Artificial intelligence may turn out to be the most powerful deflationary force of the 2020s but not in the simple, magical way Silicon Valley sometimes sells it.

The popular version goes like this: AI gets smarter, workers become more productive, companies produce more with less, and prices fall. That story is not wrong. It is just incomplete. The real picture is messier. AI is deflationary in some places, inflationary in others, wildly bullish for a handful of S&P 500 giants, dangerous for certain white-collar wages, and potentially transformative for the way investors think about margins, labor, software, energy and capital spending.

The way I see it, AI is not just another productivity tool. It is a cost-repricing machine. It attacks the price of knowledge work, software development, customer support, advertising, research, design, financial analysis and eventually parts of physical labor through robotics. Any technology that can compress the cost of producing intelligence, code, content, logistics decisions and business analysis has the potential to push prices down across the economy.

But there is a catch: before AI can lower prices, someone has to pay for the chips, data centers, energy, cloud infrastructure and talent required to run it. That is why the AI economy currently looks inflationary in the short term and deflationary in the long term.

In other words, AI may be deflationary the same way railroads, electricity, the internet and cloud computing were deflationary: not instantly, not evenly, and not without bubbles, winners, losers and painful labor-market transitions.

Why AI Could Become Deflationary

The basic deflationary argument is simple: when technology lowers the cost of production, competition eventually forces companies to pass some of those savings to customers.

That is the heart of the AI deflation thesis. If a company can handle customer service with AI agents, write software faster, produce marketing campaigns in hours instead of weeks, automate compliance checks, improve inventory forecasting, reduce fraud, summarize legal contracts, optimize logistics and accelerate research, then the cost of delivering a product or service falls.

At first, companies may keep the savings as higher profit margins. But over time, competitors copy the same tools. Once everyone has access to similar AI capabilities, productivity becomes table stakes. McKinsey makes this point clearly: productivity improvements alone are unlikely to create a durable advantage because competition tends to erode those gains and shift value toward customers.

That is deflationary.

It means AI does not need to destroy demand to lower prices. It can lower prices by increasing supply, reducing unit costs and making companies compete more aggressively. In software, for example, the marginal cost of creating features, documentation, testing scripts and customer support flows could fall dramatically. In media, the cost of producing basic content is already collapsing. In finance, junior analytical work can be accelerated. In retail, demand forecasting can reduce waste. In manufacturing, AI-assisted robotics can lower error rates and downtime.

The most important phrase here is marginal cost. If AI lowers the marginal cost of producing an extra unit of output an extra report, an extra software feature, an extra ad, an extra customer interaction then prices eventually come under pressure.

That is why Sam Altman’s broad claim that AI could create “massively deflationary pressure” is not absurd. His argument is that AI will make work done in front of a computer dramatically cheaper, and that robotics could eventually extend the same logic into the physical economy.

I do not think the question is whether AI is deflationary. I think the real question is: deflationary for whom, when and after how much capital destruction?

The Five Deflationary Channels of AI

AI can push prices lower through several channels at once.

| Deflationary channel | How it works | Likely impact |

|---|---|---|

| Labor substitution | AI performs tasks previously done by humans | Lower wage pressure in exposed jobs |

| Productivity gains | Workers produce more output per hour | Lower unit costs |

| Software abundance | Code, apps and digital tools become cheaper to build | Cheaper software and services |

| Better price discovery | Consumers and businesses compare options faster | Less pricing power for sellers |

| Automation of overhead | Admin, support, legal, finance and HR workflows shrink | Higher margins or lower prices |

The first channel is labor. Goldman Sachs Research estimates that around 300 million jobs globally are exposed to AI automation and that AI could potentially automate tasks accounting for 25% of all U.S. work hours.

That does not mean 300 million people lose their jobs. It means a large share of tasks can be changed, compressed or automated. The difference matters. AI is more likely to remove tasks before it removes entire occupations. But if a company can reduce the number of hours needed in customer support, coding, design, legal review, marketing production or financial analysis, then wage growth in those areas becomes harder to sustain.

The second channel is productivity. If AI lets a ten-person team do what previously required twenty people, the output per worker rises. When productivity rises faster than wages, unit labor costs fall. That is one of the cleanest paths to disinflation.

