What Trump Actually Said About Taking Control of Cuba

When Donald Trump said the United States would “take control” of Cuba “almost immediately,” I did not read it as just another aggressive political headline. I read it as a potential macro risk signal.

According to RTVE, Trump made the statement during a private political and business dinner in West Palm Beach, Florida, adding that once the “job” in Iran was finished, he could send the USS Abraham Lincoln aircraft carrier to the Caribbean and position it close to Cuba’s coast. The same report says the Trump administration had also intensified sanctions against sectors including energy, defense, mining and financial services.

That matters because markets usually do not wait for troops to move. They move when probabilities change.

In my view, the key question is not whether the U.S. literally takes control of Cuba tomorrow. The key question is how investors, banks, commodity traders and governments start pricing the risk of escalation. A presidential statement about Cuba, military positioning in the Caribbean and expanded sanctions is not just diplomatic noise. It can become a pricing event.

For me, Cuba is not only a political story. It sits at the intersection of U.S. power projection, Caribbean shipping routes, energy dependence, sanctions risk, Latin American geopolitics and strategic minerals. That makes the situation much bigger than the headline suggests.

Why I Don’t Read This as Just Another Cuba Story

Cuba has always carried symbolic weight in U.S. foreign policy. But in markets, symbolism only becomes important when it creates uncertainty around supply chains, sanctions, capital flows or military risk.

This is why my first instinct is to look at five things: oil, shipping, sanctions, regional risk and strategic commodities.

If Washington increases pressure on Havana, the first impact may not come through an invasion scenario. It may come through financial restrictions, insurance costs, banking compliance, energy disruption and diplomatic retaliation. That is how geopolitical risk usually enters the market: gradually at first, then suddenly if a threshold is crossed.

The recent sanctions context is important. Reuters reported that Trump signed an executive order expanding sanctions on Cuba, targeting people and entities connected to Cuba’s security apparatus, corruption or human rights abuses, while also affecting key sectors such as energy, defense, metals and mining, finance and security. The order also included secondary sanctions risk for those facilitating transactions with sanctioned parties.

That is the part I would watch most closely as a macro observer. Sanctions can create market impact before any military action happens. They can make banks pull back, insurers reprice risk, commodity flows become more complicated and foreign companies reconsider exposure.

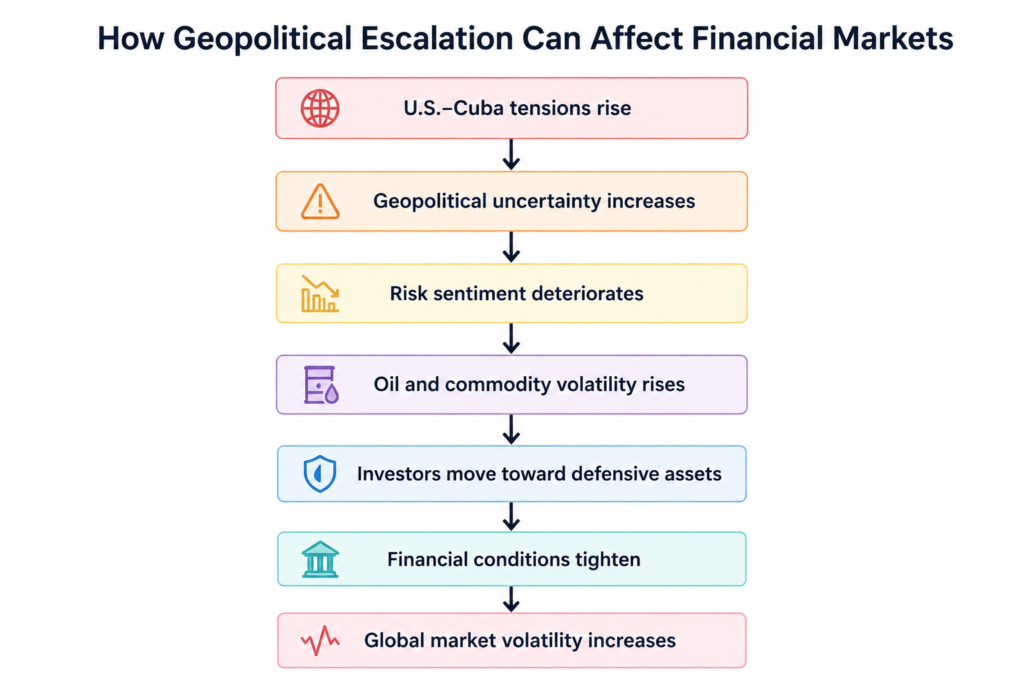

How Geopolitical Escalation Can Affect Financial Markets

Geopolitical shocks rarely affect markets in a linear way.

Even before any real military escalation occurs, uncertainty alone can tighten financial conditions, increase volatility and shift investor behavior across global markets.

What a Possible U.S. Takeover of Cuba Would Mean for Markets

A possible U.S. takeover of Cuba would be interpreted by markets as a geopolitical shock in the Caribbean. The severity would depend on the path: rhetoric, sanctions escalation, naval pressure, regime-change attempt or direct military intervention.

