The five largest companies in the world are no longer treating artificial intelligence as a product feature, a marketing trend, or a side experiment. They are reorganizing themselves around it.

NVIDIA, Alphabet, Apple, Microsoft and Amazon sit at the top of the global market-cap ranking in early May 2026, with NVIDIA leading the list and valued at roughly $4.7 trillion to $4.8 trillion depending on the tracker. That alone says a lot about where the market believes the next decade of value creation will come from.

But here is where I become both excited and cautious.

I do believe AI is real. I do believe it will transform software, cloud computing, advertising, consumer devices, search, robotics, healthcare, finance and probably many industries we are still underestimating. But I also think the market is starting to behave as if the final outcome is already guaranteed.

And that is dangerous.

When the biggest companies in the world all decide to spend hundreds of billions of dollars on the same technological future, the question is no longer simply: “Will AI grow?”

The better question is:

Will AI generate enough cash flow, fast enough, to justify the infrastructure, debt, valuations and expectations being built around it?

That is the real story. Not just artificial intelligence. Not just NVIDIA. Not just Big Tech earnings.

The real story is that AI has become an industrial investment cycle and industrial investment cycles can create enormous productivity gains, but they can also create overcapacity, overleveraging and brutal market corrections.

AI Is No Longer a Side Project for Big Tech

A few years ago, most people still talked about AI as software. Chatbots, copilots, recommendation systems, image generators, search assistants, coding tools. Useful, impressive, sometimes overhyped but still mostly digital products sitting on top of existing infrastructure.

That phase is over.

The AI race has moved from apps to infrastructure. Big Tech is now competing through data centers, GPUs, custom chips, cloud capacity, energy contracts, networking systems, model training, inference capacity and distribution.

That is why this cycle feels so different from previous software booms.

Software used to scale with almost magical margins. Build once, distribute globally, collect recurring revenue. AI does not work exactly like that. The best AI models need massive compute. Massive compute needs chips. Chips need supply chains. Supply chains need factories. Data centers need land, power, cooling, fiber, memory, storage and financing.

In other words, AI is not just a software revolution. It is becoming a capital expenditure revolution.