The third channel is software abundance. Software has already been eating the world for decades. AI may now eat the cost of making software. If code generation keeps improving, the price of building internal tools, websites, workflows and apps should fall. That could hurt legacy software vendors with expensive seats and weak differentiation.

The fourth channel is price transparency. AI shopping agents, procurement bots and automated negotiation tools could make it easier for consumers and companies to compare prices in real time. When buyers become smarter, sellers lose pricing power.

The fifth channel is overhead compression. Every large company has layers of administrative work: reporting, compliance, scheduling, procurement, onboarding, customer tickets, sales operations, internal documentation and management analysis. AI can attack those costs directly.

This is why I think AI’s biggest deflationary effect may not come from humanoid robots replacing factory workers. It may come from boring workflow automation inside large companies.

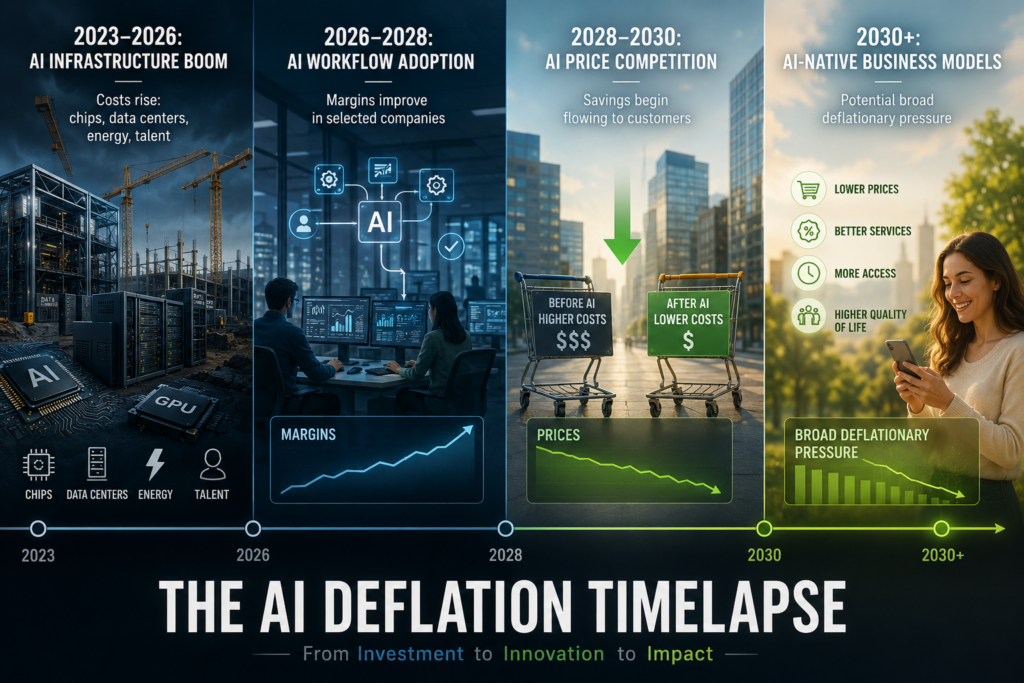

Why AI Is Inflationary Before It Becomes Deflationary

Here is the paradox: AI may lower prices later by raising costs now.

The AI boom requires enormous upfront investment in semiconductors, servers, cloud infrastructure, data centers, electricity, cooling systems, networking equipment and specialized talent. Reuters reported that Alphabet, Amazon, Meta and Microsoft were expected to collectively invest about $650 billion in AI-related infrastructure in 2026, up sharply from $410 billion in 2025, according to Bridgewater analysis.

That kind of spending is not deflationary in the short term. It increases demand for chips, construction labor, engineers, land, power equipment, copper, cooling technology and electricity. It can push up prices in exactly the sectors needed to build the AI economy.

Goldman’s framing, as summarized by Fortune, is basically an “up then down” story: AI spending can be inflationary first, then disinflationary later if productivity gains become broad enough. Fortune also noted Goldman’s finding that, as of March, there was no meaningful relationship yet between AI and economy-wide productivity, even though some measured tasks showed gains around 30%.

That distinction is critical. A chatbot making one employee 30% faster on a specific task is not the same as the entire U.S. economy becoming 30% more productive. For AI to become a true deflationary force, it has to move from pilots to workflows, from workflows to business models, and from business models to industry-wide price competition.

Right now, a lot of AI is still in the expensive buildout phase.

