A potential US-Iran peace framework is no longer just a geopolitical headline. It has become a full macroeconomic event.

Markets are reacting as if one of the biggest inflation risks of the year may be starting to unwind. Oil prices are falling sharply, global equities are rallying, bond yields are moving lower and investors are quickly repricing the probability of a wider Middle East shock fading from the market.

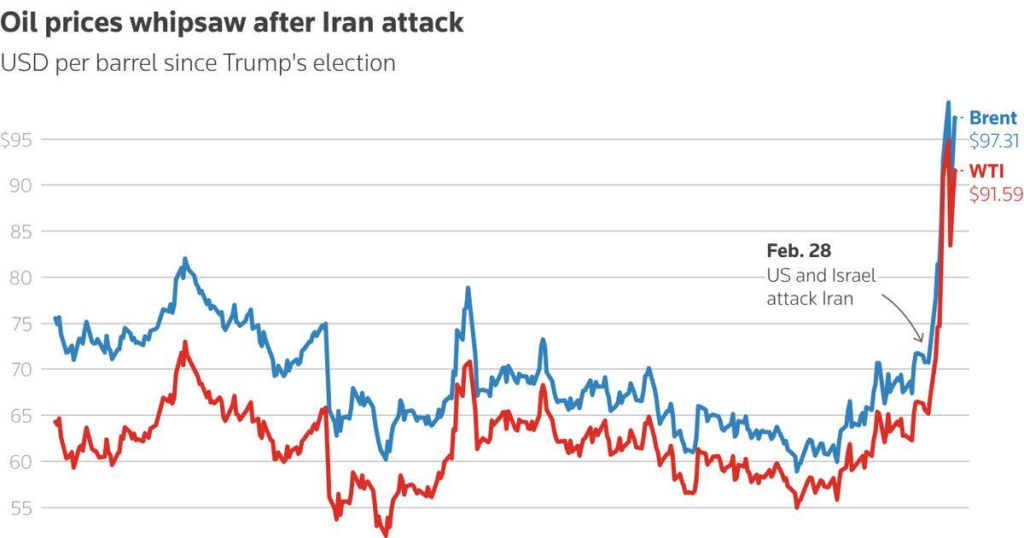

Oil prices surged after renewed geopolitical escalation involving Iran, increasing inflation concerns and market volatility

According to reports first cited by Axios and later confirmed as accurate by a Pakistani source involved in the negotiations, the United States and Iran are closing in on a one-page memorandum of understanding to end the war. The proposed framework would reportedly include a moratorium on Iran’s uranium enrichment, sanctions relief from Washington, the release of frozen Iranian funds and the easing of restrictions around the Strait of Hormuz. Iran is expected to respond to key terms within 48 hours.

That last detail is crucial: this is not a signed deal yet.

But markets do not wait for signatures. Markets price probabilities. And right now, they are pricing a much higher probability that the oil shock, shipping disruption risk and geopolitical inflation premium could fade.

Why This Is a Macro Story, Not Just a Peace Story

The reason this matters so much is simple: the Iran conflict has been sitting directly on top of the global inflation trade.

The Strait of Hormuz is one of the most important energy chokepoints in the world. Any risk to shipping there immediately feeds into crude oil, gasoline expectations, airline costs, freight prices, inflation forecasts and, eventually, central bank policy.

That is why this possible deal matters far beyond Tehran and Washington.

It affects:

- Oil prices.

- US inflation expectations.

- Federal Reserve rate-cut probabilities.

- Treasury yields.

- The US dollar.

- Stock market risk appetite.

- Energy stocks.

- Emerging markets.

- Crypto and high-beta assets.

In other words, this is not only about whether Iran accepts. It is about whether markets can remove a major geopolitical risk premium from the entire global economy.

And that is exactly what appears to be happening today.

Reuters reported that global stocks surged while oil prices slid after the US-Iran peace deal report. Brent crude fell 7.5% to around $101.70 a barrel, the STOXX 600 rose more than 2%, MSCI’s global equity index reached a new record and US 10-year Treasury yields dropped to around 4.35%. The dollar also weakened against major currencies.

That is a classic macro relief trade: oil down, bonds up, yields down, stocks up, dollar down.

The Market Is Trading One Big Idea: Lower Oil Means Lower Inflation Pressure

The most important market reaction is not the stock rally. It is the oil move.

Oil is the transmission mechanism between war and inflation.

When crude spikes, investors immediately worry about higher gasoline prices, higher transportation costs, weaker consumer spending and a Federal Reserve forced to stay tighter for longer. That creates a toxic mix for risk assets: higher inflation, higher yields and lower growth.

