Iran’s proposed three-phase plan is not just another diplomatic document. At least, that is not how I read it. When I look at this proposal, I see something much bigger than a ceasefire formula or a negotiating tactic. I see a possible turning point for oil prices, shipping routes, sanctions, inflation, regional investment and the economic confidence that markets have been losing since the war began.

According to reports, Iran has put forward a plan that prioritizes a definitive end to the war, a new mechanism for the Strait of Hormuz, and a later discussion of the nuclear file. Swissinfo, citing EFE, describes the proposal as a 14-point plan focused on ending the conflict permanently, lifting the naval blockade, obtaining non-aggression guarantees, withdrawing U.S. forces from the region, easing sanctions and releasing frozen assets. El País also reports that Iran’s plan is structured in three stages and leaves the nuclear issue for the final phase of negotiations.

That order matters. In normal diplomatic language, it may sound technical. But economically, it is huge. Iran is basically saying: first stop the war, then stabilize the Strait of Hormuz, and only after that talk about the nuclear issue. For me, the most important question is not only whether Washington accepts this sequence. The real question is whether markets believe it.

Because if markets believe the war is ending, oil prices could calm down. Shipping risk could fall. Inflation expectations could soften. Investors could start pricing in a less chaotic Middle East. But if the war continues, the economic bill will not stay inside Iran, Israel or the Gulf. It will keep spreading through fuel prices, insurance premiums, trade routes, sanctions, currencies and consumer prices.

Iran’s Three-Phase Plan, Explained Simply

Phase One: Ending the War and Securing Guarantees

The first phase of Iran’s proposal focuses on ending the war, not merely extending a fragile ceasefire. Swissinfo reports that Tehran rejected the idea of simply prolonging the current truce and instead proposed resolving war-related issues within 30 days.

This is the part that matters politically, but also economically. A ceasefire reduces immediate violence. A formal end to the war reduces uncertainty. And uncertainty is one of the most expensive things in global markets.

When companies do not know whether a shipping lane will be open next week, they pay more for insurance. When oil traders do not know whether supply routes will be disrupted, they price in risk. When governments do not know whether the conflict will expand, they hold back on investment plans. That is why “ending the war” is not just a diplomatic phrase. It is an economic signal.

Iran is also demanding guarantees that the United States and Israel will not launch new military action against Iranian territory. From an economic point of view, that demand is central. If those guarantees are credible, the risk premium attached to oil, regional assets and shipping could fall. If they are vague or impossible to verify, markets may treat the plan as temporary theater rather than a serious peace framework.

Phase Two: The Strait of Hormuz and Global Oil Flows

The second phase is where the economic story becomes impossible to ignore. The Strait of Hormuz is one of the most important energy chokepoints in the world. Swissinfo reports that around 20% of global crude oil passes through this route, and that restrictions during the war helped push oil above $110 per barrel.

This is where geopolitics stops being abstract and starts showing up in daily life. A problem in Hormuz can become a problem at the gas pump. It can become a problem for airlines, supermarkets, factories and central banks. Higher oil prices raise transport costs. Higher transport costs feed into consumer prices. Consumer prices affect inflation. Inflation affects interest rates. And interest rates affect mortgages, loans, business expansion and household spending.

El País reports that the second phase of the plan would focus on how to manage the Strait of Hormuz, with Oman playing a relevant role because it is the other coastal state bordering the passage. That detail matters. If the plan creates a predictable legal or security framework for ships, markets may calm down. But if the result is a toll system, political control over passage, or selective access for certain countries, companies may still treat the route as risky.

For me, this is probably the economic heart of the whole plan. The nuclear issue gets the headlines, but Hormuz is where the world economy feels the conflict almost immediately.

Phase Three: The Nuclear Issue Comes Last

The third phase leaves the nuclear file for the end. El País reports that Iran wants to delay nuclear negotiations until after agreement is reached on ending the war and managing Hormuz. It also notes that Washington’s demands reportedly include limits on Iran’s uranium enrichment and highly enriched uranium stockpile.

This sequencing is controversial because the nuclear issue is one of the main reasons the conflict escalated in the first place. But Iran’s logic seems clear: it does not want to negotiate its strategic program while bombs, sanctions, blockades and military pressure remain active.