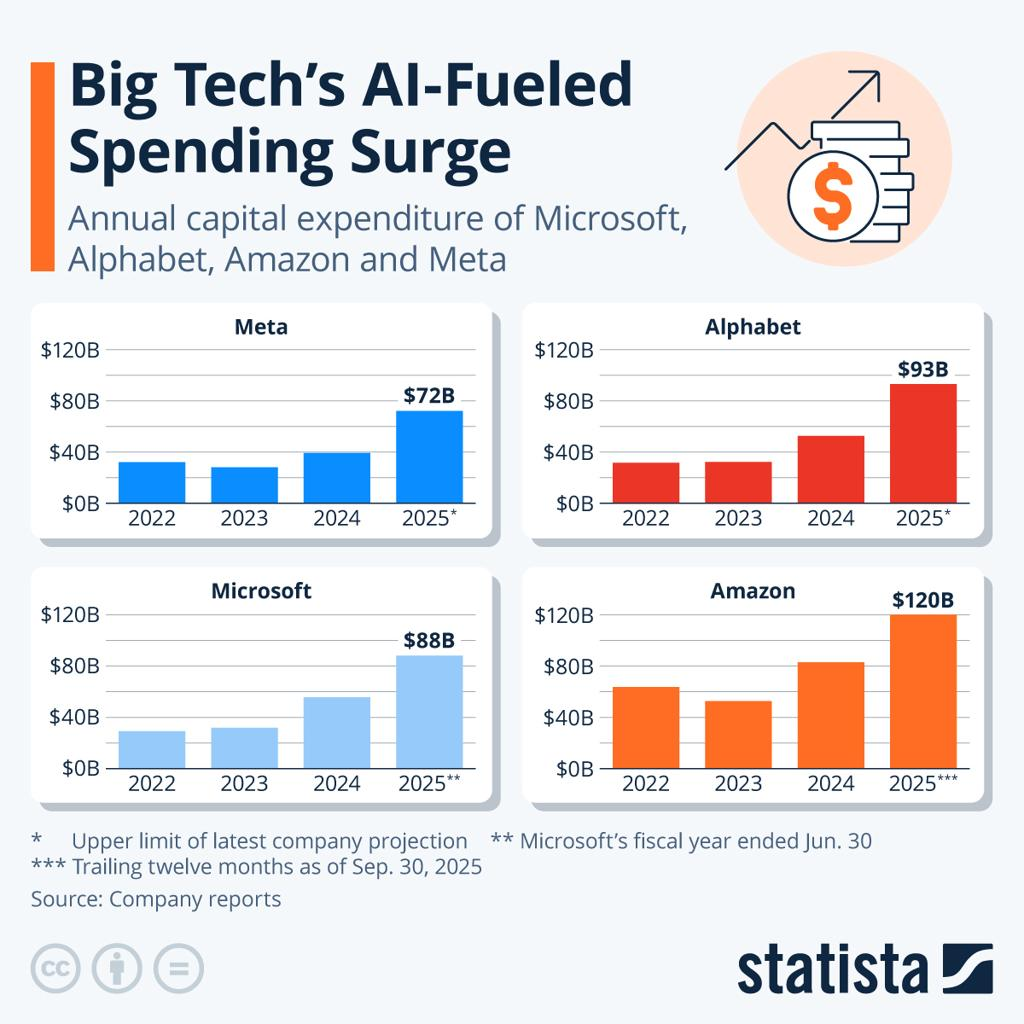

Bridgewater Associates estimated that Alphabet, Amazon, Meta and Microsoft alone could invest around $650 billion in AI infrastructure in 2026, up from roughly $410 billion in 2025. That is an extraordinary number. It means the AI race is not being fought with slogans. It is being fought with balance sheets.

And that is where I think many investors are missing the nuance.

The demand for AI can be real, and the investment cycle can still become financially dangerous. Both things can be true at the same time.

A company can be right about the future and still overpay for getting there too early.

NVIDIA Has Become the Center of Gravity of the AI Economy

When I listen to Jensen Huang talk about AI, I do not hear the CEO of a normal chip company. I hear the CEO of a company that sits at the toll booth of the new digital economy.

That is what makes NVIDIA so fascinating.

NVIDIA is not just selling GPUs anymore. It is selling the foundation of the AI buildout: accelerated computing, networking, software ecosystems, full-stack systems and increasingly the architecture of what Huang has described in different interviews and public appearances as the future of AI factories. Recent market coverage continues to frame NVIDIA as the world’s most valuable company, largely because investors see it as the clearest winner of the AI infrastructure boom.

The phrase “AI factory” matters because it changes how we understand the business.

A traditional factory turns raw materials into physical products. An AI factory turns electricity, data and computing power into intelligence or, more practically, into tokens, predictions, automation and digital labor.

That idea is powerful.

It also explains why NVIDIA’s valuation has exploded. If AI becomes the next core layer of the economy, then NVIDIA is not merely a supplier. It becomes the company enabling the rest of the AI economy to function.

That is why NVIDIA’s rise to the top of the S&P 500 matters so much. The largest company in the index is no longer an oil giant, a bank, a consumer-products company or even a traditional software firm. It is the infrastructure provider for artificial intelligence.

That tells us what the market is really betting on. The market is not just betting that people will use AI tools.

It is betting that intelligence itself becomes a scalable industrial product.

Microsoft, Alphabet, Amazon, Apple and Meta Are Playing Different AI Games

Although people often group Big Tech together, each company is approaching AI from a different position.

Big Tech’s AI spending boom is becoming one of the most important macro stories in markets.

Microsoft, Alphabet, Amazon and Meta are rapidly increasing capital expenditures as the AI race shifts from software innovation to massive infrastructure investment, data centers and computing power.

Microsoft has one of the clearest monetization paths. It can embed AI into Office, Windows, Azure, GitHub, enterprise workflows and developer tools. Its advantage is distribution. If AI becomes a productivity layer for companies, Microsoft already has the customer relationships.

Alphabet is playing both offense and defense. On one hand, it has world-class AI research, Google Cloud, custom chips and enormous data advantages. On the other hand, AI threatens the traditional search model that made Google one of the most profitable companies in history. Alphabet must use AI to improve Search without destroying the economics of Search.

