KYC is one of those boring acronyms that sounds harmless until it starts following you everywhere.

It stands for Know Your Customer, and in plain English, it means this: before a company lets you use a service, it wants to know who you are. That can mean your legal name, address, phone number, email, government ID, passport, selfie, payment method, company documents, beneficial ownership records, IP address, device data, or even biometric checks.

In banking and crypto, KYC is already normal. You open an exchange account, and suddenly you are uploading your ID, taking a live selfie, proving your address, and hoping some automated system does not flag you for no clear reason.

But now the question is moving into a much bigger area:

Does the US want KYC to use AI?

The answer is: not exactly for every normal chatbot user at least not yet. But the US government has already explored rules that would push KYC-style identity checks into the AI infrastructure layer, especially for cloud providers, foreign customers, resellers, and large AI model training. In January 2024, the US Department of Commerce proposed rules that would require US Infrastructure as a Service providers to identify certain foreign customers and report when foreign persons use US cloud infrastructure to train large AI models that could be used for malicious cyber activity.

So no, this is not as simple as “upload your passport to use ChatGPT tomorrow.”

But yes, the direction is obvious: AI access is becoming a regulated checkpoint.

And personally, I do not think people should ignore that.

Security against hackers? Fine.

Mass surveillance dressed up as security? That is where I start having a problem.

What Is KYC in Simple Terms?

KYC means Know Your Customer. It is a process companies use to verify that a customer is a real person or a legitimate business.

The classic version comes from finance. Banks, payment processors, brokerages, fintech apps, and crypto exchanges use KYC because governments require them to fight money laundering, fraud, terrorist financing, sanctions evasion, and identity theft.

In practice, KYC usually means proving your identity before you can use a service.

You may be asked for:

- Your full legal name;

- Date of birth;

- Address;

- Government ID;

- Passport;

- Driver’s license;

- Phone number;

- Email;

- Tax information;

- Source of funds;

- Business registration documents;

- Beneficial ownership information;

- Selfie or live video verification;

- Biometric checks;

- Payment details.

On paper, the idea is simple: if platforms know who is using them, criminals have a harder time hiding.

That sounds reasonable until you see how far it can go.