Markets do not price all of those scenarios equally.

If this remains political rhetoric, the impact could be limited and short-lived. Oil may barely move, the dollar may not react much and emerging market investors may treat it as headline risk. But if the situation moves toward naval pressure, energy restrictions or a broader confrontation involving Cuba’s allies, the risk premium would rise.

The first assets I would watch are:

| Asset / Market | Possible Reaction |

|---|---|

| Oil | Higher geopolitical risk premium if Caribbean energy flows or Cuban supply lines are disrupted |

| Gold | Potential safe-haven bid if military language escalates |

| U.S. dollar | Stronger if investors move toward safety |

| Emerging market debt | Pressure on Latin American and frontier risk assets |

| Defense stocks | Potential upside from higher perceived geopolitical tension |

| Caribbean tourism | Negative impact from travel disruption and regional instability |

| Shipping and insurance | Higher costs if the Caribbean becomes a risk zone |

I would not assume a massive global shock immediately. Cuba is not a major global oil producer. But markets are not only about direct supply. They are about second-order effects: who responds, which routes are affected, what sanctions are enforced, which banks get nervous and whether the Caribbean starts to look like a military theater.

That is where the macro story begins.

Commodities: Oil, Sugar, Nickel and the Caribbean Shock Factor

Oil: The First Market I Would Watch

Oil is the most obvious commodity to monitor, not because Cuba itself dominates global production, but because the island is highly exposed to fuel supply disruptions.

Reuters recently described Cuba as heavily dependent on petroleum compared with regional peers and reported that Russian oil provided only short-term relief to the island’s energy problems. Another Reuters report said a Russian oil shipment met only about one-eighth of Cuba’s monthly demand and would provide limited relief through the end of April.

That tells me something important: Cuba’s energy system is already fragile. If U.S. pressure increases, oil becomes the transmission mechanism.

I would watch for three signals:

- Tanker movements toward Cuba.

- Restrictions on countries or companies supplying fuel.

- Blackouts, refinery disruptions or rationing.

If those worsen, the story becomes less about political speeches and more about energy stress. That could affect regional sentiment, humanitarian conditions and diplomatic calculations.

Sugar: Symbolic, Not Systemic

Sugar is historically tied to Cuba, but today I would treat it more as a symbolic and regional commodity story than a global supply shock. A Cuba crisis could create headlines around agricultural disruption, but it would probably not transform global sugar pricing by itself unless broader regional logistics or weather-related supply issues were already pressuring the market.

Still, sugar matters narratively. It reminds investors that Cuba’s economy is not just about ideology. It is about food, fuel, labor, exports and hard currency.

Nickel and Mining: The Strategic Angle Few People Discuss

The mining angle is more interesting than most people realize.

RTVE reported that the sanctions targeted sectors including mining, and Reuters also noted that the expanded sanctions affected metals and mining.

Cuba has relevance in nickel and cobalt-linked supply chains, even if it is not the dominant global producer. USGS data on Cuba’s mineral industry showed production declines in 2023, including estimated decreases in crude petroleum, cobalt and nickel-cobalt sulfide.

For me, this is not about Cuba suddenly controlling the global battery supply chain. It is about strategic optionality. In a world already sensitive to critical minerals, sanctions or control over mining assets can matter more than headline production numbers suggest.

If the U.S. were ever to push for direct influence over Cuba’s economy, mining would be one of the sectors to watch.

Sanctions, Banks and the Financial Transmission Channel

The biggest near-term market impact may come from finance, not commodities.

RTVE reported that the White House warned foreign banks that facilitating significant transactions for sanctioned Cuban parties could lead to restrictions on Wall Street accounts or dollar operations.

That is a serious macro channel.

When banks hear “secondary sanctions,” they often reduce exposure before regulators force them to. This can create a chilling effect. Even legal transactions become harder because compliance departments do not want to touch anything remotely connected to sanctioned entities.

That means a Cuba escalation could affect:

- Foreign banks with Caribbean or Latin American operations.

- Shipping companies moving energy or food.

- Mining and infrastructure firms.

- Tourism operators.

- Remittance channels.

- Companies exposed to Cuban state-linked entities.

This is why I would not only watch oil prices. I would watch banking behavior. If banks start exiting relationships, delaying payments or tightening compliance, the economic pressure on Cuba increases without a single shot being fired.

Scenario Analysis: How I Would Interpret the Next Moves

Scenario 1: Political Rhetoric With Limited Market Impact

This is the lowest-impact scenario. Trump’s statement remains a political message aimed at domestic voters, Cuban exiles, regional allies and adversaries.

In this case, markets may barely react. Oil stays focused on broader supply-demand fundamentals. Gold and the dollar may not move meaningfully. Investors treat the story as noise unless new military or sanctions action follows.

My interpretation: this would be loud politically but modest economically.

Scenario 2: Sanctions Escalation and Commodity Pressure

This is more market-relevant.

If sanctions expand further, especially against energy, mining, finance or shipping, the impact becomes tangible. Cuba’s fuel crisis could deepen, foreign companies could pull back and banks could become more cautious.

This scenario would probably not create a global oil crisis by itself, but it could add a regional risk premium and worsen Cuba’s economic conditions.