Economically, postponing the nuclear issue creates both opportunity and risk. The opportunity is that the parties could first lower the temperature, stabilize energy routes and reduce immediate war costs. The risk is that if the nuclear question remains unresolved, investors may treat any peace deal as incomplete.

That is why a three-phase plan could help markets in the short term but still leave long-term uncertainty. Peace would not solve everything overnight. But continued war would almost certainly keep exporting instability.

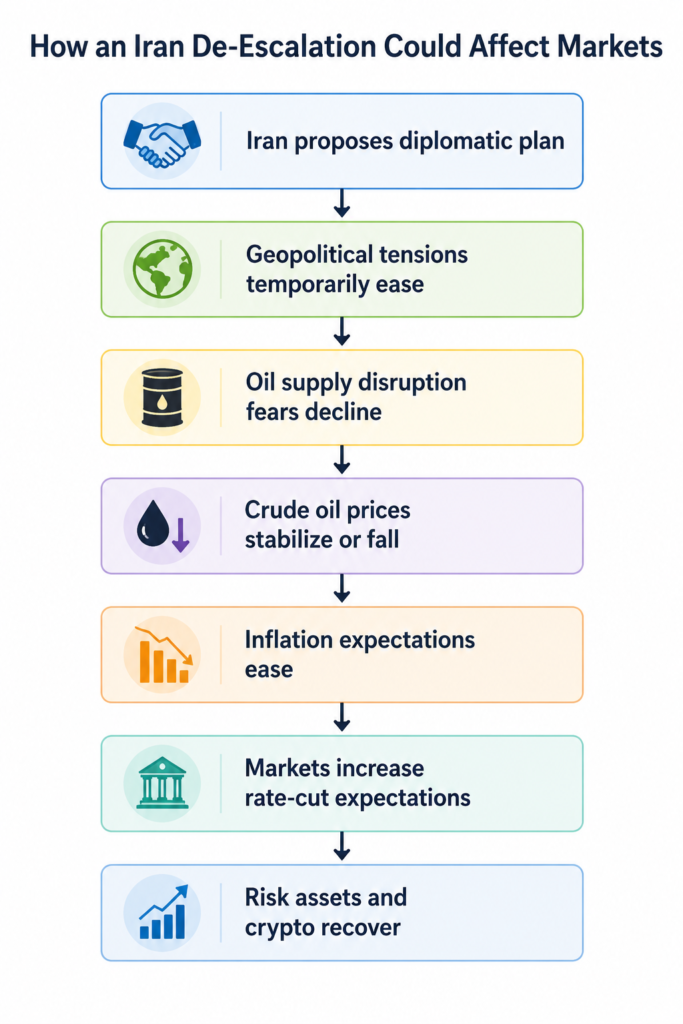

How an Iran De-Escalation Could Affect Markets

If diplomatic progress reduces the probability of a wider conflict, oil risk premiums could fall, inflation expectations may ease and markets could begin pricing a more flexible Federal Reserve.

Why the Economic Stakes Are Bigger Than the Diplomatic Headlines

Oil Prices Are the First Market to Watch

Oil is usually the first place where Middle East conflict appears in global markets. In this case, the connection is direct. The war has already affected the Strait of Hormuz, naval activity and tanker movement. Swissinfo reports that the U.S. imposed a naval blockade on Iranian ports and ships, and that 45 Iranian vessels were intercepted while trying to bypass the maritime restrictions.

If the war ends, oil prices could fall or at least become less volatile. Traders would no longer need to price in the same level of disruption risk. Tankers could move with more confidence. Energy importers in Asia and Europe could face fewer emergency costs.

But if the war continues, the opposite could happen. Oil may not simply rise in a straight line, but volatility could remain high. And volatility itself has a price. Airlines hedge fuel. Shipping firms pay higher insurance. Governments prepare emergency reserves. Consumers eventually feel the pressure through fuel, electricity and imported goods.

My view is simple: the economic impact of this plan should be judged first by what happens to oil risk. Not just oil supply, but oil risk.

Shipping Costs Could Fall or Spike Again

The Strait of Hormuz is not only about crude oil. It is also about trust in maritime trade. When shipping companies believe a route is dangerous, they do not wait for disaster. They adjust immediately. They reroute, delay, insure, surcharge or withdraw.

A peace deal that includes a credible Hormuz mechanism could reduce costs for maritime trade. Insurance premiums may ease. Delivery schedules could become more predictable. Energy exporters and importers could return to normal planning.