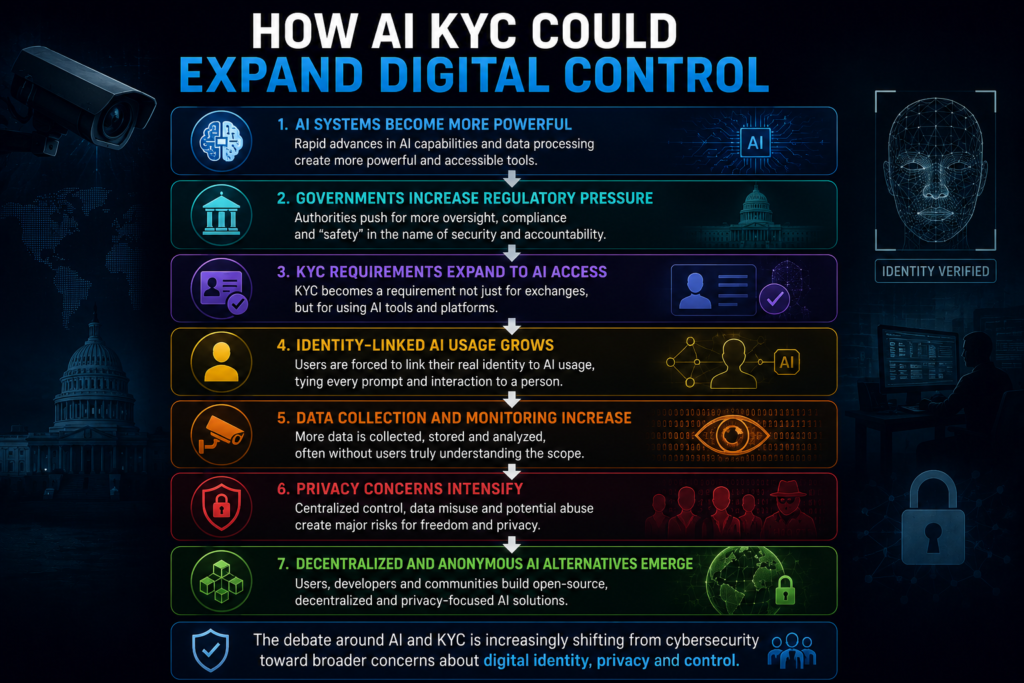

Because KYC is not just “checking an ID.” It is also the creation of a permission system. You are allowed in only after you identify yourself. You are blocked if you fail the check. You can be monitored after you pass. And the service provider can be forced to store, share, or report your data. That is why KYC is not just a compliance tool. It is also an access-control tool. And when access-control tools move from banks into AI, things get much more serious.

The Key Difference: AI Doing KYC vs KYC to Use AI

This is the part a lot of people mix up.

There are two completely different ideas here:

- AI used to perform KYC.

- KYC required before using AI.

They sound similar, but they are not the same thing.

AI Doing KYC

This is already happening everywhere. Financial platforms use AI to scan documents, compare selfies with IDs, detect fake passports, recognize suspicious behavior, analyze transactions, spot deepfakes, and flag fraud.

For example, KYC systems can use optical character recognition to read identity documents, facial recognition to match a selfie with an ID, and liveness detection to make sure the person is not using a static photo or manipulated video.

This version is basically:

“We use AI to verify who you are.”

That is the normal compliance use case. Banks, exchanges, fintechs, and payment apps love it because it makes onboarding faster and cheaper.

But that is not the controversial part.

KYC to Use AI

The more important issue is the reverse:

“You must verify who you are before you can access powerful AI tools, cloud infrastructure, APIs, model training, or compute.”

That is a very different world.

Now KYC is not just being helped by AI. KYC becomes the gatekeeper of AI.

This could apply to:

- Cloud accounts;

- AI APIs;

- GPU clusters;

- Model training;

- Advanced model weights;

- Enterprise AI platforms;

- Foreign resellers;

- Companies training frontier models;

- Customers using US infrastructure.

This is where the US debate becomes interesting.

The US government has been especially focused on cloud infrastructure, because powerful AI models are not trained on a laptop in someone’s bedroom. They are usually trained on large-scale compute: GPUs, cloud clusters, data centers, and infrastructure providers.

That means governments do not need to control every user directly at first. They can pressure the infrastructure layer.

And that is the real story.

So, Does the US Want KYC to Use AI?

The honest answer is:

The US has already pushed toward KYC-style rules for AI infrastructure, especially when foreign customers use US cloud services to train large AI models.

Under the Biden administration’s Executive Order 14110, the Commerce Department was directed to develop rules requiring US cloud providers to report certain AI training activity by foreign persons. The proposed rule included customer identification requirements for US Infrastructure as a Service providers and foreign resellers. It also focused on large AI models with potential capabilities that could be used in malicious cyber-enabled activity.

That matters because it shows the US government was not only thinking about AI safety in abstract terms. It was looking at the practical chokepoints: cloud accounts, resellers, foreign customers, compute access, and large model training.

However, there is an important update: President Trump revoked Biden’s AI Executive Order 14110 in January 2025 and issued a new order focused on removing barriers to American AI leadership.

So the current situation is not “the US has one settled permanent rule forcing everyone to do KYC to use AI.”

It is more complicated:

- The US has shown strong interest in identifying who uses American cloud infrastructure for advanced AI;

- The legal and regulatory path has shifted with the change in administration;

- Export controls, model weight restrictions, AI chip controls, and cloud reporting remain part of the broader national security conversation;

- The idea of “Know Your Customer” for AI compute has not disappeared.

In other words, the exact rule may change, but the direction is still clear: AI is being treated as strategic infrastructure.

And when something becomes strategic infrastructure, governments usually want identity, logs, permissions, reporting, and control.

No, This Is Not Exactly “Upload Your ID to Use a Chatbot”… Yet

It is important not to exaggerate.

When people hear “KYC for AI,” they may imagine this:

“Before you ask a chatbot to write an email, you must upload your passport.”

That is not what the US proposal was mainly about.