But when oil falls sharply, the macro picture changes.

Lower oil can:

- Reduce headline inflation pressure.

- Ease pressure on consumers.

- Improve corporate margins in transport-heavy sectors.

- Support airlines, retailers and industrials.

- Give the Fed more room to sound dovish.

- Lower recession fears linked to an energy shock.

That is why the reaction has been so powerful. The market is not only celebrating the possibility of peace. It is celebrating the possibility that one of the biggest upside risks to inflation may be disappearing.

In my view, this is the central point: markets are not just buying peace; they are buying a lower inflation path.

Will Iran Accept the Deal?

My current estimate is that Iran has a 55% to 65% chance of accepting some version of the proposed framework.

That does not mean Iran will simply say yes to every condition. It means the incentives to keep negotiating are strong enough that a modified agreement looks more likely than a total collapse.

Iran has several reasons to accept or at least move closer to a deal:

First, sanctions relief would matter immediately. Access to frozen funds and reduced financial restrictions would provide economic oxygen at a time when war pressure is expensive.

Second, a diplomatic framework allows Tehran to avoid looking like it is surrendering militarily. A one-page memorandum gives both sides enough ambiguity to claim a political win.

Third, pausing uranium enrichment may be more acceptable if the duration is negotiable. Reports suggest there is still disagreement over the length of the enrichment moratorium, with Iran preferring a shorter timeline and Washington pushing for a longer one.

But there are also major reasons Iran may resist.

The leadership may be divided. Hardliners could view any enrichment pause as a strategic concession. The release of frozen funds may not be enough if Tehran believes the US could reimpose sanctions later. And any deal that appears too favorable to Washington could become politically toxic inside Iran.

So I would frame it this way: Iran is likely to engage, but acceptance depends on whether the final language lets Tehran sell the deal at home.

That is why the next 48 hours matter so much. The first reaction from Iran may not be a clean yes or no. It could be a conditional acceptance, a request for changes or a delay dressed up as negotiation.

Has the Market Already Reacted?

Yes strongly.

This is not a small move. It is already a broad cross-asset repricing.

Reuters reported that stocks and bonds rallied after the Axios report, while oil prices fell sharply. European equities rose more than 2%, economically sensitive sectors such as banks and miners outperformed, and oil and gas stocks declined. US 10-year Treasury yields dropped around 6 basis points to 4.35%, while German, British and Italian yields also fell.

Energy equities are taking the other side of the trade. Barron’s reported that Exxon Mobil and Chevron fell in premarket trading, while several other oil names also dropped as crude prices sold off. West Texas Intermediate crude was down more than 9% at one point, according to the report.

That tells us the move is not isolated. It is not just traders chasing headlines. It is a full rotation:

Out of war-premium assets. Into risk assets. Out of oil. Into equities and bonds.

The market is saying: if the war risk fades, the inflation risk fades with it.

Is This a Real Rally or a False Move?

This is where investors need to be careful.

I would not call this a fake move. The reaction makes macro sense. If the probability of peace rises, oil should fall, yields should ease and equities should rally.

But I also would not call it a fully confirmed trend yet.

Right now, this is a probability rally, not a confirmation rally.

The market is pricing a better outcome before the outcome has actually happened. That means the rally can continue if Iran accepts, but it can also reverse violently if Tehran rejects the deal or if the final terms look weaker than expected.

There is also a “buy the rumor, sell the news” risk. If investors price too much optimism before the agreement is signed, even a positive announcement could trigger profit-taking.

So the most accurate reading is this:

The move is real, but fragile.

It is real because the macro logic is strong. It is fragile because the political risk has not disappeared.

What This Means for the Fed

This is where the story gets even more interesting for US investors.

The Federal Reserve has been fighting a complicated inflation backdrop. Energy shocks are difficult because they hit consumers directly and can quickly change inflation expectations. If oil remains elevated because of war risk, the Fed has less flexibility to cut rates, even if growth slows.

But if oil falls and the Middle East risk premium fades, the Fed gets breathing room.

Lower oil prices could reduce headline CPI pressure. Lower yields could ease financial conditions. A weaker dollar could support global risk appetite, although it can also complicate import prices. The key is that a successful deal would remove one major reason for the Fed to stay defensive.

That is why the bond market rally matters.

When Treasury yields fall on geopolitical relief, the market is effectively saying: less oil risk, less inflation risk, less need for extreme policy caution.

This does not guarantee rate cuts. But it improves the macro setup.

Who Wins If the Deal Happens?