That is why I would describe today’s AI economy like this:

The exact timeline could be wrong. But the sequence matters.

The S&P 500 Impact: Why Big Tech Is at the Center of the Story

AI is already reshaping the S&P 500 because the index is heavily influenced by the largest technology and platform companies. The companies most exposed to the AI boom include Nvidia, Microsoft, Alphabet, Amazon, Meta, Apple, Tesla and Broadcom either because they sell AI infrastructure, run cloud platforms, control consumer ecosystems or have massive data and distribution advantages.

The current AI trade has two sides.

On one side are the infrastructure winners: Nvidia, chip suppliers, cloud platforms, data center operators, power companies and hardware providers. Goldman Sachs Research has noted that equity gains have been concentrated in semiconductors, hyperscalers, data center operators, technology hardware providers and power companies.

On the other side are the productivity beneficiaries: companies that can use AI to reduce labor costs, improve margins, automate workflows and defend pricing. These may include banks, insurers, software companies, retailers, logistics firms, healthcare administrators, media companies and professional services businesses.

The first group benefits when AI spending rises. The second group benefits when AI actually works.

That difference is everything for investors.

If you own Nvidia, you care about GPU demand, inference growth, data center expansion and whether hyperscalers keep spending. If you own Microsoft, Amazon or Alphabet, you care about whether AI spending turns into cloud revenue and customer lock-in. If you own Meta, you care about whether AI improves ad targeting, content recommendation and engagement. If you own a bank, insurer or retailer, you care about whether AI lowers headcount growth and operating costs.

In the short run, the market has rewarded the companies selling picks and shovels. In the long run, it may reward the companies that convert AI into cash flow.

How AI Affects the Largest S&P 500 Companies

| Company | AI role | Deflationary exposure | Investor question |

|---|---|---|---|

| Nvidia | Core AI chip supplier | Enables cheaper computation over time | Can demand stay ahead of competition and chip cycles? |

| Microsoft | Cloud, Copilot, enterprise AI | Automates office work and software workflows | Can AI revenue justify massive capex? |

| Alphabet | Search, cloud, AI models, ads | Lowers search, ad and software costs | Does AI protect or disrupt search margins? |

| Amazon | AWS, logistics, retail automation | Reduces fulfillment, cloud and retail costs | Can AI lift margins across AWS and retail? |

| Meta | AI ads, recommendation systems | Lowers content and ad targeting costs | Can AI keep increasing ad efficiency? |

| Apple | Devices, consumer AI distribution | Could commoditize some software features | Can Apple make AI a device upgrade cycle? |

| Tesla | Robotics, autonomy, manufacturing AI | Potentially lowers transport and labor costs | Can autonomy become real cash flow? |

The clearest winner so far has been the infrastructure layer. But the bigger deflationary story may come later from companies that use AI to reduce operating expenses.

For example, a large bank can use AI to summarize earnings calls, process documents, detect fraud, assist compliance, support customers and accelerate software development. A retailer can use AI to forecast demand, reduce inventory waste, automate product descriptions and optimize pricing. An insurer can use AI to process claims faster. A media company can produce more content with fewer people. A software company can reduce support and engineering costs.

Each example is small on its own. Across the S&P 500, the combined effect could be enormous.

But there is a risk: if every company uses AI to cut costs, those savings may not remain as profits. Competition may force them into lower prices, better service or higher customer expectations. That is why AI can be bullish for productivity but bearish for pricing power.

Wages: AI Is Deflationary for Some Workers, Inflationary for Others

AI will not affect all wages equally.

For workers whose jobs consist of repeatable digital tasks, AI is a direct source of wage pressure. Junior developers, copywriters, support agents, analysts, paralegals, designers, translators, recruiters and administrative workers are all exposed to some degree. The work may not disappear, but the number of people needed to produce the same output may fall.

Goldman’s labor-market research points to displacement risk in tech, knowledge and creative sectors, while also noting that AI infrastructure buildout can create demand for construction workers, engineers, electricians and power-related jobs. Goldman also expects hundreds of thousands of jobs tied to power and data-center demand in the U.S. by 2030.

That means AI could be deflationary for white-collar wages while inflationary for electricians.

This is one of the most underappreciated points in the debate. AI does not simply “lower wages” or “raise wages.” It changes the wage map.