Amazon is fighting through AWS. Its AI opportunity is huge because cloud infrastructure is where many companies will train, deploy and scale AI systems. But Amazon also faces a difficult financial equation: building enough AI capacity requires enormous spending, and that can pressure free cash flow before the revenue fully arrives.

Apple is the quietest player, but it may have the most powerful distribution advantage. Apple does not need to win the model race in the same way as OpenAI, Google or Anthropic. Its opportunity is to bring AI directly into the hands of hundreds of millions of users through the iPhone, Mac, iPad, Watch and services ecosystem. Apple’s challenge is that the market has become impatient with its slower AI rollout.

Meta is slightly different because it is not always in the top-five market-cap list depending on the date, but it is impossible to ignore in the AI spending race. Meta is using AI to improve advertising, recommendation engines, content discovery, business messaging and consumer products. It is also one of the most aggressive companies in open-source AI.

This is why the AI race is so complex.

These companies are not all chasing the same prize. Microsoft wants enterprise productivity. Alphabet wants to defend and reinvent search. Amazon wants infrastructure demand. Apple wants device-level intelligence. Meta wants better engagement, advertising and eventually new AI-native social experiences.

But they all need the same thing: compute.And that brings the story back to NVIDIA.

How the AI investment boom could create financial risk

The AI race is no longer just a software story ,it is becoming a capital-intensive macroeconomic cycle.

As Big Tech companies accelerate spending on data centers, chips and infrastructure, investors are increasingly focused on whether future AI profitability will justify the massive rise in leverage, operating costs and capital expenditures.

The Hidden Cost of the AI Race: Capex, Energy and Data Centers

The most underestimated part of the AI boom is that it is physical.

People talk about AI as if it lives in the cloud. But the cloud is not magic. It is someone else’s building, someone else’s servers, someone else’s chips and someone else’s electricity bill.

AI requires data centers at a scale that is starting to resemble a new industrial revolution. That means power availability, cooling systems, grid connections, specialized chips, advanced networking, memory, storage and land are becoming strategic assets.

This is where the story gets much bigger than Silicon Valley.

If Big Tech spends hundreds of billions of dollars on AI infrastructure, the winners will not only be the companies building chatbots. The winners may also include chipmakers, optical networking companies, power-equipment suppliers, cooling specialists, construction firms and data center operators.

This also explains why Bitcoin miners have suddenly become part of the AI conversation.

Bitcoin miners already understand high-density energy usage, data center operations and power procurement. Some mining companies own infrastructure that could potentially be repurposed or adapted for AI workloads. That does not mean every Bitcoin miner becomes an AI winner, but it does mean the boundary between crypto infrastructure and AI infrastructure is becoming more interesting.

In my view, this is one of the most important secondary effects of the AI boom. The market is not only revaluing software companies. It is revaluing anything connected to compute, electricity and physical infrastructure.

That is exciting.

But again, it creates risk.

When every company suddenly wants the same GPUs, the same power contracts, the same data center capacity and the same engineers, costs rise. And when costs rise faster than revenue, even a real technological revolution can become a financial problem.

Why Higher Rates Make the AI Boom More Fragile

One of the most underestimated risks in the current AI boom is that it is unfolding in a very different monetary environment than previous technology revolutions.

For years, ultra-low interest rates and abundant liquidity allowed technology companies to expand aggressively with relatively limited concern about financing costs. Capital was cheap, borrowing conditions were favorable and investors were willing to prioritize future growth over near-term profitability.

That environment has changed significantly.

Today, companies are building the AI economy while interest rates remain much higher than during the early phases of previous tech cycles. And that matters more than many investors realize.

The AI race is becoming extremely capital intensive.

Building advanced AI systems now requires:

- Massive data centers.

- Expensive GPU infrastructure.

- Semiconductor supply chains.

- Energy-intensive computing.

- Long-term cloud investment.

- Highly specialized engineering talent.

All of this dramatically increases capital expenditures and financing needs. From a macro perspective, the problem is that higher interest rates increase the cost of funding that expansion.

When bond yields rise and financial conditions tighten:

- Debt becomes more expensive.

- Refinancing risk increases.

- Free cash flow comes under pressure.

- Margins become harder to maintain.

- And markets become less tolerant of aggressive spending cycles.

This creates an important shift in investor psychology.