If Iran accepts and the agreement holds, the likely winners are:

Airlines and transports. Lower fuel costs are directly positive for margins.

Consumer stocks. Lower gasoline prices can support disposable income and sentiment.

Industrials and manufacturers. Lower input and freight costs help margins.

Banks and cyclicals. A better growth outlook and less geopolitical stress can support risk appetite.

Growth stocks and tech. Lower yields are usually supportive for long-duration assets.

Emerging markets. A weaker dollar and lower energy stress can improve financial conditions.

That explains why the equity rally is broad. The market is not only buying peace. It is buying a softer inflation impulse and easier financial conditions.

Who Loses?

The clear losers are oil-linked assets.

Energy producers, oil services companies and parts of the commodity complex are vulnerable if crude continues to unwind the war premium.

That does not mean the long-term oil story is dead. Supply-demand fundamentals still matter. But a major chunk of recent oil strength may have been geopolitical. If that premium disappears, energy stocks can underperform even while the broader market rallies.

Gold is more complicated. Lower geopolitical risk is usually negative for gold, but lower yields and a weaker dollar can support it. That creates a mixed setup rather than a clean bearish one.

Crypto could benefit if risk appetite improves, but it remains highly sensitive to liquidity and broader sentiment.

The Bear Case: What If Iran Says No?

If Iran rejects the framework, the macro trade could reverse quickly.

Oil would likely spike. Energy stocks would rebound. Treasury yields could move higher if investors fear a renewed inflation shock. Equities would probably sell off, especially sectors exposed to fuel costs and consumer weakness.

The worst-case scenario would be a breakdown in talks combined with renewed disruption around Hormuz. That would bring back the market’s biggest fear: a geopolitical oil shock that feeds directly into inflation.

In that scenario, the Fed would face a much harder problem. Growth could weaken while inflation risk rises. That is exactly the kind of environment equity markets hate.

So the risk is asymmetric. A deal can extend the rally, but a rejection can unwind it fast.

My Take: The Market Is Right, But It May Be Early

I think the market reaction is justified.

A credible US-Iran framework would be one of the most important macro events of the year because it could remove a major oil shock from the inflation outlook. Stocks should like that. Bonds should like that. The dollar should soften. Oil should fall.

But I also think the market may be moving faster than the diplomacy.

The deal is not signed. Iran has not formally accepted. The enrichment issue remains sensitive. Domestic politics in Tehran could still derail the process. And traders may already be pricing a best-case scenario.

So my base case is this:

Peace is closer, the macro outlook has improved, but the rally is not fully de-risked.

For investors, the next move depends on confirmation. If Iran accepts, the peace trade can continue: lower oil, lower yields, stronger equities. If Iran rejects or delays, today’s rally may look like a classic headline-driven squeeze.

The key question is no longer simply “will there be peace?”

The real macro question is:

Can this deal permanently remove the war premium from oil and give the Fed a cleaner path toward easier policy?

That is what markets are trading today.

Conclusion

The potential US-Iran peace deal is becoming a major macroeconomic catalyst. It touches every major market variable: oil, inflation, Fed policy, Treasury yields, the dollar and equity risk appetite.

Markets have already reacted strongly because investors believe the probability of de-escalation has improved. Oil is falling, stocks are rising, bonds are rallying and the dollar is weakening. That is a textbook reaction to lower geopolitical inflation risk.

But this is still a probability trade, not a confirmed peace deal.

Iran’s response over the next 48 hours will decide whether this becomes a lasting macro reset or just another false rally driven by headlines.

For now, the message from markets is clear: peace is not priced in completely, but the war premium is already coming out fast.

FAQs

Why is the US-Iran deal important for markets?

Because it could reduce the geopolitical premium in oil, lower inflation expectations and give the Federal Reserve more flexibility on rates.

Has the market already reacted?

Yes. Global stocks rallied, oil prices dropped sharply, bond yields fell and the dollar weakened after reports that the US and Iran were close to a memorandum.

What is the probability Iran accepts?

My estimate is around 55% to 65% for some version of the framework. The incentives are strong, but political and nuclear-enrichment issues remain unresolved.

Is the rally real or fake?

It is real as a macro relief rally, but it is not fully confirmed. It depends on Iran’s formal response and the final terms of the agreement.

What happens to oil if Iran accepts?

Oil could fall further as the war premium fades, especially if restrictions around the Strait of Hormuz ease.

What happens if Iran rejects the deal?

Oil could rebound sharply, stocks could fall and inflation fears could return, putting pressure back on the Fed and Treasury yields.