Likely wage pressure:

– Junior analysts

– Customer support

– Basic coding

– Content production

– Admin and back-office work

Likely wage support:

– AI engineers

– Data center construction

– Power-grid workers

– Cybersecurity

– Robotics technicians

– High-trust human experts

In my view, the most vulnerable workers are not necessarily the least intelligent. They are the workers whose output is easiest to measure, replicate and integrate into automated workflows.

The safest workers will be those who combine judgment, taste, trust, physical execution, domain expertise and responsibility. AI can draft a legal memo. It cannot yet carry the professional liability of being the attorney of record. AI can suggest a diagnosis. It cannot fully replace the trust relationship between doctor and patient. AI can generate a financial model. It cannot sit with a CEO and own the consequences of a capital allocation decision.

That distinction matters for wages.

Prices: What Could Actually Get Cheaper?

AI will not make everything cheaper. Rent will not fall just because a chatbot writes emails faster. Healthcare will not automatically become affordable because doctors use AI assistants. Food prices will not collapse unless AI changes agriculture, logistics, labor and energy costs.

But some categories are more exposed to AI-driven price compression.

| Category | Probability of AI-driven price pressure | Why |

|---|---|---|

| Software tools | High | Code generation and feature commoditization |

| Customer support | High | AI agents reduce service costs |

| Digital marketing | High | Content and ad production become cheaper |

| Professional research | Medium-high | Summaries, analysis and data work automated |

| Legal/admin services | Medium | Routine documents and review workflows shrink |

| Healthcare admin | Medium | Claims, billing and scheduling automation |

| Physical goods | Medium-low | Depends on robotics, logistics and energy |

| Housing | Low | Land, zoning, rates and supply dominate |

The first wave of AI deflation is likely to appear in digital services, not supermarkets.

I expect software to be one of the most interesting battlegrounds. If AI lets companies build custom internal tools quickly, some expensive software-as-a-service products may face pricing pressure. Why pay for a bloated seat-based platform if an AI-assisted team can build a narrower internal tool for less?

The same logic applies to content. Generic content is already becoming abundant. That does not mean great journalism, entertainment or analysis becomes worthless. It means average content becomes cheaper, faster and less defensible.

The danger for companies is that AI may improve productivity while destroying differentiation.

Investments: The AI Trade Is Bigger Than Nvidia

From an investor’s perspective, the AI deflation story creates four major baskets.

| Basket | Examples | What investors are betting on |

|---|---|---|

| Infrastructure | Nvidia, data centers, networking, power | AI demand keeps growing |

| Platforms | Microsoft, Amazon, Alphabet, Meta | AI becomes embedded in cloud and consumer products |

| Productivity beneficiaries | Banks, insurers, software users, retailers | AI lowers operating costs |

| Disrupted incumbents | Legacy software, outsourcing, low-end services | AI compresses pricing power |

The infrastructure trade has already been massive. Goldman notes that investors have focused heavily on near-term earnings beneficiaries of AI spending, especially semiconductors, hyperscalers, data center operators, hardware providers and power companies.

But the second phase may be more subtle. Investors will have to ask: which companies can use AI to expand margins without giving all the savings away to customers?

That is harder than buying the obvious chip winner.

A company with high labor costs, repeatable workflows and strong distribution could become an AI productivity winner. But if the industry is highly competitive, those productivity gains may flow to customers instead of shareholders. Airlines, retail and commodity-like services may struggle to keep AI savings. Software platforms with strong ecosystems may keep more of the value.

This is why AI could be deflationary for the economy but still uneven for stocks.

A productivity boom does not automatically mean every stock wins. Sometimes productivity destroys pricing power. Sometimes it shifts profits from labor to capital. Sometimes it moves value from application companies to infrastructure providers. Sometimes it benefits consumers more than shareholders.

That is the investment puzzle of the decade.

The Bear Case: What If AI Does Not Deliver?

The skeptical case deserves respect.

So far, many companies are spending heavily on AI without clear economy-wide productivity gains. McKinsey describes an AI paradox: adoption and investment are rising, but sustained performance impact remains elusive for many companies. As of late 2025, nearly nine out of ten companies had deployed AI in at least one function, yet most respondents reported not seeing significant value from those investments.

That is a warning sign.

