The Federal Reserve held interest rates steady today, leaving the federal funds target range at 3.50% to 3.75% in what looks, on the surface, like a simple pause. But I do not read this meeting as routine. To me, this was a transition meeting: Jerome Powell is preparing to leave the chair role, Kevin Warsh is waiting in the wings, the Fed is visibly divided, and the Iran war has made the inflation outlook harder to trust.

The headline is easy: officials held rates steady. The real story is more complicated. The Fed is trying to avoid cutting too soon while inflation is still elevated, energy prices are rising, and geopolitical uncertainty is bleeding into the economic forecast. Powell also said he plans to stay on as a Fed governor after his chair term ends, which means his influence at the central bank may not disappear overnight.

In my view, the most important takeaway is this: the Fed did not choose calm; it chose caution.

The Fed Held Rates Steady But This Was Not a Quiet Pause

The Federal Reserve’s decision keeps borrowing costs at a restrictive level. That matters because a rate hold is not the same as doing nothing. When rates stay elevated, mortgages, credit cards, auto loans, business loans, and market valuations all continue to feel the pressure.

The Fed is essentially saying: inflation is still too risky, the economy is still strong enough to absorb tight policy, and the shock from the Middle East makes it dangerous to declare victory too early. The official message is not “we are done.” It is closer to: we need more time.

What stands out is how divided the decision was. Reuters reported that the vote was the most divided Fed decision since 1992, with four dissents: three officials objected to keeping language that leaned toward possible future cuts, while one official wanted an immediate cut.

That split matters. It tells us the Fed is no longer debating one clean path. Some policymakers are worried about inflation staying hot. Others are worried the economy could weaken if rates stay high for too long. That is exactly the kind of environment where markets can misread the Fed, and where every word from Powell or Warsh becomes more important.

Personally, I see this as the kind of Fed meeting where the “no change” decision hides a lot of movement underneath. Rates did not move, but the balance of risks did.

Why the Fed Did Not Cut Interest Rates

The Fed did not cut rates because inflation is still the central problem. Inflation remains above the Fed’s 2% target, and the recent increase in global energy prices has made that problem harder. Fed language cited Middle East developments as a major source of uncertainty and linked elevated inflation partly to higher global energy prices.

That is important because the Fed can cut rates when inflation is clearly cooling and the labor market needs support. But when inflation is sticky and oil prices are rising, cutting too early can make the central bank look careless. It could also loosen financial conditions at exactly the wrong moment.

The labor market also gives the Fed room to wait. Reporting today cited unemployment around 4.3%, which is not weak enough to force the Fed into emergency support mode.

I do not read the rate hold as the Fed saying everything is fine. I read it as the Fed choosing the risk it understands better. It knows high rates are painful. But it also knows that cutting into an oil-driven inflation shock could create a bigger credibility problem later.

The harder question is what happens if inflation stays high while growth slows. That would put the Fed in a much worse position: cut to protect jobs, or hold to protect price stability? Today’s meeting suggests officials are not aligned on that answer.