The focus was more on foreign access to US cloud infrastructure, especially if that access could be used to train large AI models with dangerous cyber capabilities. The Department of Commerce proposal discussed Customer Identification Programs for IaaS providers and reporting obligations for certain AI model training transactions involving foreign persons.

That means the first targets are more likely to be:

- Cloud providers;

- Foreign customers;

- Resellers;

- Companies training large models;

- Entities using large amounts of compute;

- Organizations connected to high-risk jurisdictions;

- Infrastructure used for cyber operations.

Not the average person asking an AI tool to summarize a document.

But here is the problem: rules often start at the enterprise or infrastructure level and then slowly become normal everywhere else. Crypto is a good example.

At first, KYC was mainly for banks and regulated exchanges. Then it spread to more platforms, more jurisdictions, more payment rails, more wallets, more fiat on-ramps, more compliance providers, and more automated risk scoring systems.

Once a society accepts the idea that access requires identification, it becomes easier to expand that logic.

Today it is cloud infrastructure. Tomorrow it could be API access.

After that it could be certain models, certain prompts, certain countries, certain users, certain payment methods, or certain “risk profiles.”

That is why this debate matters now, before it becomes invisible.

Why Governments Justify It: Crypto Hacks, Deepfakes, and Cyberattacks

The security argument is not fake. There are real problems.

AI can help criminals scale attacks. It can make phishing more convincing. It can generate malware assistance, automate social engineering, create fake documents, produce synthetic identities, and improve scams. Deepfakes can help attackers bypass weak identity checks. Crypto hacks can move stolen funds across exchanges, mixers, wallets, bridges, and shell accounts.

When hackers steal crypto, they need infrastructure.

They may need:

- Exchange accounts;

- Cloud servers;

- Fake identities;

- Payment rails;

- VPNs;

- Domains;

- Phishing kits;

- AI tools;

- Automated scripts;

- Mule accounts;

- Companies that look legitimate.

From a government perspective, KYC is attractive because it creates a trail.

If every account has a verified person or company behind it, investigators can follow the chain. If a foreign actor rents US cloud infrastructure to train a model that could support cyberattacks, the government wants to know who they are. If a reseller gives access to that infrastructure, the government wants the reseller to verify the customer too.That is the official logic. And to be fair, I understand part of it.

Nobody wants North Korean hackers, ransomware groups, state-backed attackers, crypto scammers, or deepfake fraud networks freely using high-end US infrastructure with zero checks.

Security matters. The problem is not the idea of stopping hackers. The problem is what governments often do with a tool once the public accepts it.

Security Against Hackers, Yes. Mass Surveillance, No.

This is where I draw the line.

I am not against security. I am not saying platforms should ignore fraud. I am not pretending crypto hacks are harmless. I understand why governments care about AI-enabled cyberattacks.

But I do not like how every new control mechanism arrives wearing the same costume:

“Do not worry, it is only for your safety.”

We heard that with financial surveillance. We heard it with online identity checks. We heard it with crypto regulation. Now we are hearing it with AI infrastructure.

In my view, KYC for AI can become another excuse to control the population if it is expanded without strict limits.

Because once identity becomes mandatory for access, anonymity disappears by default.

And anonymity is not only for criminals. It is also for whistleblowers, journalists, dissidents, developers, researchers, activists, political minorities, people in unstable countries, and ordinary users who simply do not want every action tied to a permanent identity file.

That is the uncomfortable part.

A government can say:

“We only want to stop malicious cyber activity.”

But the system it builds may also allow:

- Tracking who uses AI;

- Blocking access based on nationality;

- Restricting tools by political risk;

- Monitoring model usage;

- Forcing platforms to report activity;

- Creating databases of AI users;

- Pressuring providers to deny service;

- Expanding identity checks into normal consumer products.

And once the infrastructure exists, the temptation to expand it is massive.

So yes, stop hackers.

But do not pretend that every identity mandate is automatically harmless.

The Big Hole in the System: Leaked Models, Proxies, and Shell Companies

Here is the part regulators often do not like to admit:

KYC works best against normal users. It does not always stop sophisticated actors.

A regular person gets blocked because their document photo is blurry, their country is unsupported, their address does not match, or the automated system flags them.