During periods of near-zero rates, markets were often willing to reward growth almost regardless of profitability. But in a higher-rate environment, investors increasingly demand evidence that massive AI investments can eventually generate sustainable returns.

That is where the concept of “markets pricing perfection” becomes extremely important.

At current valuations, many AI-related companies are not simply being priced for strong growth they are being priced for near-flawless execution over many years.

The market is effectively assuming:

- Continued AI adoption.

- Strong monetization.

- Sustained productivity gains.

- Expanding profit margins.

- And long-term dominance in the AI ecosystem.

Any sign that:

- Spending is rising too quickly.

- Monetization is slower than expected.

- Margins are deteriorating.

- Or financing conditions remain restrictive.

Could lead to significant repricing across technology markets.

This is particularly relevant for companies increasing leverage to finance large-scale infrastructure expansion.

From my perspective, the key macro risk is not necessarily that AI demand disappears. The risk is that the financial system becomes less capable of supporting such an aggressive investment cycle under tighter monetary conditions.

And historically, some of the most volatile moments in technology markets occur precisely when:

- Expectations remain extremely high.

- While liquidity conditions begin tightening underneath the surface.

That tension is now becoming increasingly visible across the AI sector.

The Overleveraging Problem: When a Real Trend Becomes a Financial Risk

This is where I think we need to be careful.

A bubble does not always begin with a fake idea. Sometimes bubbles begin with a very real idea that attracts too much capital too quickly. The internet was real in 1999. Railroads were real in the 19th century. Fiber-optic networks were real before the dot-com crash. Housing was real before the 2008 financial crisis.

The problem is not always the technology. The problem is the financing structure, the assumptions and the speed of capital deployment.

AI could follow a similar pattern if companies and investors begin to assume that every dollar spent on infrastructure will automatically produce high-margin revenue. That assumption may prove correct for the strongest companies. It will probably not prove correct for everyone.

Overleveraging in AI can appear in several ways.

First, companies may build more data center capacity than the market can profitably absorb in the short term.

Second, startups may raise money at valuations that require impossible revenue growth.

Third, infrastructure providers may finance expansion based on long-term demand projections that turn out to be too optimistic.

Fourth, public-market investors may push valuations so high that even excellent companies struggle to justify them.

This is why I keep coming back to cash flow. AI headlines are exciting. Capex announcements are impressive. Jensen Huang’s vision is compelling. But eventually, the numbers have to work. The market cannot live forever on the idea that future intelligence will pay for today’s spending.

At some point, AI must produce enough measurable productivity, revenue, cost savings and customer demand to support the capital being poured into it.

How This AI Cycle Could Evolve Over the Next Few Years

I see three possible paths for the AI investment cycle.

Scenario 1: AI Becomes the Next Productivity Supercycle

This is the bullish case.

In this scenario, AI becomes deeply embedded into business operations. Companies use AI agents to automate repetitive work, improve software development, accelerate research, optimize logistics, personalize customer service and reduce costs.

If that happens, the current infrastructure buildout may look rational in hindsight.

NVIDIA remains central. Microsoft monetizes AI through enterprise software. Alphabet protects Search and grows Cloud. Amazon turns AWS into the backbone of AI deployment. Apple brings AI to everyday consumer devices. Meta improves advertising and user engagement with increasingly intelligent systems.

In this version of the future, AI spending creates enough productivity to justify the investment.

This is the outcome Jensen Huang seems to be pointing toward when he talks about a new era of computing. And honestly, I think this scenario is possible. Maybe even likely over the long term.

But “long term” is doing a lot of work in that sentence.

Scenario 2: AI Spending Normalizes After an Investment Shock

This is the more balanced scenario.

AI continues to grow, but companies realize they do not need to spend at the current pace forever. Capex slows. Investors become more selective. Some AI tools become highly profitable, while others turn out to be expensive features with limited pricing power.

In this scenario, the winners still win but the market becomes less euphoric.

NVIDIA remains important, but revenue growth normalizes. Big Tech keeps investing, but with more discipline. AI startups face more pressure to prove real business models. Data center demand remains strong, but not infinite.

This may actually be the healthiest path. The AI boom does not collapse. It matures.

Scenario 3: Overcapacity Exposes the Weakest Players

This is the bearish case.