However, a failed plan could make things worse. If Iran, the United States and regional actors cannot agree on who controls access, who pays transit fees, and what counts as a hostile vessel, the Strait could remain a pressure point. El País reports that Iran’s proposal includes discussions around a new system for the Strait of Hormuz and possible transit fees or tolls.

That would create a new layer of economic uncertainty. Even if open conflict slows, a politically managed chokepoint could still make global trade more expensive.

Inflation Could Ease If Energy Markets Calm Down

Inflation is not only about money supply or central banks. It is also about energy shocks. When oil prices jump, everything that moves becomes more expensive: trucks, ships, planes, tractors, delivery vans, factories and power plants.

That is why the end of the war could help inflation expectations. If energy markets calm down, businesses may stop raising prices preemptively. Central banks may face less pressure to keep rates high. Consumers may regain some confidence.

But if the war continues, inflation pressure could spread. Fuel costs would be the first hit. Food prices could follow, because agriculture depends on fuel, fertilizers and transport. Imported goods could become more expensive if shipping costs rise. And countries already struggling with weak currencies could suffer even more because energy is often priced in dollars.

This is the part I think people sometimes underestimate. A regional war can become a global household problem very quickly.

What Could Happen Economically If the War Ends

Relief for Oil Markets

The most immediate economic effect of a credible peace deal would probably be relief in oil markets. Not necessarily a dramatic collapse in prices, but a reduction in fear.

Oil prices are not only based on today’s supply. They are based on what traders think might happen tomorrow. If tankers can move more safely through Hormuz, if the naval blockade is lifted, and if the risk of attacks falls, the market may remove part of the war premium.

That could benefit oil-importing countries, transport companies, airlines, manufacturers and consumers. It could also help governments that have been forced to absorb higher fuel costs through subsidies or emergency measures.

Still, there is a catch. If the peace deal includes new tolls or political conditions for Hormuz transit, the relief may be limited. Markets want stability, not just a new kind of uncertainty.

A Possible Opening for Sanctions Relief

Another major issue is sanctions. Swissinfo reports that Iran’s proposal includes the lifting of economic sanctions and the release of frozen assets, including $6 billion previously unlocked in a prisoner exchange and later frozen again in Qatar.

If sanctions relief becomes part of a broader settlement, Iran’s economy could breathe. More access to foreign currency, oil revenues, imports and financial channels would reduce pressure on businesses and households. It could also make Iran more attractive for limited forms of trade and investment.

But sanctions relief would likely be gradual and conditional. The United States would not lift major measures without guarantees. Iran would not accept relief that can be reversed instantly without gaining something strategic in return.

This is why I see sanctions as both an economic prize and a political trap. If handled carefully, they can support peace. If handled badly, they can become another reason for the plan to collapse.

More Confidence for Regional Investment

A real end to the war would also help regional investment. Gulf economies, energy companies, logistics firms and infrastructure investors all watch conflict risk closely. Nobody wants to put billions of dollars into a region where shipping lanes, military bases or oil facilities may become targets.

Peace would not erase geopolitical risk, but it could reduce the premium investors demand. Projects delayed by uncertainty might restart. Regional currencies could stabilize. Banks could become more willing to finance trade.

The wider Middle East has spent years trying to attract capital into energy diversification, ports, logistics, tourism, technology and infrastructure. A prolonged Iran-centered war works against all of that. A credible peace framework would support it.

A Lower Risk Premium Across Global Markets

Markets hate surprises. A peace deal would reduce one of the world’s biggest active geopolitical risks. That could support stocks, lower energy volatility, reduce safe-haven pressure and improve global sentiment.

The effect would probably be uneven. Energy importers may benefit more than energy exporters. Airlines and shipping firms may benefit from lower costs. Defense stocks might lose some conflict premium. Emerging markets vulnerable to oil shocks could gain breathing room.

But the key point is this: peace has an economic value even before the first sanction is lifted or the first reconstruction contract is signed. The value comes from reducing uncertainty.

What Could Happen If the War Continues

Higher Energy Prices and More Inflation Pressure

If the war continues, the most obvious economic risk is higher energy prices. Even without a full closure of Hormuz, the fear of disruption can keep prices elevated. Swissinfo reports that restrictions around Hormuz had already helped push oil above $110 per barrel during the conflict.

