Markets are sending one message. The real economy is sending another.

That is the uncomfortable idea behind the recent “market disconnect” theory the view that financial markets, especially equities, are behaving far more optimistically than the underlying economy seems to justify. Stocks can rally, volatility can stay contained, and investors can talk about soft landings, AI productivity and future rate cuts. Meanwhile, households face tighter budgets, companies deal with higher costs, credit becomes less forgiving, and recession risk refuses to disappear.

What makes this moment interesting is not simply that markets and the economy are moving at different speeds. That happens often. What matters now is that the gap appears to be widening at a time when several asset classes are telling different stories.

Equities still want to believe in growth. Bonds are more sensitive to slowdown risk. Gold is quietly reminding investors that uncertainty has not gone away. Oil and commodities are caught between geopolitics, supply shocks and weaker demand expectations.

In my view, the key question is no longer whether the disconnect exists. The real question is this: what happens if the gap suddenly closes?

Why the disconnect matters now

The idea that “the stock market is not the economy” is not new. But lately, it has become much harder to dismiss.

A recent interview in Cinco Días with Silvia García-Castaño, chief investment officer for Spain at Lombard Odier, captured the issue clearly: financial markets have been holding up reasonably well, while companies are already seeing higher costs and weaker consumption. That is the essence of the disconnect asset prices remain resilient, but the real economy feels more fragile.

The same concern appears in recession-focused commentary around Mark Zandi of Moody’s, where the market’s strength is contrasted with weaker consumer signals, labor and housing vulnerabilities, and a recession probability that remains elevated.

That contrast is what makes this story important. A strong stock market can create the impression that the economy is fine. But headline indices can be misleading, especially when gains are concentrated in a narrow group of companies.

The AI effect: when a few stocks carry the market

One of the biggest reasons markets can look healthier than the economy is concentration.

AI enthusiasm has become one of the dominant forces behind equity market optimism. Large technology companies tied to artificial intelligence, semiconductors, cloud infrastructure and data centers can lift entire indices, even if the average business is facing a much tougher environment.

This does not mean the AI story is fake. It means the market may be pricing a very specific future: one where a handful of companies generate enough growth to offset broader economic weakness.

That is possible. But it is also risky.

When market leadership becomes narrow, the index stops being a clean reflection of the economy. The S&P 500 can rise while small businesses struggle. Mega-cap tech can attract capital while cyclical sectors weaken. Investors can celebrate earnings from a few dominant names while the broader consumer quietly slows down.

This is where I think the disconnect becomes dangerous. It encourages investors to confuse index strength with economic strength.

Why markets can ignore recession risk until they cannot

Markets are not built to price the present. They price expectations.

If investors believe central banks will cut rates, inflation will ease, and policy makers will step in if conditions deteriorate, risk assets can stay supported for longer than fundamentals suggest. Liquidity, expected rate cuts and the hope of policy support can all keep markets elevated.

That is why recessions rarely arrive with perfect warning signs in equity prices. Often, the market keeps believing in the soft-landing story until the data becomes too weak to ignore.

The problem is that once the narrative changes, repricing can be abrupt. If investors move from “growth is resilient” to “earnings are too high and recession risk is real,” equities can adjust quickly.

That is what would close the disconnect: not a slow academic realization, but a sudden shift in expectations.

What a recession scare could mean for stocks

If recession risk rises, equities would likely be the first asset class most people notice.

The most vulnerable areas would probably be the parts of the market priced for perfection: high-multiple growth stocks, speculative AI names, unprofitable companies, and cyclical sectors dependent on strong consumer demand. If earnings expectations fall, these areas could face the sharpest adjustment.

But the impact would not be uniform. Defensive sectors such as healthcare, quality consumer staples and some cash-rich companies could hold up better. Select technology may also remain attractive, especially firms with real earnings power rather than just narrative momentum.

That distinction matters. A recession scare does not mean “sell everything.” It means markets start separating durable cash flows from optimistic stories.

In the Lombard Odier interview, García-Castaño mentioned increased exposure to gold, selective technology, pharmaceuticals and electrification-related companies. That kind of positioning says a lot about the current environment: investors are not necessarily abandoning risk, but they are becoming more selective.

Bonds may tell the truth before equities do

If equities are the optimistic asset class, bonds are often where stress appears earlier.

Government bonds can perform well when recession fears rise, especially if investors expect weaker growth and lower interest rates. In that environment, Treasury yields may fall as capital moves toward safety.