But a well-funded actor?

They can use intermediaries. They can use shell companies. They can use nominees. They can use foreign resellers. They can use stolen identities. They can use compromised accounts. They can use infrastructure in another jurisdiction. They can buy access indirectly. They can wait for open-source or leaked models.

And if a powerful model’s weights leak online, KYC becomes almost irrelevant. Once model weights are copied and distributed, you cannot put the file back inside the box. People can mirror it, torrent it, run it locally, fine-tune it, modify it, and move it across borders.

That is why I see a huge weakness in the “KYC solves dangerous AI access” argument. It may slow down some bad actors. It may create friction. It may help investigations. It may reduce casual abuse. But it will not magically stop determined groups with money, networks, or state support.

Meanwhile, the average user becomes easier to monitor. That is the tradeoff nobody wants to say out loud.

A strict KYC system can become theater: very visible, very expensive, very invasive, and very effective at controlling ordinary people while the most serious actors route around it.

This is exactly why the debate should not be framed as:

“Do you support hackers or do you support KYC?”

That is a false choice.

The real question is:

“Can we fight real cyber threats without building a permanent identity checkpoint for access to intelligence tools?”

That is the question people should be asking.

The debate around AI and KYC is increasingly shifting from cybersecurity toward broader concerns about digital identity, privacy and control.

Why This Matters for Crypto

Crypto is one of the main reasons this topic is becoming urgent.

Crypto hacks are public, expensive, and embarrassing. When funds are stolen from exchanges, bridges, wallets, or DeFi protocols, regulators see a familiar pattern: pseudonymous accounts, fast transfers, cross-border movement, fake identities, mixers, and weak customer verification.

AI adds fuel to that fire.

AI can help scammers create better phishing messages. It can help generate fake customer support scripts. It can create deepfake videos. It can automate impersonation. It can help attackers research targets. It can create fake documents or synthetic profiles. It can make social engineering cheaper and faster.

So when governments connect AI, KYC, and crypto, the logic is easy to understand:

- Crypto has money;

- Hackers want money;

- AI can help hackers;

- KYC can create identity trails;

- Therefore, more KYC is presented as the solution.

But again, the real world is messier.

If a crypto hacker uses a fake identity, a mule, a shell company, or a compromised verified account, KYC does not prevent the attack. It may help later during investigation, but it does not necessarily stop the harm before it happens.

And when KYC databases themselves get hacked, the damage becomes even worse. Now criminals do not just steal money. They steal passports, selfies, addresses, phone numbers, and identity documents that can be reused for fraud.

That is the irony.

A system created to prevent identity fraud can become a goldmine for identity fraud.

Could This Reach Regular AI Tools?

Yes, eventually it could.

Not necessarily tomorrow. Not necessarily everywhere. Not necessarily through one giant law that says, “Everyone must do KYC to use AI.”

It could happen slowly.

First, cloud providers identify foreign customers.

Then resellers must verify business clients.

Then API providers require stricter business verification.

Then high-capability models require approved access.

Then certain countries are blocked.

Then anonymous payment methods disappear.

Then consumer platforms introduce “verified user” tiers.

Then unverified users get lower limits, weaker models, or restricted features.

That is how these things often happen: not as one dramatic event, but as a gradual normalization.

The argument will always sound reasonable:

- Prevent fraud;

- Stop deepfakes;

- Protect children;

- Fight scams;

- Block terrorists;

- Stop cyberattacks;

- Protect national security;

- Enforce sanctions;

- Prevent election manipulation;

- Protect intellectual property.

Some of those concerns are real. But the solution can still be dangerous.

Because once access to AI depends on identity, AI stops being just a tool. It becomes a permissioned system.

And whoever controls the permission layer controls who gets to think, build, automate, research, publish, compete, and create with the most powerful tools of the next decade.

That is not a small issue.

What Would a Better Approach Look Like?

If governments are serious about preventing malicious AI use, they should focus on targeted controls instead of turning every user into a suspect.