That kind of price pressure does not stay isolated. It moves through the economy. Fuel becomes more expensive. Electricity may rise. Transport companies raise rates. Imported goods cost more. Governments face pressure to subsidize consumers. Central banks worry about inflation expectations.

In other words, continued war could act like a tax on the global economy.

More Disruption Around the Strait of Hormuz

If negotiations fail, the Strait of Hormuz could remain the main pressure point. Iran may keep using its geographic position as leverage. The United States may maintain or intensify naval pressure. Regional states may become more involved.

That is dangerous because Hormuz is not a symbolic route. It is a real artery of global energy trade. Even partial disruption can have global consequences.

For me, this is the clearest reason why the economic discussion matters. The war is not just being fought with missiles, sanctions and speeches. It is also being fought through logistics.

Deeper Damage to Iran’s Economy

Iran’s economy would also keep suffering. War damages infrastructure, reduces investor confidence, increases military spending, weakens currency stability and makes everyday business harder. Swissinfo reports that Iran is seeking war reparations for damage suffered during 39 days of Israeli and U.S. bombing, including destroyed homes, hospitals, schools and industrial facilities, according to Iranian figures.

Whether one accepts every figure or not, the economic logic is clear. Bombed infrastructure must be rebuilt. Lost workers cannot be replaced easily. Hospitals, schools and factories are not just buildings; they are part of a country’s productive capacity.

The longer the war continues, the more expensive peace becomes later.

Wider Risks for the Middle East and Global Trade

The conflict also has regional spillover risks. Swissinfo reports that Iran wants the end of hostilities to include all related fronts, including Lebanon, where Hezbollah has been involved in fighting with Israel.

That matters economically because regional wars rarely respect borders. Insurance markets respond to regional risk. Investors respond to regional risk. Shipping companies respond to regional risk. Even countries not directly involved can pay the price through lower tourism, higher borrowing costs or reduced trade flows.

A continued war could also force governments to spend more on defense and less on development. That is another hidden cost: money that could go to infrastructure, health, education or energy transition gets redirected toward security.

The Effects the War Has Already Had

Oil Has Already Reacted

The war has already affected oil markets. The clearest evidence is the reported rise in oil prices above $110 per barrel after restrictions around Hormuz. That is not a theoretical consequence. It has already happened.

This matters because oil is a benchmark for broader economic anxiety. When oil jumps, markets immediately begin asking: Will inflation return? Will central banks delay rate cuts? Will consumers spend less? Will businesses protect margins by raising prices?

That is why Iran’s proposal is being read not only by diplomats, but also by traders, energy analysts and investors.

Maritime Trade Has Become More Expensive and Risky

The naval blockade and interceptions of Iranian vessels have already changed the maritime environment. Swissinfo reports that the U.S. blockade began on April 13 and that 45 Iranian vessels had been intercepted.

Even when ships are not directly attacked, the presence of military restrictions changes commercial behavior. Insurance rises. Delays increase. Companies become more cautious. Some cargoes may be postponed or rerouted.

This is one of the quietest but most important effects of war: trade does not need to stop completely to become more expensive.

Sanctions, Frozen Assets and Reparations Are Now Central Issues

The war has also pushed sanctions, frozen assets and reparations into the center of negotiations. Iran is not only asking for a ceasefire. It wants economic relief, access to frozen money and compensation for damages.

That tells us something important. Tehran sees the war as an economic conflict as much as a military one. The United States uses sanctions and blockades. Iran uses Hormuz, regional influence and negotiation sequencing. Both sides understand that money, oil and trade are part of the battlefield.

The Human Cost Is Also an Economic Cost

It is easy to talk about oil, sanctions and shipping and forget the human side. But the human cost is also an economic cost. Deaths, displacement, destroyed hospitals, damaged schools and lost jobs all weaken a society’s future.

El País opened its report with a symbolic reference to Minab, where it says 168 minors, mostly girls, died in a U.S. bombing of a school on the first day of the war, according to the Iranian narrative described in the article. That kind of detail matters because wars do not only destroy present income. They destroy future capacity.

A school destroyed today is not just a tragedy today. It is lost education, lost productivity and lost social stability tomorrow.