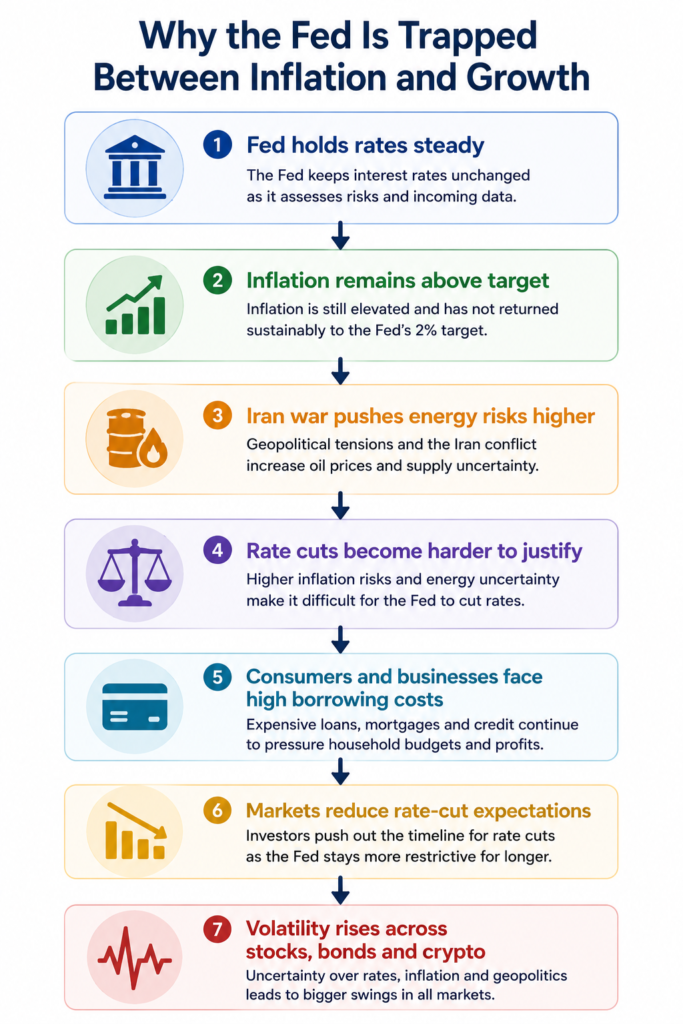

Why the Fed Is Trapped Between Inflation and Growth

Why the Fed Is Trapped Between Inflation and Growth

The Fed’s biggest problem right now is that the two sides of its mandate are moving in opposite directions.

Inflation remains too high for the central bank to cut aggressively, but keeping rates elevated for too long continues to pressure consumers, businesses and financial markets.

The Iran war makes that balance even harder. If oil prices stay elevated, inflation expectations may rise again. But if the Fed keeps policy restrictive, borrowing costs remain painful across mortgages, credit cards, corporate debt and market valuations.

From my perspective, this is why today’s rate hold matters. The Fed is not simply waiting. It is trying to avoid making the wrong mistake at the wrong time.

Powell’s Mandate Is Ending, But His Influence May Not Be

Jerome Powell’s term as Fed chair is nearing its end, but he has said he plans to remain on the Federal Reserve Board as a governor. That distinction matters. The chair leads the institution, sets the tone, and dominates communication, but Fed policy is not a one-person decision. Governors and regional Fed presidents still vote, dissent, debate, and influence the policy path.

What stands out to me is that Powell’s mandate may be ending on paper, but his influence is not disappearing overnight. By staying as governor, he keeps a seat inside the institution at a moment when the Fed is moving from one era into another.

Powell also said he would not try to act as a “shadow chair” and would support Kevin Warsh where possible. That is an important signal. It lowers the risk of an obvious public power struggle, but it does not erase the reality that Powell’s presence could still matter in committee debates.

This is why Powell staying on is such a meaningful part of today’s story. It gives the Fed continuity, but it also means the Warsh era may not begin with a totally clean slate. Powell’s approach to inflation, independence, and gradualism will still be present in the room, even if he is no longer the person at the podium.

For markets, that could be reassuring. For political actors expecting a sharp pivot, it could be frustrating. For the Fed itself, it may help preserve institutional memory during a very fragile handoff.

What Could Change Under Kevin Warsh

Kevin Warsh taking over as Fed chair would not automatically change interest rates. That is one of the biggest misunderstandings around central banks. A new chair can influence communication, priorities, and consensus-building, but he cannot simply command the full committee to cut or hike.

That said, leadership does matter. A Warsh-led Fed could sound different. It could frame inflation risks differently. It could shift how the Fed talks about financial conditions, government pressure, the balance sheet, or the acceptable trade-off between inflation and employment.

The key point is that Warsh would inherit a divided Fed, not a unified one. Today’s dissents show that the committee is already split between those worried about premature easing and those more open to cuts.

That makes the next phase harder to predict. Warsh may want to set a new tone, but the Iran war, oil prices, inflation data, and labor market numbers could limit his room for maneuver. In other words, the next Fed chair may arrive with political expectations attached to him, but the economy may not cooperate.

For me, the big question is not just whether Warsh wants a different Fed. It is whether he gets an economy that allows him to be different.

How the Iran War Clouds the Economic Outlook

The Iran war is not just a geopolitical headline for the Fed. It is an inflation problem, an oil problem, a confidence problem, and potentially a growth problem.

Energy prices are the clearest channel. If oil prices rise because of conflict in the Middle East, gasoline, transportation, shipping, production, and consumer prices can all feel the impact. Reuters reported that oil prices above $100 a barrel have contributed to inflation concerns and reduced expectations for rate cuts in 2026.

This kind of inflation is especially difficult for a central bank. If prices rise because demand is too strong, the Fed can cool demand by keeping rates high. But if prices rise because war disrupts energy supply, higher rates do not produce more oil. They simply slow the economy while consumers are already paying more for energy.

That is why the Iran war makes the outlook feel fragile. The Fed may be forced to fight inflation that is not fully caused by domestic demand. If it cuts too soon, it risks letting inflation expectations rise. If it waits too long, it risks squeezing households and businesses into a slowdown.

This is the uncomfortable part of today’s decision: the Fed is trying to manage an economy where the biggest shock may be outside its control.