Too much capital enters the sector. Too many companies build infrastructure based on aggressive forecasts. AI adoption grows, but not fast enough to support the spending. Margins disappoint. Financing becomes tighter. Weaker startups fail. Some data center projects become less attractive. Investors rotate away from the most expensive AI names.

In this scenario, AI is still real but the market was too early, too aggressive and too leveraged.

This is the risk I think people should take seriously. Not because AI is fake. Because AI is important enough to attract dangerous amounts of money.

My Take: I Believe in AI, But Not in Blind AI Euphoria

Personally, I am not bearish on AI.

Actually, I think AI may become one of the most important technological shifts of our lifetime. The ability to turn natural language into software, analysis, design, automation and decision support is not a small thing. It changes how people work.

But I am skeptical of the idea that every AI investment deserves a premium valuation.

That is different. I can believe in AI and still worry about overleveraging.

I can believe NVIDIA is one of the best-positioned companies in the world and still think investors should be careful about paying any price for growth.

I can believe Big Tech is right to invest aggressively and still ask whether the current spending cycle creates future financial pressure.

That is the balance I think the market needs.

The most dangerous phrase in investing is not “this technology is useless.”

It is: “This time, valuation does not matter.” It always matters. Even when the technology is revolutionary. Even when Jensen Huang is right. Even when NVIDIA becomes the most valuable company in the world. Even when every CEO says AI will transform everything.

Reality still has a balance sheet.

Conclusion: The AI Boom Is Real, But Reality Still Has a Balance Sheet

The five largest companies in the world are doubling down on artificial intelligence because they understand that AI could define the next decade of economic power.

NVIDIA is no longer just a chip company. It is the infrastructure engine of the AI economy.

Alphabet, Apple, Microsoft and Amazon are not simply adding AI features. They are defending and rebuilding their core businesses around intelligence.

Meta, although not always counted among the top five by market value, remains one of the most important AI spenders and deserves to be part of any serious discussion about the sector.

But the bigger the AI boom becomes, the more investors need to separate three things:

Technological reality.

Business profitability.

Market valuation.

AI can be real and still overpriced. AI can be transformative and still overfunded. AI can create huge winners and still destroy capital for weaker players.

That is why the next phase of the AI race will not be judged only by model performance, GPU shipments or CEO interviews. It will be judged by revenue, margins, cash flow and return on invested capital.

The companies that turn AI infrastructure into durable profits will define the next era of the market.

The companies that confuse spending with strategy may become warnings.

FAQs

Why are the world’s biggest companies investing so much in AI?

Because AI is becoming a core layer of cloud computing, productivity software, search, advertising, consumer devices and enterprise automation. The biggest companies are investing now because they do not want to depend on someone else’s AI infrastructure later.

Is the AI boom becoming a bubble?

Not necessarily, but parts of the market show bubble-like behavior. The technology is real, but the risk is that too much capital is being deployed too quickly, based on revenue expectations that may take longer to materialize.

Why is NVIDIA so important to the AI economy?

NVIDIA provides much of the accelerated computing infrastructure used to train and run advanced AI systems. Its GPUs, networking technology and software ecosystem have made it one of the central companies in the AI buildout.

What is overleveraging in AI?

Overleveraging happens when companies, startups or infrastructure providers take on too much financial risk to build AI capacity, assuming future demand will easily justify today’s spending. If demand disappoints, the financial pressure can become severe.

Which companies are leading the AI race?

NVIDIA, Microsoft, Alphabet, Amazon, Apple and Meta are among the most important public companies in the AI race. NVIDIA leads infrastructure, Microsoft leads enterprise distribution, Alphabet leads search and AI research, Amazon leads cloud infrastructure, Apple controls consumer-device distribution, and Meta is aggressively investing in AI for advertising, content and open models.

Could Bitcoin miners benefit from AI infrastructure demand?

Some Bitcoin miners may benefit if they can repurpose energy access and data center infrastructure for AI workloads. However, not all mining infrastructure is suitable for AI, and execution risk remains high.

What should investors watch in the AI cycle?

Investors should watch capital expenditure, free cash flow, revenue from AI products, data center utilization, energy costs, margins and return on invested capital. AI headlines matter, but cash flow matters more.