Credit is different. High-yield bonds are especially important because they sit closer to the real economy. When companies with weaker balance sheets face higher refinancing costs, slower demand and tighter lending conditions, credit spreads tend to widen. That can happen before equity investors fully accept the risk.

This is why I would watch high-yield spreads closely. If equities remain strong while high-yield credit weakens, the disconnect is not closing it is becoming more visible.

Vulcano Global’s market commentary made a similar point, highlighting divergence between high-yield bonds, Treasuries and the S&P 500 as a warning sign that can precede equity corrections.

For me, that is one of the clearest signals. Equity indices can be distorted by a few giant companies. Credit markets are often harder to fool.

Commodities: gold, oil and the recession puzzle

Commodities complicate the picture because they do not all behave the same way.

Gold is the cleanest part of the story. If uncertainty rises, real yields fall, debt concerns increase, or investors lose confidence in the soft-landing narrative, gold can benefit. It is not just an inflation hedge. In this environment, it is also a hedge against policy mistakes and financial instability.

Oil is more complicated. If recession risk becomes the dominant story, oil usually faces pressure because weaker growth means weaker demand. But geopolitics can override that, at least temporarily. Supply disruptions, conflict risk or energy shocks can keep prices elevated even as the economy slows.

That creates a difficult scenario: oil can act like a tax on consumers if prices spike, but it can also fall sharply if recession fears overwhelm supply concerns.

Industrial commodities are more directly tied to global growth. If the real economy weakens, demand for copper, steel, energy inputs and other cyclical materials can soften. That is why commodities should not be treated as one single trade. Gold, oil and industrial metals can send very different signals.

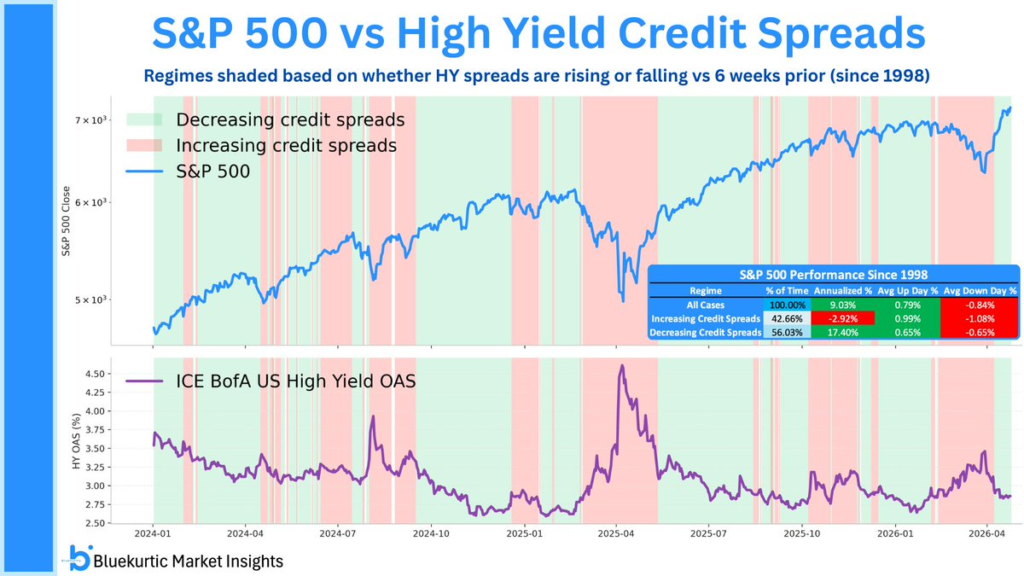

The chart: where the disconnect becomes visible

A useful way to visualize this market disconnect is to compare the S&P 500 with US high-yield credit spreads.

The S&P 500 shows how equity investors are pricing growth, earnings and risk appetite. High-yield spreads, on the other hand, show how investors are pricing stress in lower-quality corporate debt. When equities rise while high-yield spreads remain sticky or start widening, it suggests that the stock market and the credit market are not telling the same story.

That is exactly why this chart matters.

Image source: Bluekurtic Market Insights.

Stocks continued to price resilience through much of the period, but credit did not always fully confirm that optimism. When equities stay elevated while high-yield spreads widen or refuse to compress, the disconnect between financial markets and the real economy becomes much easier to see.

The chart does not prove that a recession is inevitable. But it does show why investors should be careful with headline equity strength. If the S&P 500 remains strong while credit stress begins to rise, the market may be pricing a soft landing while corporate debt is quietly preparing for something rougher.