What Steady Rates Mean for Consumers, Markets, and Businesses

For consumers, steady rates mean borrowing remains expensive. Mortgage rates are likely to stay under pressure, credit-card balances remain costly, and auto loans do not suddenly become easier to afford. A Fed pause does not reduce monthly payments. It simply means the current pressure continues.

For businesses, the message is similar. Higher financing costs can delay hiring, expansion, equipment purchases, and investment. Small businesses feel this especially sharply because they often rely on credit lines and variable-rate borrowing.

For investors, the decision complicates the rate-cut story. Markets often want a clear path: inflation cools, the Fed cuts, yields fall, stocks rise. Today’s meeting does not offer that clean path. It says inflation is still elevated, oil prices are a risk, and policymakers are divided. Reuters reported that stocks dipped and rate-cut expectations diminished after the decision.

Here is a simple way to read the impact:

| Group | What steady rates mean |

|---|---|

| Homebuyers | Mortgage affordability remains strained |

| Credit-card borrowers | High interest costs continue |

| Savers | Savings yields may remain relatively attractive |

| Businesses | Financing stays expensive |

| Investors | Rate-cut hopes become less certain |

| The Fed | More time to watch inflation, oil, and jobs |

I think this is the part many readers underestimate: holding rates steady still changes behavior. People delay buying homes. Companies delay borrowing. Investors rethink valuations. The economy keeps absorbing the pressure even without a new hike.

What Happens Next for Rate Cuts?

The next rate cut depends on four things: inflation, jobs, oil prices, and Fed leadership.

If inflation cools convincingly and the labor market weakens, the Fed could still cut. If oil prices stay high and inflation expectations rise, cuts become harder. If growth slows sharply, the Fed may be forced into a more difficult debate. And if Warsh takes over with a divided committee, communication may become even more important.

The Fed’s problem is that it cannot promise a path right now. The data are too messy, the committee is too divided, and the war has added too much uncertainty.

My read is that the Fed wants to keep the door open to cuts without giving markets permission to price in easy money too aggressively. That is a hard message to deliver. It is even harder during a leadership transition.

So the next phase of Fed policy may be less about one dramatic decision and more about a slow test of credibility. Can the Fed stay independent? Can Warsh build consensus? Can Powell remain a governor without becoming a rival center of gravity? Can inflation fall even with oil prices elevated?

Those are the questions that will define the next meetings

Bottom Line

The Fed held rates steady today, but this was not a boring pause. It was a cautious decision made under pressure from sticky inflation, war-driven energy risks, leadership change, and internal disagreement.

Powell’s decision to stay on as a Fed governor adds continuity, but it also makes the transition more complex. Warsh may soon lead the Fed, but he will inherit a divided committee and an economy shaped by forces no chair can fully control.

My final read is this: today’s Fed meeting was less about where rates are now and more about how difficult the next move has become. The Iran war has clouded the inflation outlook, Powell is not fully leaving the stage, and steady rates will continue to weigh on consumers, markets, and businesses until the Fed sees a clearer path.

FAQs

Did the Fed cut interest rates today?

No. The Federal Reserve held interest rates steady at a target range of 3.50% to 3.75%.

Why did the Fed hold rates steady?

The Fed held rates steady because inflation remains elevated, global energy prices have risen, and the Iran war has increased uncertainty around the economic outlook.

What does Jerome Powell staying as governor mean?

It means Powell may no longer be Fed chair, but he can still remain inside the Federal Reserve as a board governor. That gives the institution continuity during the transition to Kevin Warsh, while Powell has said he does not intend to act as a “shadow chair.”

Could Kevin Warsh change Fed policy?

Yes, but not instantly or alone. A Fed chair can shape communication and consensus, but interest-rate decisions are made by the broader FOMC. Today’s divided vote suggests Warsh may inherit a committee that is already split.

How does the Iran war affect inflation and interest rates?

The Iran war can push oil and energy prices higher, which can feed into inflation. That makes it harder for the Fed to cut rates because lower rates could worsen inflation expectations at a time when price pressures are already elevated.

What does the Fed’s decision mean for mortgages and credit cards?

It means borrowing costs are likely to remain elevated for now. A rate hold does not reduce mortgage rates, credit-card APRs, or auto-loan costs immediately. It keeps financial pressure in place while the Fed waits for clearer inflation and labor-market data.

When could the Fed cut rates?

The Fed could cut rates when inflation cools more convincingly, the labor market weakens, or financial conditions tighten enough to threaten growth. But the Iran war, higher oil prices, and internal disagreement at the Fed make the timing less certain.