My interpretation: this is the scenario markets should take seriously first.

Scenario 3: Naval Pressure in the Caribbean

If U.S. naval assets move closer to Cuba, the market interpretation changes.

A military presence does not automatically mean war, but it changes the risk map. Shipping insurers may pay attention. Oil traders may price uncertainty. Regional governments may issue statements. Gold and the dollar could catch a bid if the situation coincides with other geopolitical stress.

My interpretation: this is where headlines become tradable.

Scenario 4: Regime Change Attempt or Direct Intervention

This would be the highest-impact scenario.

A direct intervention or forced regime-change attempt could trigger regional backlash, diplomatic conflict, humanitarian disruption and possible responses from countries aligned with Cuba. The market would not only look at Cuba. It would look at Russia, China, Venezuela, Mexico, Brazil and the broader Latin American response.

My interpretation: this is a low-probability but high-impact tail risk.

Winners and Losers in a Cuba Escalation

From a market perspective, geopolitical shocks rarely hurt everyone equally. They redistribute risk.

Potential winners could include defense companies, safe-haven assets, some energy names and parts of the security infrastructure sector. If the crisis creates a broader perception of instability, gold and the U.S. dollar could benefit from defensive flows.

Potential losers could include Caribbean tourism, airlines with regional exposure, companies operating in or near Cuba, foreign banks with compliance exposure, and riskier Latin American assets.

Tourism is especially vulnerable. The Guardian recently reported that escalating sanctions and an oil blockade have severely affected Cuban tourism, with fuel shortages, grounded airlines and collapsing visitor numbers adding pressure to the island’s economy.

That is one of the clearest real-economy links. If people cannot fly easily, hotels lose revenue. If hotels lose revenue, workers lose income. If fuel is scarce, transport slows. If transport slows, agriculture and tourism both suffer.

This is how macro risk becomes human reality.

What I Would Watch Next as a Macro Signal

If I were tracking this as a market event, I would focus less on speeches and more on confirmation signals.

The first signal would be military movement. If aircraft carriers, surveillance flights or naval assets become a recurring feature around Cuba, risk perception changes.

The second signal would be oil flow. Cuba’s energy stress is already severe. AP reported that a U.S.-imposed energy blockade has worsened fuel, water and power shortages, hitting agriculture and food production. AP also reported that Cuba has faced systemic blackouts and fuel shortages, with a Russian tanker delivery offering only partial relief.

The third signal would be banking behavior. If foreign banks reduce Cuban exposure, that would suggest sanctions are biting.

The fourth signal would be regional diplomacy. Statements from Mexico, Brazil, Venezuela, Russia, China and the European Union would help determine whether this remains a bilateral U.S.-Cuba confrontation or becomes a wider geopolitical issue.

The fifth signal would be market reaction itself: oil, gold, the dollar, emerging market spreads and defense stocks.

Markets often tell us when a political story is becoming an economic story.

My Bottom Line: This Is a Probability Event, Not a Certainty

I would not treat Trump’s statement as a guarantee that the United States will take control of Cuba. That would be too simplistic.

But I also would not dismiss it as pure theater.

For me, this is a probability event. The market does not need certainty to react. It only needs a higher probability of disruption.

A possible U.S. takeover of Cuba would matter because it could reshape risk perception in the Caribbean, intensify sanctions, disrupt energy flows, pressure banks, affect tourism and raise questions about strategic minerals. The most important market impact may not come from the dramatic scenario of direct military control. It may come from the steps before that: sanctions, shipping pressure, financial restrictions and energy stress.

That is how I interpret the headline. Not as a prediction. Not as panic. But as a macro signal worth watching carefully.

From my perspective, the real market risk is not Cuba itself, but what the situation represents: a world where geopolitics is once again becoming one of the dominant forces shaping inflation, liquidity and global financial markets.

FAQs

Did Trump really say the U.S. would take control of Cuba?

According to RTVE, Trump said the United States would “take control” of Cuba “almost immediately” and linked the idea to future U.S. military positioning in the Caribbean after Iran.

Is a U.S. takeover of Cuba realistic?

It is better to think in scenarios. A literal takeover would be an extreme and high-impact event. A more immediate risk is sanctions escalation, naval pressure, banking restrictions and energy disruption.

Could this affect oil prices?

Yes, but probably through risk premium rather than direct Cuban oil supply. Cuba is not a major global oil producer, but its energy dependence, fuel shortages and regional position make oil the first commodity I would watch.

Which commodities are most exposed to Cuba?

Oil is the most immediate. Nickel, cobalt-linked mining and sugar are also relevant, although in different ways. Oil matters for energy stress, nickel and cobalt matter for strategic-resource discussions, and sugar matters more as an agricultural and historical exposure.

How could sanctions affect global banks?

Secondary sanctions risk can make foreign banks reduce or avoid transactions connected to Cuba. Even when trade is legal, compliance risk can discourage banks from processing payments.

What should investors watch first?

I would watch military movement in the Caribbean, oil shipments, banking restrictions, statements from Cuba’s allies, gold, oil, the U.S. dollar and Latin American risk assets.