In my view, this is one of the cleanest ways to understand the current environment. Equity indices can be distorted by mega-cap leadership, AI enthusiasm and liquidity. Credit spreads are usually more sensitive to refinancing pressure, default risk and the real cost of capital. That makes them a valuable warning signal when the market narrative becomes too comfortable.

For the article, I would use the chart as the visual anchor of the argument: the disconnect is not just a theory it appears when different asset classes start disagreeing with each other.

What investors should watch next

The disconnect will not last forever. Either the economy improves enough to justify market optimism, or markets eventually adjust to weaker fundamentals.

The key signals to watch are:

| Signal | Why it matters |

|---|---|

| High-yield credit spreads | Early warning of stress in weaker companies |

| Earnings revisions | Shows whether analysts are cutting profit expectations |

| Labor market data | Confirms whether slowdown risk is spreading |

| Consumer spending | Reveals pressure on the real economy |

| Treasury yields | Shows how bond markets price growth and rate expectations |

| Gold | Reflects demand for safety and macro protection |

| Oil | Captures the tension between geopolitics and demand weakness |

The most dangerous setup would be one where equities remain complacent while credit, employment and consumption deteriorate. That would suggest the market is not solving the disconnect it is ignoring it.

Why the Market Disconnect Matters More Than It Looks

The biggest risk in today’s market is not that stocks are rising.

The real risk is that financial markets may be pricing a much cleaner economic scenario than the one actually developing underneath the surface.

When equities continue climbing while consumers face higher prices, governments carry heavier debt loads and central banks remain cautious, the result is a growing disconnect between market expectations and economic reality.

From my perspective, this is where investors need to be careful.

Markets can stay optimistic for a long time when liquidity is strong, earnings expectations remain resilient and mega-cap technology companies continue supporting index performance. But if that optimism becomes too disconnected from fundamentals, even a small disappointment can trigger a larger repricing.

The problem is that the index itself can hide weakness.

A few large companies can push the S&P 500 higher while smaller companies, consumers and more cyclical sectors are already showing signs of stress. That creates the illusion of broad strength when the real economy may be much more fragile than the headline market suggests.

This is especially important in a higher-rate environment.

When interest rates remain elevated, companies with weaker balance sheets face higher refinancing costs, consumers feel more pressure from credit cards and loans, and governments have less fiscal flexibility. At the same time, investors may still be paying premium valuations for future growth that has not yet fully materialized.

That is the essence of the disconnect.

The market is looking forward to a soft landing, lower inflation and future rate cuts.

But the economy is still dealing with sticky inflation, expensive debt, weaker purchasing power and geopolitical uncertainty.

If those two stories fail to converge, volatility could return quickly.

How the Market Disconnect Develops

Strong index performance can hide underlying economic weakness when liquidity and mega-cap stocks drive markets higher while consumers, debt and refinancing pressures continue to deteriorate.

Conclusion: the gap will close one way or another

The market disconnect is not just a theory anymore. It is becoming one of the clearest ways to understand the current macro environment.

Stocks are still trying to price optimism. Bonds are more cautious. Gold is signaling uncertainty. Commodities are split between geopolitical risk and growth concerns. And the real economy is not giving the same clean bullish signal that equity markets seem to suggest.

My view is that investors should stop asking whether the stock market is “right” or “wrong.” Markets can be right for a while and still become vulnerable later. The better question is whether current prices leave enough room for disappointment.

Because if recession risk rises and the real economy continues to weaken, the disconnect will eventually close.

The only uncertainty is how: through a stronger economy, or through lower asset prices.

FAQs

What is the market disconnect from the real economy?

It is the gap between strong financial market performance and weaker underlying economic conditions such as slowing consumption, tighter credit, weaker hiring or lower business confidence.

Why can stocks rise when the economy is slowing?

Stocks can rise because investors price future expectations, not just current conditions. Rate-cut hopes, liquidity, AI optimism and strong mega-cap earnings can support markets even when the broader economy weakens.

What asset class usually warns first?

High-yield credit can be one of the earliest warning signs. If spreads widen while equities remain strong, it may suggest credit investors are pricing more stress than stock investors.

How could a recession affect bonds?

Government bonds may benefit if yields fall on weaker growth expectations. Corporate credit, especially high-yield debt, would likely face more pressure.

Is gold useful during a market disconnect?

Gold can be useful when uncertainty rises, real yields fall, or investors seek protection against financial instability, policy mistakes or debt concerns.

What happens to commodities in a recession?

Industrial commodities usually weaken if demand slows. Oil depends on both demand and supply shocks, while gold often behaves more defensively.