AI could disappoint in several ways:

| Risk | Why it matters |

|---|---|

| Productivity gains stay narrow | AI helps with tasks but not full business processes |

| Energy costs rise | Data centers make electricity more expensive |

| Capex becomes excessive | Companies overbuild infrastructure |

| Models commoditize | AI providers struggle to earn attractive returns |

| Regulation slows adoption | Legal, copyright and privacy risks increase |

| Workers resist adoption | Bad implementation creates backlash |

| Quality issues persist | Hallucinations and errors limit mission-critical use |

The worst-case scenario is not that AI does nothing. The worst case is that AI creates huge capital spending, higher electricity demand, labor disruption and inflated market expectations — without generating enough productivity to offset the costs.

That would make AI inflationary, not deflationary.

Some Federal Reserve officials have already warned about the uncertainty. Reuters reported that Chicago Fed President Austan Goolsbee argued rising productivity could restrain inflation or potentially boost it if expectations of future gains cause businesses and households to spend too aggressively before the productivity actually arrives.

That is the macro risk: the economy prices in an AI productivity miracle before the miracle shows up.

My Base Case: First Inflationary, Then Deflationary

My base case is simple: AI is inflationary in the buildout phase, disinflationary in the adoption phase and potentially deflationary in the maturity phase.

The buildout phase is what we are living through now. Chips, power, data centers and talent are expensive. Investors reward infrastructure. Hyperscalers spend aggressively. The S&P 500 becomes more dependent on AI leaders.

The adoption phase comes when companies stop experimenting and start redesigning workflows. That is when AI moves from “cool demo” to “operating model.” Headcount growth slows. Margins improve. Some wages come under pressure. Back-office costs fall.

The maturity phase comes when AI becomes common. At that point, the competitive advantage fades. Customers expect lower prices, faster service and better products. Companies that cannot differentiate get squeezed. Consumers benefit, but weaker businesses lose pricing power.

That is the real deflationary force.

Not “AI makes everything free.”

More like: AI makes intelligence cheaper, and cheaper intelligence eventually makes many products and services cheaper.

Final Takeaway

Artificial intelligence could be the biggest deflationary force of the decade because it attacks the cost of knowledge work, software, operations, customer service, analysis and eventually physical automation.

But the path will not be smooth. In the short term, AI is creating inflationary pressure through massive investment in chips, data centers, energy and talent. In the medium term, it will pressure wages in exposed white-collar sectors while supporting demand for technical, infrastructure and power-related workers. In the long term, if productivity gains spread broadly, AI could lower unit costs across large parts of the economy.

For companies, the message is clear: AI is not just a tool. It is a margin test. The winners will use it to redesign workflows, products and business models. The losers will use it as a bolt-on productivity toy and then wonder why competitors are cutting prices.

For investors, the message is even sharper: the AI trade is moving from hype to proof. Infrastructure winners have captured the first wave. The next wave belongs to companies that can turn AI into durable cash flow.

For workers, the lesson is uncomfortable but useful: the safest jobs will not be the ones AI cannot touch at all. They will be the ones where AI increases the value of human judgment.

And for the economy, the big question is still open: will AI create enough productivity to offset its own enormous cost?

If the answer is yes, AI may not just change technology. It may change the value of money itself.

FAQs

Is AI deflationary or inflationary?

AI is likely both. It is inflationary in the short term because companies are spending heavily on chips, data centers, energy and talent. It may become deflationary later if productivity gains spread widely and reduce the cost of goods and services.

Why would AI lower prices?

AI can lower prices by reducing labor costs, increasing output per worker, automating overhead, making software cheaper to build and increasing price transparency for buyers.

Which companies benefit most from AI deflation?

Infrastructure providers benefit first: chipmakers, cloud platforms, data centers and power suppliers. Later, companies with high labor costs and repeatable workflows may benefit if they can convert AI productivity into higher margins.

Will AI reduce wages?

AI may pressure wages in jobs built around repeatable digital tasks, especially in support, basic coding, content, research and admin work. But it may raise wages for AI engineers, electricians, data center workers, cybersecurity experts and high-trust professionals.

What is the biggest risk to the AI deflation thesis?

The biggest risk is that AI spending rises faster than AI productivity. If companies spend hundreds of billions on infrastructure but fail to produce broad efficiency gains, AI could become an inflationary investment bubble instead of a deflationary productivity boom.