Peace vs Continued War: Economic Impact Comparison

| Scenario | Likely economic effect | Who feels it first |

|---|---|---|

| War ends credibly | Lower oil risk premium | Energy markets, airlines, importers |

| Hormuz stabilizes | Lower shipping and insurance risk | Shipping firms, exporters, consumers |

| Sanctions relief begins | More liquidity for Iran | Iranian businesses and households |

| Nuclear issue remains unresolved | Long-term uncertainty stays | Investors and governments |

| War continues | Higher energy volatility | Oil importers and consumers |

| Hormuz remains unstable | Costlier maritime trade | Tanker operators and insurers |

| Sanctions intensify | More pressure on Iran’s economy | Iranian currency, banks, imports |

| Regional conflict spreads | Broader investment slowdown | Middle East economies and global markets |

My Take: This Plan Is Really an Economic Test

Peace Would Not Solve Everything Overnight

I do not think Iran’s three-phase plan should be treated as a magic solution. Even if accepted, it would leave many difficult questions open. Who verifies non-aggression guarantees? What exactly happens in Hormuz? How fast would sanctions relief come? What does Washington accept on the nuclear issue? What role do Oman, Pakistan and Russia play?

These are not small details. They decide whether the plan becomes a real economic turning point or just another temporary pause.

But I also think it would be a mistake to dismiss the proposal only because it is complicated. Peace agreements are always complicated. The point is whether they reduce the cost of uncertainty.

Continued War Would Keep Exporting Instability

If the war continues, the economic damage will keep spreading. Iran will suffer directly. Israel and U.S. regional positions will remain exposed. Gulf economies will face more risk. Oil importers will pay more. Consumers may face higher prices. Investors will demand more compensation for uncertainty.

That is why I see this plan less as a diplomatic document and more as an economic test.

If it calms Hormuz, reduces oil volatility, opens a path to sanctions relief and lowers the chance of renewed attacks, it could matter a lot. If it fails, the war will continue doing what wars always do: destroying locally and inflating costs globally.

Conclusion: The Real Question Is Whether Markets Believe the Plan

Iran’s three-phase proposal is built around a clear sequence: end the war first, manage the Strait of Hormuz second, and discuss the nuclear issue last. Diplomatically, that sequence is controversial. Economically, it is logical. Iran wants security and commercial breathing room before entering the hardest negotiation.

The economic impact of ending the war could be significant: lower oil volatility, cheaper shipping, softer inflation pressure, possible sanctions relief and more regional investment confidence. But if the war continues, the opposite risks remain: higher energy prices, disrupted trade, deeper damage to Iran’s economy, more regional instability and a larger global inflation shock.

What interests me most is not only whether the plan sounds realistic on paper. It is whether it can change expectations. Because markets move on expectations before they move on facts.

If investors, shipping firms and oil traders believe the war is ending, the economic relief could begin quickly. If they believe the plan is just a pause before the next escalation, the risk premium will stay.

That is the real test of Iran’s three-phase plan: not only whether diplomats sign it, but whether the world economy believes it.

From my perspective, the most important shift is not whether a final agreement is immediately reached, but whether markets begin believing that the probability of a larger regional conflict is starting to decline.

FAQs About Iran’s Three-Phase Plan

What is Iran’s three-phase plan?

Iran’s three-phase plan is a proposal to end the war by first securing a definitive cessation of hostilities, then negotiating a new mechanism for the Strait of Hormuz, and finally addressing the nuclear issue. El País reports that Iran wants the nuclear file left for the last stage of negotiations.

Why is the Strait of Hormuz so important?

The Strait of Hormuz is a crucial maritime route for global energy trade. Swissinfo reports that around 20% of global crude oil passes through the strait. Any disruption there can affect oil prices, shipping costs, inflation and global trade.

How could the plan affect oil prices?

If the plan reduces the risk of conflict around Hormuz, oil prices could calm down or become less volatile. If negotiations fail and the strait remains unstable, oil prices could stay high or spike again.

What happens economically if the war continues?

A continued war could keep energy prices elevated, increase shipping and insurance costs, worsen inflation pressure, damage Iran’s economy further and discourage investment across the region.

Why is the nuclear issue left for last?

Iran appears to want security guarantees and a settlement over the war and Hormuz before negotiating the nuclear file. This sequencing gives Tehran leverage, but it also makes acceptance harder because Washington sees the nuclear issue as central to the conflict.