A better approach would include:

- Strong security standards for cloud providers;

- Monitoring of genuinely high-risk compute usage;

- Narrow warrants or legal processes for sensitive user data;

- Strict limits on data retention;

- Transparency reports;

- Independent audits;

- Clear definitions of “high-risk AI training”;

- Protection for open research;

- Privacy-preserving verification where possible;

- Penalties for misuse of KYC data;

- Rules against indefinite identity tracking;

- Strong breach liability for companies storing IDs.

The key principle should be simple:

Control dangerous behavior, not ordinary access.

If someone is training a massive model with clear malicious intent, that is a real issue. If someone wants to use an AI tool to code, translate, write, research, study, build a business, or understand crypto security, they should not have to surrender their identity by default.

The burden should be on governments and companies to justify invasive checks, not on users to prove they deserve privacy.

My Take: The US Is Testing the Gate

So, does the US want KYC to use AI?

My answer is:

The US has already moved toward KYC-style controls for parts of the AI stack, especially cloud infrastructure and foreign access to large model training. It is not yet a universal ID requirement for every AI user, but the gate is being tested.

That is the key point. The first gate is not always the chatbot. It is the compute layer. The cloud provider. The API. The reseller. The company account. The GPU cluster. The model training run.

And once that gate exists, expanding it becomes much easier.

I understand the cybersecurity argument. AI can absolutely be abused. Crypto hacks are real. Deepfakes are real. Foreign cyber operations are real. Pretending none of that matters would be naive. But I also think it is naive to believe identity mandates will only ever be used against “bad guys.”

In my opinion, this is another excuse that can easily become population control if people do not push back early. Not because every regulator is evil.

But because every system built for control eventually attracts people who want to control more.

And the worst part? The most dangerous actors will still find ways around it. Leaked models will circulate without KYC. Shell companies will pass checks. Proxies and intermediaries will appear. Sophisticated groups will route around the system.

Meanwhile, the normal user gets tracked. That is why the debate should not be “KYC or chaos.”

It should be:

How do we stop real AI abuse without turning access to intelligence into a government-approved privilege?

That is the conversation worth having.

FAQs About KYC and AI

What does KYC mean?

KYC means Know Your Customer. It is a verification process used to confirm the identity of a person or business before they can use a service. It is common in banking, fintech, crypto exchanges, payment processors, and regulated financial platforms.

Is the US already forcing everyone to do KYC to use AI?

No. The US is not currently forcing every normal user to upload ID just to use a chatbot. The more relevant US proposals have focused on cloud infrastructure, foreign customers, resellers, and large AI model training that could be used for malicious cyber activity.

What is the difference between AI doing KYC and KYC to use AI?

AI doing KYC means companies use AI to verify documents, selfies, biometrics, and fraud signals. KYC to use AI means a user, company, reseller, or foreign customer may need identity verification before accessing AI infrastructure, compute, APIs, or model training.

Why does AI matter for crypto hacks?

AI can make crypto crime easier to scale. It can help with phishing, fake identities, deepfakes, social engineering, scam automation, and document manipulation. That gives regulators a reason to argue for stricter identity checks around financial platforms, cloud infrastructure, and AI tools.

Can KYC stop hackers?

KYC can help create friction and provide an identity trail, but it does not fully stop sophisticated hackers. Bad actors can use stolen identities, compromised accounts, shell companies, proxies, foreign resellers, or leaked models. KYC is useful in some cases, but it is not a magic shield.

Why can KYC be dangerous for privacy?

KYC can create large databases of sensitive personal information: IDs, selfies, addresses, phone numbers, payment records, and business ownership details. If these databases are abused, leaked, hacked, or expanded into broader surveillance systems, the privacy risk becomes serious.

Could KYC become mandatory for AI APIs or advanced models?

It is possible. The most likely path would be gradual: stricter checks for cloud providers first, then resellers, enterprise accounts, high-compute users, API access, and eventually some advanced model features. That does not mean it is guaranteed, but the direction is realistic.

Is KYC for AI about safety or control?

It can be both. The safety argument is real: AI can be used for cyberattacks, deepfakes, fraud, and crypto scams. But identity systems can also become tools of control if they are broad, permanent, opaque, and applied to ordinary users instead of narrowly targeted at genuinely high-risk activity.