on the other hand, keeps companies from feeling pressure right away. On the other hand, a stronger yen is usually bad news for big Japanese exporters because it makes their sales abroad worth less when they are converted back into yen.

Also, if Japanese rates keep going up in the next few months, growth sectors may have to deal with lower valuations. The market doesn’t just look at how much money you make right now; it also looks at how much money will cost in the future. And a monetary policy that is less flexible changes the rules of the game.

Impact on Bonds and the Carry Trade

In bonds, the interpretation is also clear: if expectations of future hikes increase, Japanese government bond yields could remain under upward pressure. That matters not only for Japan but also for global markets, because ultra-low Japanese rates fueled carry trade strategies for years.

As Japan moves away from its long period of near-frozen rates, many international flows need to adjust. It does not happen overnight, but every restrictive signal from the BoJ forces investors to reassess positions in currencies, fixed income, and risk assets.

The Key Is the Message: A Pause Today, a Possible Hike Tomorrow

It would be a big mistake to think that this decision shows weakness on the part of the Bank of Japan. That’s not how I see it. The BoJ doesn’t want to raise rates too quickly, but it also doesn’t want to look like it’s not worried about inflation.

The fact that three members voted for a hike to 1% is highly relevant. In central banking, dissents often serve as a preview of the debate ahead. Today it is three votes; in the next meetings, if oil continues to pressure prices and inflation does not ease, that bloc could gain weight.

It’s also important to pay attention to how growth is talked about. Not only did the BoJ raise its inflation forecasts, but it also lowered its growth outlook. That mix of higher prices and less activity is especially hard for any central bank to deal with because it makes it harder to take strong action.

Japan is not stopping because everything is fine, in other words. It is taking a break because the situation has become more difficult.

Quick Table: Likely Market Impact by Asset

| Asset | Likely Impact | Market Interpretation |

|---|---|---|

| Japanese yen | Bullish if hike expectations rise | Market focuses on the divided vote and inflation |

| Nikkei 225 | Mixed / pressure on exporters | Higher future rates and a potentially stronger yen |

| Japanese bonds | Upward pressure on yields | Greater probability of additional hikes |

| Japanese banks | Potentially positive | Higher rates may improve margins |

| Exporters | Negative risk | A stronger yen reduces competitiveness |

| Carry trade | Higher volatility | Funding in yen becomes less attractive |

My Take: This Is Not a Dovish Pause, It Is a Defensive Pause

You shouldn’t read this decision by the Bank of Japan as a classic dovish signal. This is not a central bank holding rates because the economy is doing well and inflation is under control. This is a central bank holding rates because inflation is going up because of things outside the economy, while growth is slowing down.

And that makes the market see things in a very different way.

When I look at a rate decision, I don’t just look at the number. Of course, the 0.75% rate is important, but the upward revision to inflation, the downgrade to growth, and the split vote are even more important. Together, they show that the Bank of Japan is getting more and more uneasy.

That is why the next signals will be very important to the markets: oil prices, wages in Japan, core inflation, the yen’s performance, and Kazuo Ueda’s tone. If those signs stay tense, a rise to 1% could quickly become the main point of discussion again.

Conclusion: Japan Is Buying Time, but Markets Are Already Pricing in More Pressure

The Bank of Japan has kept rates at 0.75%, but the decision does not clear up the uncertainty. On the contrary, it confirms that Japanese monetary policy is entering a more complicated phase: higher inflation, weaker growth, and an increasingly divided policy board.

For markets, the key point is not only that the BoJ did not raise rates. The key is that three members already wanted to do so, inflation expectations were revised higher, and oil is once again acting as a threat to an economy that relies heavily on imported energy.

My conclusion is clear: the Bank of Japan has not closed the door to further rate hikes. It has simply decided to wait. And in markets, when a central bank waits but leaves signs of pressure, a pause can move assets just as much as a hike.

FAQs About the Bank of Japan and Interest Rates

Why is the Bank of Japan holding rates?

Because it wants to assess the impact of the previous hike to 0.75% on companies and households, while avoiding further damage to economic growth. The problem is that inflation has picked up due to higher oil prices, making the decision much more complicated.

What are interest rates in Japan right now?

The Bank of Japan’s short-term benchmark rate remains at 0.75%, after the central bank decided not to change it at its April meeting.

Could the Bank of Japan raise rates to 1%?

Yes, that possibility remains open. Three policy board members already supported raising rates to 1%, which shows there is internal pressure within the BoJ to continue normalizing monetary policy.

How does this decision affect the yen?

It could support the yen if the market interprets the current pause as increasing the likelihood of a future hike. Although holding rates is usually negative for a currency, the restrictive tone of the decision may offset that effect.

Is this good or bad news for Japanese stocks?

It is mixed. In the short term, not raising rates avoids immediate pressure on valuations. But if the yen strengthens and expectations for more hikes rise, exporters and growth companies could come under pressure.